![StubHub Holdings, Inc. (STUB) Securities Class Action Lawsuit Update [December 3, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/stub-alert-plus-banner.webp)

Anatomy of a Post-IPO Collapse

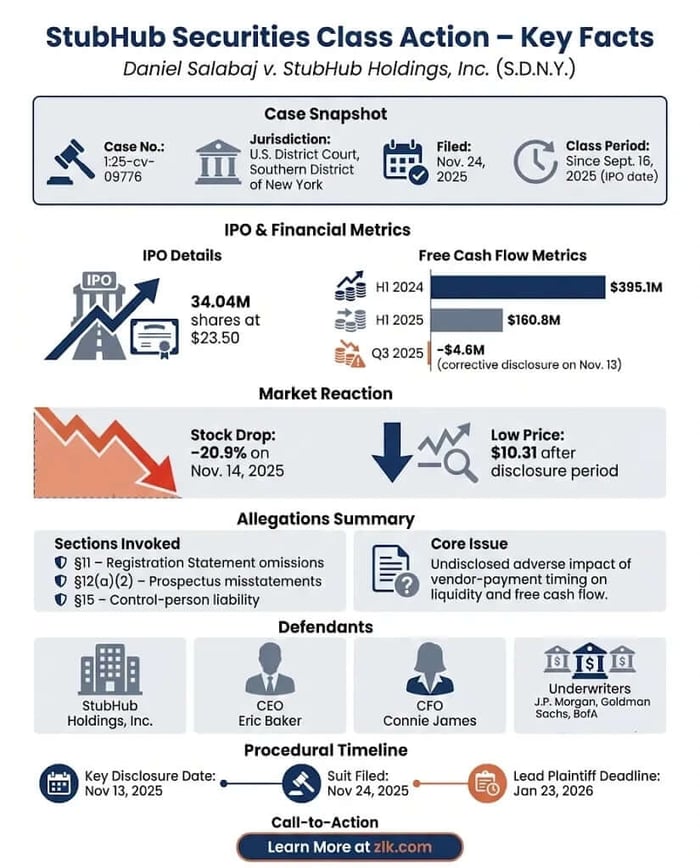

Case Name: Salabaj v. StubHub Holdings, Inc. et al.

Case No.: 1:25-cv-09776

Jurisdiction: U.S. District Court, Southern District of New York

Filed on: November 24, 2025

Class Period: September 16, 2025 (IPO Date)

Introduction

Red Cat said it was ready to soar. It wasn’t. StubHub Holdings, Inc., the global ticketing giant, conducted its initial public offering (IPO) in September 2025, promising investors a platform poised for growth and, crucially, a solid financial footing measured by its free cash flow. Now, mere weeks after that market debut, the company faces a securities class action lawsuit that lays bare the peril of undisclosed operational trends—a reckoning over liquidity that began the moment the market realized what had been left out of the Offering Documents.

The lawsuit, Daniel Salabaj v. StubHub Holdings, Inc. et al., filed in the U.S. District Court for the Southern District of New York (Case No. 1:25-cv-09776), focuses on a fundamental disconnect: the IPO materials presented free cash flow as a key liquidity metric yet, investors allege, they omitted the significant, adverse impact that changes in the timing of payments to vendors were already having. When the company finally disclosed a precipitous decline in free cash flow on November 13, 2025, the market reaction was immediate and punishing. The stock lost nearly 21% of its value the following day, plunging below its $23.50 offering price. The narrative that had been so carefully constructed for the IPO had shattered.

Backdrop and Business Context

StubHub Holdings, Inc. operates a vast, established ticketing marketplace, running a global platform for live-event tickets through the StubHub and viagogo websites. It is a dual-brand powerhouse providing online marketplaces that enable buyers and sellers to transact for live events across geographies, capitalizing on the persistent consumer appetite for experiences.

The company’s Initial Public Offering in September 2025 was a high-profile event, pricing 34.04 million shares at $23.50 each. The Offering Documents, including the Registration Statement, served as the primary source of financial representation for prospective investors. Within these documents, the company specifically highlighted free cash flow, stating it was "a meaningful indicator of liquidity for management and investors," and reporting its metrics for the first half of 2025 compared to 2024. This metric, in the opaque world of ticketing transactions, is often critical for assessing a marketplace’s health—the actual cash flow derived from operations. It is the lifeblood of a company’s ability to fund strategy or service debt (the reason we look at it is precisely because it cuts through accounting noise). The entire operational setup leading up to the IPO was one of capitalizing on the post-pandemic live-event boom and demonstrating financial stability.

