![Freeport-McMoRan Inc. (FCX) Securities Lawsuit Update [November 26, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/fcx-alert-plus-banner.webp)

The Safety Pretense Behind Catastrophic Shareholder Losses

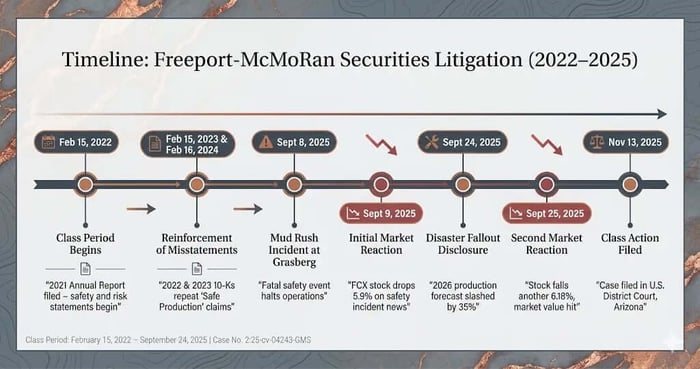

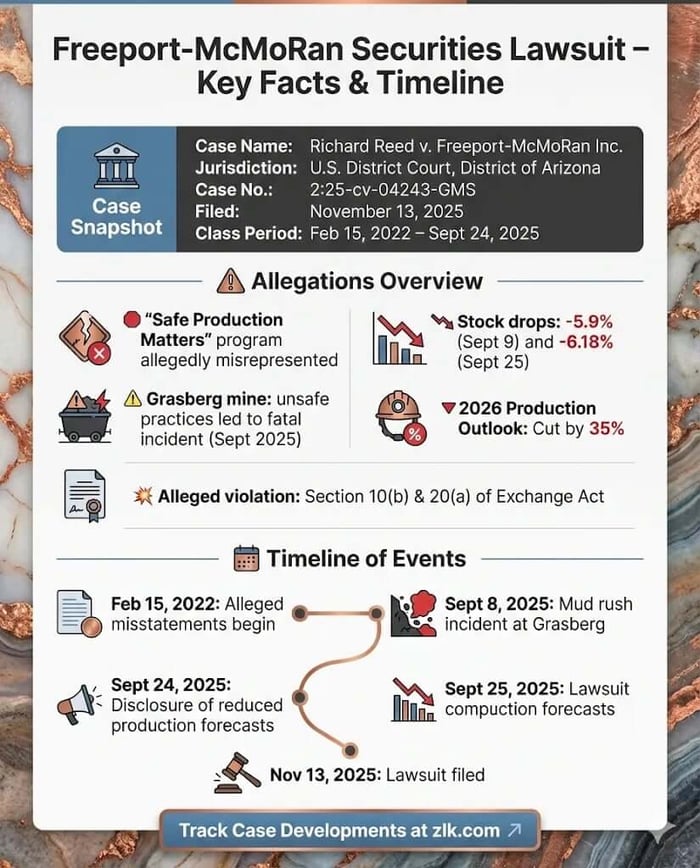

Case Name: Reed v. Freeport-McMoRan Inc., et al.

Case No.: 2:25-cv-04243-GMS

Jurisdiction: U.S. District Court, District of Arizona

Filed on: November 13, 2025

Class Period: February 15, 2022–September 24, 2025

Introduction

A new reckoning has arrived for the copper and gold giant, Freeport-McMoRan Inc. (NYSE: FCX), which now faces a securities class action lawsuit in the United States District Court for the District of Arizona. The lawsuit, led by Plaintiff Richard Reed , asserts that the Company and its senior leadership misled investors over a class period spanning from February 15, 2022, through September 24, 2025 , by fundamentally misrepresenting the safety and operational integrity of its most crucial asset, the Grasberg Mine in Indonesia. The heart of the allegation is simple: Freeport’s promises of "Safe Production Matters" were a thin, hollow shell, hiding systemic unsafe practices that exposed the business to material and foreseeable risk. The truth was violently exposed by a devastating mine safety incident in September 2025, triggering a pair of sharp stock drops that quantify the investor harm. For sophisticated investors and fund managers, this case is not merely about mining misstatements; it is a profound lesson in the market’s intolerance for the unstated operational risk that lies just beneath the veneer of corporate ESG promises.

Backdrop and Business Context

Freeport-McMoRan, a mining company incorporated in Delaware and headquartered in Phoenix, Arizona, is globally synonymous with the extraction of copper, gold, and molybdenum. Its common stock is traded on the New York Stock Exchange under the ticker symbol FCX. The gravity of this lawsuit rests almost entirely on a single, massive piece of geography: the Grasberg Copper and Gold Mine in Papua, Indonesia. Grasberg is not just a major asset; it is one of the world's most significant business enterprises in a geologically and politically complex region. The Indonesian government, through a state-owned enterprise, holds a commercial interest in the mine, making the Company’s operations intrinsically linked to the delicate geopolitical winds of Southeast Asia. Operations at Grasberg require meticulous management—of the ore body, of the subterranean hazards, and of the relationship with Jakarta. When the alleged misconduct was underway, the Company’s leadership included former CEO and current Chairman Richard C. Adkerson , CEO Kathleen L. Quirk , and CFO Maree E. Robertson. Their task was to project stability for an operation defined by its immensity and inherent instability.

