![Nutex Health, Inc. (NUTX) Securities Class Action Lawsuit Update [November 28, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/nutx-alert-plus-banner.webp)

When Revenue Depends on Arbitration, the Clock is Always Ticking

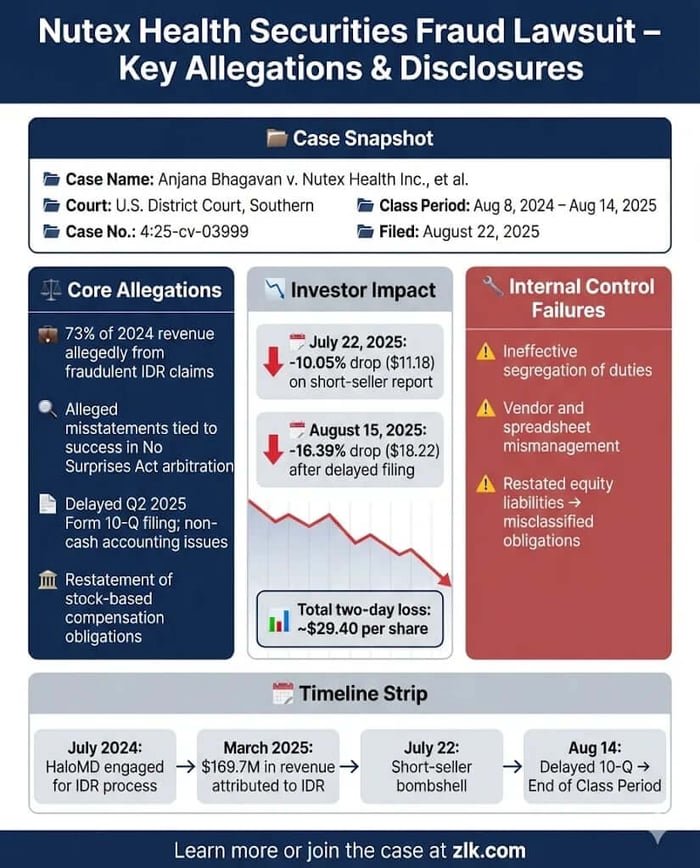

Caption: Bhagavan v. Nutex Health Inc., et al.

Case No.: 4:25-cv-03999

Jurisdiction: U.S. District Court, Southern District of Texas

Filed on: August 22, 2025

Class Period: August 8, 2024 – August 14, 2025

Introduction

Red Cat said it was ready to soar. It wasn’t. Nutex Health Inc., a physician-led healthcare services company, is now facing a securities class action lawsuit that lays bare a narrative where staggering revenue growth—73% of its 2024 increase—is allegedly tied to a coordinated scheme to defraud insurance carriers. This is a lawsuit about an innovative revenue stream that may have been nothing more than an unsustainable legal artifice, one that abruptly failed when the accounting foundation under it crumbled.

The case, Bhagavan v. Nutex Health Inc., et al., alleges that Nutex and its top executives—CEO Thomas T. Vo, CFO Jon C. Bates, and President Warren Hosseinion—made materially false and misleading statements to investors throughout the Class Period, from August 8, 2024 to August 14, 2025. The core of the complaint centers on Nutex’s use of a third-party vendor, HaloMD, to pursue out-of-network claims under the federal No Surprises Act, or NSA, via the Independent Dispute Resolution, or IDR, process. A bombshell short-seller report triggered the initial sell-off on July 22, 2025, alleging the IDR success was fraudulent. Days later, the final disclosure of the Class Period—a delayed 10-Q filing citing non-cash accounting adjustments and restatement of stock-based compensation—confirmed that the company’s internal controls were insufficient to even book its financial obligations correctly. The resulting stock drops cost investors significant capital, leading to this legal reckoning.

Backdrop and Business Context

Nutex Health is a physician-led company operating three divisions: a hospital division spanning 24 facilities in 11 states, a population health management division, and real estate. The company entered the public markets not through a traditional offering, but via a reverse merger in April 2022. This is a path often fraught with a heightened risk profile, allowing companies to bypass the rigorous scrutiny of a conventional initial public offering.

Crucially, Nutex operates primarily as an out-of-network provider, generating revenue from third-party payors like commercial insurance. This model was fundamentally challenged by the No Surprises Act, enacted in December 2020, which curtailed the practice of "balance billing," where providers could bill patients for the difference between the billed charge and the insurer's payment. The NSA forced providers like Nutex to utilize the IDR process to resolve payment disputes, essentially setting up an arbitration system to determine fair out-of-network payment amounts.

Initial results were difficult. In March 2023, the company reported its average payment by insurers for emergency services had declined by approximately 30%. To pivot, Nutex engaged HaloMD, a third-party IDR vendor, in July 2024 to "assist in the recovery of certain out of network claims." This engagement became the central engine of the company’s growth, driving $169.7 million in incremental revenue for 2024, or 73.1% of the total revenue increase.