Promises Made vs. Reality

In the Registration Statement, StubHub told investors that free cash flow in the first half of 2025 was $160.8 million, down from $395.1 million in the first half of 2024. The company acknowledged the decrease, attributing it "primarily to changes in the timing of cash receipts and payments associated with ticket sales as well as the timing of payments to vendors."

The problem, as alleged in the complaint, was one of magnitude and omission.

The filing alleges that StubHub’s disclosure was materially misleading because it failed to convey that the company was not merely experiencing changes in payment timing, but that those changes were having a significant adverse impact on its financial health, including its trailing 12 months free cash flow. The alleged promise—that the company's financial liquidity was sound—contrasted sharply with the reality that investors believe was obscured.

The truth, or at least a more granular truth, surfaced on November 13, 2025, when StubHub issued a press release and filed its Form 10-Q for the third quarter. Management stated plainly: "During the three months ended September 30, 2025, the decrease in free cash flow, compared to the same periods in the prior year, primarily reflects changes in the timing of payments to vendors." This post-IPO disclosure of significant operational impact is the core of the class action: investors claim they were not adequately warned of the severity of this "change" when the company went public.

Timeline of Alleged Misconduct and Disclosures

The narrative of the case is a rapid descent from the confidence of an IPO to the stark reality of post-earnings losses.

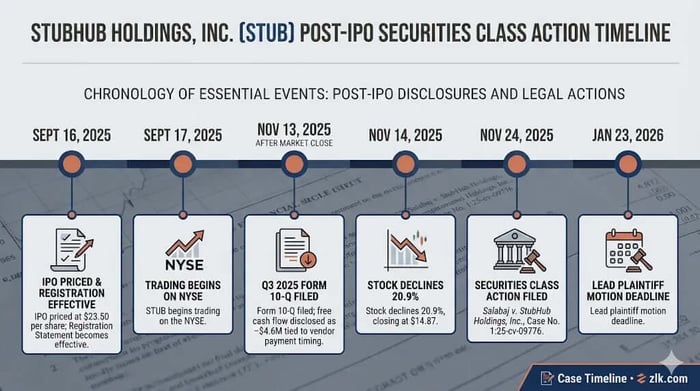

September 16, 2025: StubHub prices its IPO at $23.50 per share; the Registration Statement, which is alleged to be misleading, becomes effective.

September 17, 2025: StubHub begins trading on the NYSE under the ticker STUB, raising hundreds of millions and achieving a high-profile market debut.

November 13, 2025 (After Market Close): StubHub files its Q3 2025 Form 10-Q, revealing a free cash flow of negative $4.6 million, a 143% decline from the prior year's positive $10.6 million. The Company explicitly ties the decline to changes in the timing of payments to vendors.

November 14, 2025: The first trading day following the disclosure. The stock falls $3.95, or 20.9%, closing at $14.87 on unusually heavy trading volume.

November 24, 2025: The first securities class action lawsuit, Salabaj v. StubHub Holdings, Inc. et al., is filed. The stock had, by this point, traded as low as $10.31 per share.

Investor Harm and Market Reaction

The loss causation event—the moment the undisclosed risk materialized and decimated shareholder value—is unequivocally tied to the November 13, 2025, disclosure. Prior to that date, investors held shares under the assumption of a clear, albeit declining, liquidity trajectory. The Q3 report, however, revealed a sudden, negative pivot in free cash flow, which management immediately linked to the exact factor the IPO documents allegedly downplayed: vendor payment timing.

On November 14, 2025, the stock's 20.9% drop wiped out over a billion dollars in market capitalization. This was not a general market correction; it was a specific, violent reaction to the company’s stated financial condition. By the time the lawsuit was filed ten days later, the stock had reached a low of $10.31 per share, representing a nearly 56% decline for initial purchasers—a profound loss for those who acquired shares in the IPO. This steep decline suggests that the market, once fully informed, dramatically re-rated the company’s underlying liquidity risk and business model.

Litigation and Procedural Posture

The class action is brought pursuant to the Securities Act of 1933, which governs the registration and disclosure requirements for securities sold to the public, like in an IPO. The primary claims asserted are:

Section 11: Alleging material misstatements and omissions in the Registration Statement, a claim that does not require the plaintiff to prove scienter (intent to defraud) against the issuer.

Section 12(a)(2): Alleging material misstatements or omissions in the Prospectus or oral communications.

Section 15: Asserted against the individual officers and directors for their liability as "control persons" over the company and its filings.

The defendants include the company itself, five key executives and directors—CEO Eric H. Baker and CFO Connie James among them—and a lengthy list of major investment banks that acted as underwriters, including J.P. Morgan Securities LLC, Goldman Sachs & Co. LLC, and BofA Securities, Inc.

