![Dow Inc. (DOW) Securities Class Action Lawsuit Update [December 26, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/dow-alert-plus-banner.webp)

Dow Inc. — What Happened When the Dividend Cracked

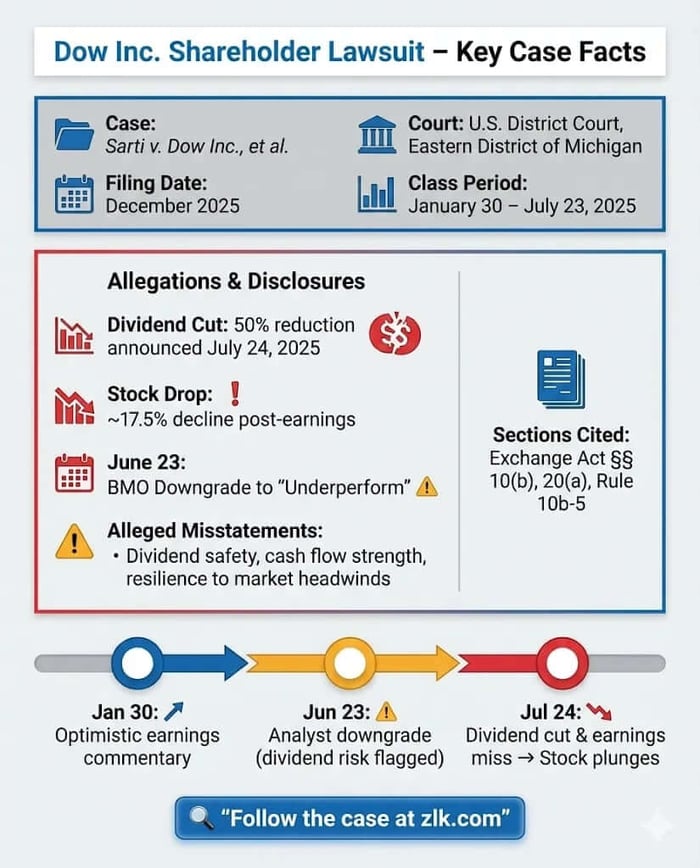

Caption: Sarti v. Dow Inc. et al.

Case No.: 1:25-cv-12744-TLL-PTM

Jurisdiction: U.S. District Court, Eastern District of Michigan, Northern Division

Filed on: August 29, 2025

Class Period: January 30, 2025–July 23, 2025

Introduction

Dow Inc. sold certainty in an uncertain world. Investors bought it. Between January 30, 2025, and July 23, 2025, shareholders allege that Dow Inc. and senior executives overstated the company’s resilience to macroeconomic and tariff-related headwinds—while quietly underestimating the strain those forces placed on cash flow and an “industry-leading” dividend. When the truth surfaced in mid-2025, the stock dropped sharply, the dividend was cut in half, and a federal securities class action followed.

The lawsuit, Sarti v. Dow Inc., et al., pending in the U.S. District Court for the Eastern District of Michigan, alleges violations of Sections 10(b) and 20(a) of the Exchange Act. At the center of the case: whether Dow’s public confidence masked a reality investors were not shown.

Backdrop and Business Context

Dow is a global materials science company serving packaging, infrastructure, mobility, and consumer markets through three operating segments: Packaging & Specialty Plastics; Industrial Intermediates & Infrastructure; and Performance Materials & Coatings. The company has long framed its dividend as a cornerstone of its investment thesis, repeatedly emphasizing financial discipline, cost-advantaged assets, and feedstock flexibility as buffers against cyclical downturns.

During an industry slump and rising trade uncertainty, management highlighted asset sales, cost reductions, and growth projects as evidence that Dow could protect margins and maintain shareholder returns. According to the complaint, these assurances became the narrative spine of Dow’s communications—one that investors relied on as conditions worsened.

Promises Made vs. Reality

Executives consistently told markets that Dow could weather the storm. In earnings releases and conference calls, CEO Jim Fitterling described the dividend as “a key element of our investment thesis,” asserting that more than 65% of shareholders depended on it. CFO Jeffrey Tate and COO Karen Carter echoed the theme, pointing to cost actions, global footprint flexibility, and near-term growth projects that would supposedly sustain cash flow.

The complaint alleges these statements omitted critical context: intensifying pricing pressure, softening global demand, and product oversupply across key markets. Plaintiffs say Dow’s true capacity to absorb these pressures—while maintaining its dividend—was materially overstated. When Q2 2025 results arrived, the gap between promise and performance became visible.

