![Perrigo Company PLC (PRGO) Securities Class Action Update [December 2, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/prgo-alert-plus-banner.webp)

PRGO Faces Investor Reckoning

Case Name: French v. Perrigo Company plc et al.

Case No.: 1:25-cv-09596

Jurisdiction: U.S. District Court, Southern District of New York

Filed on: November 17, 2025

Class Period: February 27, 2023 - November 4, 2025

Introduction

Perrigo Company PLC (NYSE: PRGO) is facing a securities class action in the Southern District of New York (Case No. 1:25-cv-09596). Lead plaintiff Tanner French alleges that between February 27, 2023 and November 4, 2025, Perrigo misled investors about the health of its infant formula business. The complaint names CEO Patrick Lockwood-Taylor, former CEO Murray Kessler, and CFO Eduardo Bezerra. At issue are claims that Perrigo overstated earnings, concealed manufacturing deficiencies, and underestimated remediation costs. Investors saw four sharp stock drops, culminating in a 25.2% collapse on November 5, 2025.

Backdrop and Business Context

Perrigo, incorporated in Ireland, markets over-the-counter health and wellness products across the U.S., Europe, and internationally. Infant formula is a critical segment, representing about 17% of North American sales in 2024. In November 2022, Perrigo acquired Nestlé’s Gateway plant in Wisconsin and the Good Start® brand for $170 million, touting the deal as a strategic expansion. The acquisition was part of a broader “Supply Chain Reinvention Program,” which promised $200–$300 million in annual savings by 2028. Instead, the Gateway plant exposed underinvestment, operational deficiencies, and regulatory risks that undermined Perrigo’s narrative of growth.

Promises Made vs. Reality

Publicly, Perrigo emphasized compliance with FDA Current Good Manufacturing Practices and assured investors that remediation costs would remain flat. Press releases highlighted “record net sales” and “strategic pricing actions.” Executives spoke of synergies and resilience. Reality diverged. The complaint alleges chronic underinvestment in maintenance and escalating remediation costs. By August 2025, Perrigo admitted to scrapping $11 million in infant formula inventory. Despite upbeat assurances, the company faced mounting production variability and declining margins. The November 2025 announcement of a strategic review confirmed that the infant formula business had become “less strategic,” contradicting years of optimistic messaging.

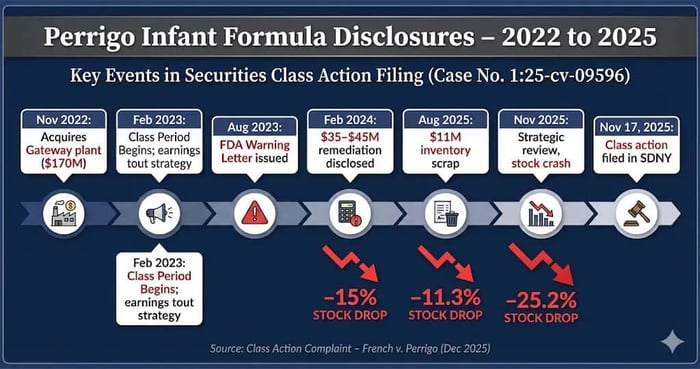

Timeline of Alleged Misconduct and Disclosures

November 1, 2022: Perrigo completes the acquisition of Nestlé’s Gateway infant formula manufacturing facility in Wisconsin and the U.S. and Canadian rights to the Good Start® infant formula brand for approximately $170 million.

February 27, 2023: Start of the alleged Class Period. Perrigo issues a press release announcing fourth-quarter and full-year 2022 earnings, highlighting growth and the strategic value of its infant formula investment.

February 28, 2023: Perrigo files its Form 10-K for fiscal year 2022, affirming prior results and describing capital expenditures and compliance with FDA manufacturing standards.

March 17, 2023: Perrigo initiates a voluntary recall of a specific infant formula product manufactured between January 2 and January 18, 2023, citing FDA communications and evolving regulatory expectations.

May 9, 2023: Perrigo releases first-quarter 2023 earnings, reporting growth and stating that integration of the Gateway facility and Good Start® brand is on track, despite impacts from a voluntary recall.

August 8, 2023: Perrigo reports second-quarter 2023 earnings, attributing Nutrition segment growth primarily to the Gateway acquisition.

August 30, 2023: Perrigo receives an FDA warning letter following a routine inspection of the Wisconsin infant formula facility acquired from Nestlé.