Promises Made vs. Reality

The chasm between Freeport’s public posture and the alleged operational reality forms the legal basis of the claim. In its Annual Reports on Form 10-K, filed with the SEO throughout the Class Period, the Company spoke with clear conviction about its priorities and its commitment to safety.

Promises Made:

The 2021 Annual Report declared, "Our highest priority is the health, safety and well-being of our employees and contractors."

Management asserted a dedication to fatality prevention and continuous improvement, stating that its global health and safety approach, "Safe Production Matters," was built on robust management systems.

The Company touted its risk management framework as certified company-wide in accordance with the new[ISO 45001 Health and Safety Management System, with the objective to achieve zero workplace fatalities.

Defendants Adkerson and Quirk, and later Robertson, signed Sarbanes-Oxley certifications attesting to the accuracy of financial reporting and the disclosure of all fraud.

Reality Alleged: The lawsuit claims these statements were materially false and misleading because, despite the rhetoric, Freeport did not adequately ensure safety at the Grasberg Block Cave mine. The reality, according to the complaint, was that the Company was conducting unsafe mining practices which were "reasonably likely to result in worker deaths." This systemic lack of proper safety constituted a heightened risk that Defendants knew or should have known would trigger heightened regulatory scrutiny by the Indonesian government. The grand pronouncements of "Safe Production Matters" were, therefore, a concealment of a material and ticking operational time bomb.

Timeline of Alleged Misconduct and Disclosures

The narrative of misstatement and ultimate corrective disclosure follows a clean, rhythmic cadence, building tension over years of alleged concealment before the inevitable market rupture:

February 15, 2022: Freeport files its 2021 Annual Report on Form 10-K, making the earliest alleged misstatements regarding safety commitments and risks in Indonesia. This marks the beginning of the Class Period.

February 15, 2023 & February 16, 2024: The Company files its 2022 and 2023 Annual Reports, containing substantially similar, and therefore continuously false, representations regarding safety and Indonesian regulatory risks.

September 8, 2025 (First Disclosing Event): A catastrophic safety incident—described by an expert later as a preventable "mud rush"—occurs at the Grasberg Block Cave mine, where affected team members were engaged in mine development activities. Mining operations were temporarily suspended to prioritize evacuation.

September 9, 2025 (Initial Market Reaction): On the initial news of the tragic event and operational suspension, the price of Freeport stock fell sharply, losing $2.77 per share, representing a 5.9% drop.

September 24, 2025 (Second Disclosing Event): Freeport issues a second press release providing a far more devastating assessment of the incident's fallout. The Company disclosed a phased restart and ramp-up scenario under which PTFI production in 2026 could potentially be approximately 35% lower than pre-incident estimates. The Company also noted it would seek recovery under insurance policies, revealing a $1.0 billion cap on losses (subject to a $0.7 billion limit on underground incidents).

September 25, 2025 (Severe Market Reaction): The market recoils from the dire operational forecast. Freeport stock plunges again, falling another $2.33 per share, or 6.18%, closing the day at $35.34. The Class Period ends on this date.

September 28, 2025 (Post-Class Period Media Coverage): A news organization focusing on Indonesia, Tempo, publishes an article citing an expert who stated the landslide was "Preventable, Not Just a Natural Disaster." The expert emphasized that this specific risk, known as a mud rush, should have been anticipated from the beginning.

Investor Harm and Market Reaction

The damages were not abstract; they were specific and quantifiable. Investors acquired Freeport securities under the belief that the Company was managing its paramount operational risk responsibly, as repeatedly attested to in its SEC filings. This confidence inflated the stock price, which then shattered across the two corrective disclosures in September 2025. The complaint explicitly ties the abrupt market value destruction to the disclosures revealing the human and operational costs of the alleged safety failures. The initial 5.9% drop on September 9, 2025, was merely the first strike; it was the second disclosure on September 24, 2025—which forecast a staggering 35% cut to 2026 production estimates—that triggered the decisive 6.18% collapse, stripping billions of dollars from the Company’s market capitalization and cementing the loss causation for investors. The case posits that absent the Defendants' alleged misstatements regarding safety and internal controls, the stock would not have traded at the artificially inflated prices throughout the Class Period.

Litigation and Procedural Posture

The securities class action, filed in the U.S. District Court for the District of Arizona, asserts two core legal claims against the Defendants:

Count I: Violations of Section 10(b) of the Exchange Act and Rule 10b-5 promulgated thereunder. This claim is asserted against all Defendants (Freeport-McMoRan Inc. and the Individual Defendants). It alleges that they employed devices, schemes, and artifices to defraud, made untrue statements of material facts, and engaged in acts that operated as a fraud or deceit upon investors.

