![Integer Holdings Corporation (ITGR) Securities Class Action Lawsuit Update [December 17, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/itgr-alert-plus-banner.webp)

Integer Holdings Corporation Did Not Miss a Quarter, It Missed a Curve

Case Name: West Palm Beach Firefighters' Pension Fund v. Integer Holdings Corporation et al.

Case No.: 1:25-cv-10251

Jurisdiction: U.S. District Court, Southern District of New York

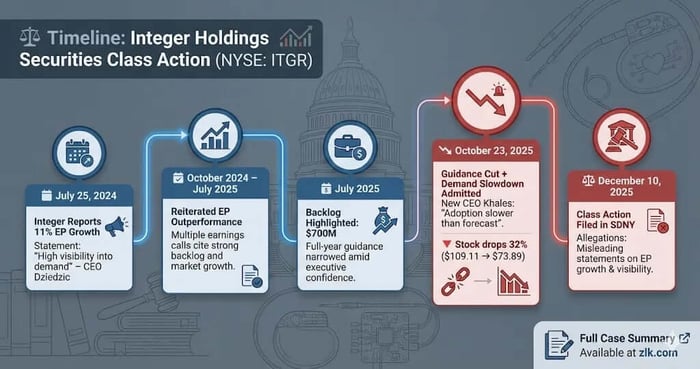

Filed on: December 10, 2025

Class Period: July 25, 2024 - October 22, 2025

Introduction

On December 10, 2025, a federal securities class action was filed against Integer Holdings Corporation and three senior executives, alleging that investors were misled about the company’s competitive position and demand outlook in the fast-growing electrophysiology market. The lawsuit centers on repeated public assurances that Integer’s electrophysiology, or EP, business was outgrowing the market, backed by what management described as “high visibility” into customer demand. According to investors, those statements masked a sustained deterioration in demand for key EP products—one that only surfaced when Integer abruptly cut guidance in October 2025, triggering a single-day stock collapse of more than 32 percent.

What followed was predictable. Analysts recoiled. Shareholders absorbed steep losses. And now, the company’s narrative of disciplined execution is being tested in court.

Backdrop and Business Context

Integer Holdings Corporation is a global contract development and manufacturing organization serving medical device companies, with a particular concentration in cardiac rhythm management and cardiovascular products. Roughly 60 percent of the company’s revenue comes from its Cardio & Vascular segment, which includes electrophysiology devices used to map and treat cardiac arrhythmias.

In the years leading up to the class period, the EP market underwent a technological shift as customers advanced pulse field ablation platforms—high-energy electrical pulse systems designed to treat atrial fibrillation. Integer positioned itself as a critical beneficiary of that transition, emphasizing its vertically integrated manufacturing footprint and participation across multiple steps of the EP procedure. Executives repeatedly described EP as a durable growth engine embedded within a broader cardiovascular platform.

That framing mattered. It shaped analyst models. It anchored guidance. And it set expectations that the company’s EP exposure was not merely cyclical, but structurally advantaged.

Promises Made vs. Reality

Beginning on July 25, 2024, Integer issued a steady cadence of public statements asserting that its EP business was outperforming the broader market.

On that date, the company reported second-quarter results and told investors that Cardio & Vascular sales rose 11 percent year-over-year, “driven by new product ramps in electrophysiology.” On the accompanying earnings call, CEO Joseph Dziedzic went further, stating that Integer was “confident in [its] ability to deliver strong sales growth given our high visibility to consumer demand” and that its electrophysiology business was growing at “1.5x the market growth rate” on a trailing four-quarter basis.

Those assurances continued across multiple quarters. In October 2024, February 2025, April 2025, and July 2025, executives reiterated that EP and structural heart products were growing faster than the market, that backlog provided strong demand visibility, and that any quarterly lumpiness reflected customer manufacturing schedules—not demand weakness.

According to the complaint, those statements omitted a critical counterweight: demand for at least two key EP devices was deteriorating, adoption was slower than forecast, and the supposed growth driver was already decelerating. Investors allege that management’s repeated claims of market outperformance and visibility lacked a reasonable basis given internal realities.

Timeline of Alleged Misconduct and Disclosures

The class period runs from July 25, 2024, through October 22, 2025.

Throughout that period, Integer reported double-digit growth in its Cardio & Vascular segment, highlighted EP product ramps, and reaffirmed guidance. In July 2025, the company even narrowed its full-year sales range, citing backlog of approximately $700 million as evidence of demand visibility.

The narrative unraveled on October 23, 2025.

Before markets opened, Integer cut its 2025 sales guidance and disclosed that it expected net sales growth of negative 2 percent to positive 2 percent in 2026. On the earnings call, newly appointed CEO Payman Khales acknowledged that sales of three new products were expected to decline in 2026, two of which were electrophysiology devices, and that “market adoption of these products has been slower than forecasted.” CFO Diron Smith added that the impact was now expected to continue into 2026, rather than being temporary.

The market reaction was swift and unforgiving.