November 29, 2023: Perrigo receives notice of additional FDA inspection observations at the Wisconsin facility and temporarily pauses production to conduct an extended site-wide assessment and cleaning.

February 27, 2024: Perrigo reports full-year 2023 earnings, disclosing significant infant formula remediation costs estimated at $35–$45 million, a 50% year-over-year decline in earnings per share, and reduced expectations for infant formula operating income. Perrigo’s stock price falls approximately 15%.

May 7, 2024: Perrigo announces first-quarter 2024 earnings, reporting sharply lower infant formula sales and margins due to remediation actions. The stock price declines approximately 9.8%.

August 6, 2025: Perrigo releases second-quarter 2025 earnings, disclosing production variability, increased product scrap, and approximately $11 million in inventory write-offs related to infant formula manufacturing. Shares fall approximately 11.3%.

November 5, 2025: Perrigo announces a strategic review of its infant formula business and cuts full-year 2025 financial guidance, citing infant formula industry dynamics. The stock price drops approximately 25.2%.

November 17, 2025: The class action complaint is filed in the U.S. District Court for the Southern District of New York, asserting claims under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934.

Each disclosure chipped away at investor confidence, exposing the gap between Perrigo’s narrative and operational reality.

Investor Harm and Market Reaction

Investor Harm and Market Reaction

The cumulative losses were severe. Investors who bought into Perrigo’s growth story saw value erode with each corrective disclosure. Analysts downgraded PRGO repeatedly, citing “execution risk” and “supply chain instability.” Trading volumes spiked on disclosure days, signaling panic exits. By November 2025, PRGO shares had lost more than half their value compared to pre-acquisition highs, leaving investors questioning management credibility.

Litigation and Procedural Posture

The complaint asserts violations of Sections 10(b) and 20(a) of the Exchange Act and Rule 10b-5. Defendants include Perrigo, CEO Lockwood-Taylor, former CEO Kessler, and CFO Bezerra. Allegations of scienter hinge on their access to non-public information and repeated assurances despite known deficiencies. The case is at its early stage, with jury trial demanded. Procedural milestones will likely include motions to dismiss, class certification, and discovery focused on internal communications and remediation costs.

Shareholder Sentiment

On Reddit and Stocktwits, sentiment shifted from cautious optimism to frustration. Early posts praised Perrigo’s “strategic expansion” and “undervalued growth play.” By mid-2024, threads lamented “another remediation surprise” and “management spin.” After the August 2025 disclosure, X/Twitter users focused on PRGO = Perrigo’s Gateway to Losses as a mantra about the firm. The November 2025 collapse triggered calls for leadership change and speculation about activist investor involvement.

Analyst Commentary

Sell-side analysts initially maintained “Buy” ratings, citing synergies and market share gains. Following the February 2024 disclosure, downgrades to “Hold” and “Underperform” proliferated. Target prices fell from the mid-$40s to the low $20s. Reports highlighted execution missteps and capital drain from infant formula. By November 2025, consensus turned bearish, with some analysts warning of “structural impairment” to Perrigo’s U.S. nutrition business.

SEC Filings & Risk Factors

Perrigo’s FY22 10-K disclosed risks of contamination, regulatory inspections, and potential recalls. Plaintiffs argue these warnings were generic and failed to capture the severity of Gateway’s deficiencies. The filings emphasized compliance with FDA cGMP but omitted the scale of remediation needed. Quarterly 10-Qs reiterated flat remediation costs, contradicting internal knowledge of escalating expenses. The lawsuit contends these omissions rendered the filings materially misleading.

Conclusion: Implications for Investors

The Perrigo case underscores the peril of relying on management assurances without scrutinizing operational realities. Investors allege they were misled by rosy narratives masking systemic deficiencies. For fund managers and class counsel, PRGO offers a cautionary tale: acquisitions framed as “strategic” can conceal costly liabilities. The broader lesson is clear — risk disclosures must be substantive, not boilerplate. As litigation unfolds, investors will watch closely for signals of accountability, governance reform, and potential settlement.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Freeport-McMoRan Inc. (FCX) Securities Lawsuit Update [November 26, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/fcx-alert-plus-banner.webp)

![Integer Holdings Corporation (ITGR) Securities Class Action Lawsuit Update [December 17, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/itgr-alert-plus-banner.webp)

![Sprouts Farmers Market, Inc. (SFM) Securities Class Action Lawsuit Update [December 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/sfm-alert-plus-banner.webp)