Count II: Violations of Section 20(a) of the Exchange Act. This is a control person liability claim asserted against the Individual Defendants—Quirk, Adkerson, and Robertson. It argues that because of their positions as senior officers, they were "controlling persons" of the Company and exercised power and authority to cause the Company to engage in the wrongful acts.

The critical hurdle in any Section 10(b) case is scienter, the intent to deceive, manipulate, or defraud. The complaint attempts to clear this bar by arguing the Individual Defendants either knew the public documents were materially false and misleading, or acted with reckless disregard for the truth by failing to disclose the unsafe practices that put Freeport’s core asset and revenue stream at material risk. The case is in its initial procedural posture, awaiting the appointment of lead plaintiff and lead counsel before moving toward discovery and the inevitable motion to dismiss.

Shareholder Sentiment

The immediate sentiment following the September disclosures was one of shock and betrayal. While the formal complaint does not capture specific data from platforms like X/Twitter or Reddit, the sheer magnitude of the stock drops—two back-to-back collapses for a combined loss of over 12% of the stock price—is a visceral metric of shareholder confidence hemorrhaging in real time. The focus swiftly shifted from the price of copper to the price of a life, or multiple lives, lost due to a seemingly preventable operational failure. The emotional arc moves from optimistic belief in management’s safety rhetoric to a bitter understanding that the Company's culture may have prioritized short-term production over human capital and long-term stability. The narrative shifts from "FCX is a commodities play" to "FCX is a failure of governance," a change in tone that fuels the momentum of the class action.

Analyst Commentary

Analyst commentary, like shareholder sentiment, undergoes a violent reset in the wake of such a crisis. Prior to the September 2025 incident, reports focused on macro commodity demand, global copper inventory, and the operational ramp-up success at Grasberg. Target prices were predicated on the Company's own production guidance, which now appears to have been anchored to an unsustainable—and allegedly unsafe—operational tempo. After the initial September 9, 2025, incident, there came a flurry of immediate price target cuts, shifting recommendations from 'Buy' or 'Hold' to 'Underperform' or 'Sell' until the operational risk could be fully assessed. The second disclosure, which quantified the crisis as a 35% reduction in 2026 production estimates, solidified a harsh consensus. Commentary centered on the immediate withdrawal of confidence in management's ability to forecast production and, more critically, the newly revealed, unpriced "geopolitical and operational risk premium" now necessary for the stock.

SEC Filings & Risk Factors

A review of Freeport’s SEC filings, such as the 2021, 2022, and 2023 Annual Reports on Form 10-K, reveals the critical legal tension in the case. The Company did disclose standard risks associated with operating in Indonesia, acknowledging that its business could be "adversely affected by political, economic and social uncertainties in Indonesia." It specifically warned that "Improper management of our working relationship with the Indonesia government could lead to a disruption of operations [...]." However, the class action complaint alleges that this disclosure was materially misleading because it failed to articulate the internal, self-inflicted risk: that Freeport’s own unsafe practices were making the very regulatory disruption it warned about "reasonably likely." While the Company published an extensive section detailing its commitment to the ISO 45001 Health and Safety Management System and its goal of zero workplace fatalities , the legal assertion is that the core, latent risk of a preventable mud rush—a known phenomenon in certain mining methods —was omitted, rendering the high-minded safety rhetoric disingenuous. The boilerplate risk was adequately disclosed; the allegedly concealed unacceptable safety culture was not.

Conclusion: Implications for Investors

The Freeport-McMoRan case offers investors a stark reminder that operational misstatement often cloaks itself in the guise of non-financial metrics—the Environmental, Social, and Governance (ESG) promises that institutional investors now covet. When a company proclaims its "highest priority is the health, safety and well-being of our employees", that is not merely good corporate citizenship; it is a material representation of business continuity and risk management. This lawsuit makes clear that a material misstatement on a core ESG factor, like safety, can translate into immediate and devastating production shortfalls, such as the predicted 35% cut to 2026 copper and gold output. The key red flag here is the disconnect between corporate rhetoric and fundamental operational reality in a sensitive, high-consequence asset like Grasberg. Investors must scrutinize global operators not just on their production numbers, but on the veracity of the safety and internal control certifications signed by their most senior executives. The legal system is now tasked with determining whether this operational failure was simply a tragedy, or a scheme.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Perrigo Company PLC (PRGO) Securities Class Action Update [December 2, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/prgo-alert-plus-banner.webp)

![Integer Holdings Corporation (ITGR) Securities Class Action Lawsuit Update [December 17, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/itgr-alert-plus-banner.webp)

![Blue Owl Capital Inc. (OWL) Securities Class Action Lawsuit Update [December 9, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/owl-alert-plus-banner.webp)