Timeline of Alleged Misconduct and Disclosures

The alleged class period opens on January 30, 2025, with upbeat commentary around Q4 2024 results and 2025 outlook. Through spring 2025, Dow continued to stress volume growth, cost discipline, and dividend safety.

On June 23, 2025, BMO Capital downgraded Dow to “Underperform,” citing weak end-markets and warning that the dividend could be at risk. Shares fell about 3% that day.

The pivotal moment came July 24, 2025. Dow reported a larger-than-expected non-GAAP loss for Q2, missed revenue estimates, and—separately—announced that it was cutting its dividend in half. The stock dropped roughly 17.5% in a single session. Analysts reacted quickly, slashing price targets and questioning whether the prior dividend narrative had been realistic.

Investor Harm and Market Reaction

According to the complaint, investors who purchased Dow securities during the class period suffered significant losses as the market repriced the company’s earnings power and capital allocation strategy. The July 24 sell-off alone erased billions in market value.

Analysts described the earnings miss as “well below” even lowered expectations. Bloomberg later reported that multiple firms reduced price targets by an average of roughly 13%. Plaintiffs tie these reactions directly to the corrective disclosures, arguing that the stock had been artificially inflated by prior statements minimizing known risks.

Litigation and Procedural Posture

The case asserts claims under Section 10(b) and Rule 10b-5 against Dow and its executives, and Section 20(a) control-person claims against individual defendants. Plaintiffs allege scienter based on executives’ access to internal data, repeated emphasis on dividend stability, and certifications accompanying SEC filings.

The lawsuit is in its early stages. No merits rulings have been issued, and defendants have not yet filed substantive responses. As with many securities class actions, the next inflection point will likely be a motion to dismiss testing whether the alleged misstatements, omissions, and loss causation are adequately pleaded.

Shareholder Sentiment

Investor sentiment turned sharply negative following the July 2025 dividend cut, with many long-term holders expressing betrayal and frustration on social media and forums. On Reddit's r/dividends, users described the move as inevitable but painful, with one noting that high yields had masked underlying issues and labeling dividends in such cases as "meaningless" compared to fundamentals. In r/ValueInvesting, investors who had bought for the yield announced plans to sell, citing broken promises from management just months earlier. Some viewed the cut as overdue realism in a cyclical industry, while others saw it as confirmation of eroded credibility, shifting pre-cut optimism about Dow's defensive qualities to widespread skepticism.

Analyst Commentary

Prior to the Q2 2025 earnings, analysts largely held neutral views, appreciating Dow's scale but wary of macro pressures; BMO's June downgrade explicitly highlighted dividend risk amid weak markets. Post-earnings, reactions were broadly negative, with firms slashing targets and emphasizing prolonged pricing pressure, oversupply, and reduced cash flow confidence.

Morningstar analysts noted the cut "shouldn’t have been a surprise" given free cash flow shortfalls and high leverage exceeding targets. Investing.com transcripts and reports highlighted a "lower for longer" environment prompting the reduction for flexibility. Many questioned management's timing in adjusting expectations, viewing the move as prudent but reflective of deeper industry challenges

SEC Filings & Risk Factors

Dow’s Form 10-K and subsequent filings contained risk disclosures about macroeconomic volatility and trade uncertainty. Plaintiffs argue these warnings were generic and failed to capture the severity of known trends—particularly the impact on pricing, demand, and dividend sustainability.

The complaint also alleges violations of Item 303 of Regulation S-K, asserting that Dow did not adequately disclose known uncertainties reasonably likely to have a material adverse effect on revenues and cash flow. Executive certifications accompanying these filings are cited as further evidence that management stood behind statements investors now challenge.

Conclusion: Implications for Investors

The Dow lawsuit underscores a familiar tension in cyclical industries: the desire to project stability when conditions are anything but. For investors, the case is a reminder to interrogate dividend narratives, stress-test assurances of “financial flexibility,” and watch closely how management discusses known headwinds.

This isn’t a verdict. It’s a reckoning in progress—one that may shape how capital-intensive companies communicate resilience in volatile markets.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Vistagen Therapeutics, Inc. (VTGN) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/vtgn-alert-plus-banner.webp)

![Smart Digital Group Limited (SDM) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/sdm-alert-plus-banner.webp)

![Bath & Body Works, Inc. (BBWI) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/bbwi-alert-plus-banner.webp)