Investor Harm and Market Reaction

On October 23, 2025, Integer’s stock fell $35.22 per share, declining more than 32 percent in a single trading session, from $109.11 to $73.89. Billions in market capitalization evaporated.

Analysts immediately recalibrated. Wells Fargo downgraded the stock, characterizing Integer’s fourth-quarter and 2026 guidance as “materially below the Street” and warning that any re-rating would require rebuilding investor confidence in management execution.

For investors who purchased during the class period—particularly those relying on management’s repeated claims of above-market EP growth—the disclosure functioned as a corrective event, revealing that the core growth thesis had been overstated.

Litigation and Procedural Posture

The case is styled West Palm Beach Firefighters’ Pension Fund v. Integer Holdings Corporation, et al., filed in the U.S. District Court for the Southern District of New York. The complaint asserts claims under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and Rule 10b-5.

Defendants include Integer Holdings Corporation and three executives: CEO Joseph Dziedzic, CFO Diron Smith, and COO-turned-CEO Payman Khales. The lawsuit alleges that defendants knowingly or recklessly made materially false statements about demand visibility, competitive positioning, and EP growth, and that the statutory safe harbor does not apply because the statements concerned then-existing conditions or were made with actual knowledge of their falsity.

The case is at the pleading stage, with motions practice expected to center on scienter, loss causation, and the adequacy of risk disclosures.

Shareholder Sentiment

Following the October 23, 2025 guidance cut and the resulting 32%+ stock drop, retail investor discussion on platforms like X (formerly Twitter) remained limited and scattered. Much of the visible activity consisted of unrelated promotional posts (e.g., spam inviting users to Discord groups for "target prices" or "next moves").

On Reddit, threads in communities like r/InsiderTradingAlerts highlighted post-drop insider activity, noting the CEO's purchase of approximately $200k in shares (a 16% increase in holdings) shortly after the plunge, framing it as a potential bullish signal amid the earnings reaction.

Broader expressions of frustration, betrayal, or sharp skepticism toward management's prior claims of "high visibility" and EP market outperformance were not prominently evident in public social media posts during the immediate aftermath. Discussion appeared muted relative to higher-volume stocks facing similar events.

Analyst Commentary

Following Integer Holdings Corporation's October 23, 2025 earnings release and guidance cut—which included lowered 2025 sales expectations and a preliminary 2026 outlook implying flat-to-negative growth—several sell-side analysts quickly revised their ratings and price targets downward.

Key actions included:

Wells Fargo downgraded the stock from Overweight to Equal Weight on October 24, 2025, slashing its price target from $132 to $80. Analysts noted limited visibility into affected products and questioned the abrupt shift in demand outlook.

Bank of America downgraded from Buy to Neutral on October 24, 2025, reducing its price target from $135 to $87, citing growth concerns tied to slower adoption of key electrophysiology and neuromodulation products.

Argus downgraded from Buy to Hold on October 24, 2025. Other firms, such as Citigroup, KeyCorp, and Raymond James, lowered price targets in the immediate aftermath, contributing to a broader consensus shift toward Hold ratings (7 Hold, 4 Buy as of mid-December 2025).

Commentary emphasized execution risk, a disconnect between prior management assurances of strong demand visibility and the magnitude of the slowdown, and the need for improved forecasting discipline before any re-rating. While some longer-term optimism remained around Integer's market position, near-term uncertainty dominated, with analysts highlighting that the revised guidance was "materially below" prior Street expectations.

SEC Filings & Risk Factors

Integer’s periodic filings during the class period included generalized risk disclosures regarding customer demand variability, product adoption cycles, and reliance on key customers. What investors allege was missing was specificity.

According to the complaint, filings failed to disclose that demand for certain EP devices was already deteriorating, that adoption timelines were slipping materially, and that EP growth was no longer tracking above market rates. As alleged, these omissions rendered contemporaneous risk disclosures inadequate because they framed risks as hypothetical when adverse trends were already unfolding.

That distinction—between possible risk and present reality—now sits at the heart of the case.

Conclusion: Implications for Investors

The Integer lawsuit is not about a missed forecast. It is about narrative control.

For investors, the case underscores a familiar lesson in growth-driven sectors: repeated claims of “visibility,” “outperformance,” and “pipeline strength” warrant scrutiny when adoption curves are opaque and customer behavior shifts quietly. Backlog can reassure. It can also mislead.

For the market, the case reinforces the legal boundary between optimism and omission. When companies speak confidently about demand and competitive position, they assume an obligation to disclose known facts that undermine those claims.

This is not a closing argument. It is a reckoning. And now, investors are asking whether the story they were told ever matched the one management was living with.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Perrigo Company PLC (PRGO) Securities Class Action Update [December 2, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/prgo-alert-plus-banner.webp)

![Sprouts Farmers Market, Inc. (SFM) Securities Class Action Lawsuit Update [December 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/sfm-alert-plus-banner.webp)

![F5, Inc. (FFIV) Securities Class Action Lawsuit Update [December 22, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/ffiv-alert-plus-banner.webp)