The litigation's initial phase focuses on the selection of a lead plaintiff, with a motion deadline set for January 23, 2026. The court’s appointment of the lead plaintiff and counsel will determine the direction and ultimate strategy of the class. Given that the claims are brought under the 1933 Act, the focus will be on the objectively material nature of the alleged omission regarding free cash flow, rather than the more difficult hurdle of proving scienter required under the 1934 Act's Rule 10b-5. This is a battle over the completeness of the narrative presented to new investors.

Shareholder Sentiment

The reaction across investor forums and social platforms mirrored the violence of the stock chart—a shift from post-IPO excitement to betrayal. Before the November 13th disclosure, sentiment was cautiously optimistic, with many discussions centering on the long-term potential of the viagogo merger integration.

The Q3 disclosure, however, acted as a cold, hard dash of water. On Stocktwits and Reddit threads, the commentary shifted almost instantly. Early posts following the news were often characterized by raw anger and confusion. There was a palpable sense that management had been overly sanguine about a critical liquidity metric. For many retail investors who bought into the IPO narrative, the experience was a jarring lesson in financial nuance, proving that an IPO prospectus, however glossy, often needs a level of scrutiny that goes beyond the headline numbers. The general sentiment settled into frustration.

Analyst Commentary

The professional investment community’s initial take on StubHub was framed by the excitement of a major IPO in a recovering sector. Initial coverage, primarily from the underwriter banks, was predictably bullish, with target prices often sitting comfortably above the $23.50 IPO price. They were selling the promise, and their reports reflected that.

The free cash flow decline led to an immediate crisis of confidence among independent analysts, and likely forced the hand of those at the underwriting institutions.

Following the November 13th disclosure, several analysts quickly moved to downgrade the stock from "Buy" or "Outperform" to "Hold" or "Market Perform." The commentary focused less on the core business strength and more on the lack of financial visibility. One major firm’s note reportedly stated that the cash flow volatility was unacceptable for a mature marketplace business, forcing a dramatic lowering of their price target from $30 to $18—a move that fundamentally re-priced the stock based on the newly revealed operational risk. The consensus shifted from viewing the stock as an attractive growth play to one burdened by significant, and now apparent, liquidity management issues.

SEC Filings & Risk Factors

The securities claims hinge on what the company chose to include in its filings. The foundational document for the IPO, the Registration Statement (effective September 16, 2025), is the focus.

In a typical IPO, the Risk Factors section is comprehensive, detailing anything from macroeconomic conditions to competitive risks. The lawsuit centers on the idea that, while the company included the change in vendor payment timing as an explanatory factor for past performance (the $160.8M vs. $395.1M in H1 free cash flow), it failed to adequately disclose this as a known trend or uncertainty that was likely to have a material adverse impact on the company going forward. An omission of this magnitude violates the spirit of risk factor disclosure, which requires management to highlight factors that could cause actual results to differ materially from expectations.

The subsequent Form 10-Q for the quarter ended September 30, 2025 (filed November 13, 2025), is the corrective disclosure itself. This document, with its explicit admission of negative $4.6 million in free cash flow and the blame placed on vendor payment timing, is the evidence used to prove that the risk was not only known at the time of the IPO but was actively impacting the company's financial results. In short, the 10-Q provides the 'before' and 'after' narrative that supports the core allegation of the class action.

Conclusion: Implications for Investors

The StubHub case is a powerful reminder that an IPO is not an end point; it is a point of maximum financial scrutiny. For fund managers and individual investors, the alleged omission regarding free cash flow is a textbook red flag concerning liquidity and management's transparency in critical financial metrics.

Investors should learn to focus intently on the footnotes and Management’s Discussion and Analysis (MD&A) sections of the S-1 and Prospectus. When a company highlights a key metric like free cash flow, but then attributes a dramatic decline to a factor like "timing of payments"—as StubHub did—that language should trigger deep skepticism. It’s a classic sign of potential cash flow manipulation or, at the very least, an unstable financial foundation. The broader relevance for the investment sector is clear: the post-IPO honeymoon period is vanishingly short, and any company coming to market that prioritizes growth over verifiable cash flow stability will be vulnerable to this kind of immediate, painful correction.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![DeFi Technologies Inc. (DEFT) Securities Class Action Lawsuit Update [December 8, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/deft-alert-plus-banner.webp)

![Bitdeer Technologies Group (BTDR) Securities Class Action Lawsuit Update [December 8, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/btdr-alert-plus-banner.webp)

![Blue Owl Capital Inc. (OWL) Securities Class Action Lawsuit Update [December 9, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/owl-alert-plus-banner.webp)