Promises Made vs. Reality

Throughout the Class Period, Nutex executives repeatedly championed the success of their IDR strategy while simultaneously assuring the market they were remediating known deficiencies in internal controls. The public statements painted a picture of savvy operators successfully navigating new federal legislation.

On the August 9, 2024 earnings call, CEO Thomas T. Vo stated, "We are pleased to report another excellent quarter for Nutex Health [...]." He emphasized the arbitration success: "We believe that there is a lot of potential incremental value and revenue to be gained from arbitration [...] In recent articles and public data, we are seeing that providers are prevailing 70% to 80% of the time in arbitration." Later, in May 2025, Defendant Vo claimed an "80% plus win rate" in arbitration, resulting in facility collections increasing by between 200% to 300% compared to initial insurance payments.

The reality, as later alleged, was a sophisticated scheme. The Blue Orca Report claimed that the "dramatically lucrative results" achieved by the IDR vendor for clients like Nutex were the product of a "coordinated fraudulent scheme to steal millions of dollars from insurance companies." The short-seller referenced "[b]ombshell [l]awsuits" filed by major insurance companies against the vendor, alleging they were "flooding the arbitration system with thousands of claims that they knew at the time of submission to be ineligible."

Further, despite repeated public assurances in their Form 10-Q filings that the company had "started the process of designing and implementing effective internal control measures to remediate the reported material weaknesses," including engaging an accounting firm and implementing a new enterprise-wide system, the internal controls were allegedly so ineffective that the company could not even classify its own financial obligations correctly. The restatement later proved the assurances of effective remediation to be overstated, at best.

Timeline of Alleged Misconduct and Disclosures

July 2024: Nutex engages HaloMD, a third-party IDR vendor, to assist in recovering out-of-network claims through the NSA's IDR process.

August 8, 2024: Nutex issues its Q2 2024 financial results, with executives touting revenue growth and the success of the IDR arbitration process. The company simultaneously represents it has "started the process of designing and implementing effective internal control measures to remediate the reported material weaknesses." This date marks the beginning of the Class Period.

February 5, 2025: Vo issued an NSA arbitration update claiming proactive arbitration had yielded "positive results" due to securing "rightful payments" and presenting an overall message of continued success.

March 31, 2025: Nutex reports Q4 and full-year 2024 results, attributing approximately $169.7 million, or 73.1%, of its total revenue increase for the year to the IDR arbitration process.

May 14, 2025: On the Q1 2025 earnings call, CEO Vo claims an "80% plus win rate" in IDR arbitration, resulting in facility collections increasing 200% to 300% compared to initial insurer payments.

July 22, 2025: Blue Orca Capital issues a short report, alleging Nutex’s IDR-driven revenue is based on a "coordinated fraudulent scheme" by its vendor, HaloMD, to steal from insurance companies. Nutex’s stock price falls $11.18 per share, a 10.05% drop, closing at $100.01.

July 24, 2025: Nutex issues a press release, stating it "strongly disagrees with the allegations" and expects to provide an update in its upcoming Form 10-Q filing.

August 14, 2025: After market close, Nutex announces a delay in filing its Q2 2025 Form 10-Q, citing "non-cash accounting adjustments related to the treatment of stock based compensation obligations." This date marks the end of the Class Period.

August 15, 2025: Nutex's stock price falls $18.22 per share, a 16.39% drop, closing at $92.91, as the company failed to rebut the fraud allegations and confirmed its internal accounting problems.

August 21, 2025 (Post-Class Period): Nutex files an 8-K confirming the need to restate previously issued financial statements because certain non-cash obligations were "treated [...] as equity rather than liabilities."

Investor Harm and Market Reaction

The damages sustained by investors were both sudden and severe, triggered by two specific and interconnected corrective disclosures. The first blow was the accusation of fraudulent practices driving the company’s revenue, a claim that struck at the heart of Nutex's vaunted growth story. The second blow was the confirmation that the company's internal accounting infrastructure was inadequate, which increased the risk of the revenue being uncollectible and the financial statements themselves being inaccurate.

The immediate market reaction to the Blue Orca Report on July 22, 2025, wiped out over one-tenth of the stock’s value, representing a $11.18 per share loss. This was an unambiguous signal that the market took the short-seller's claims of an "unsustainable" business model seriously. The second, more punishing drop followed the company's failure to deliver the promised rebuttal in its Form 10-Q filing. Instead of clarity, investors received the announcement of a delayed filing and the citation of critical accounting issues, leading to a 16.39% single-day decline, a loss of $18.22 per share. This two-stage collapse reflects the compounding nature of the allegations: the revenue was allegedly fraudulent, and the company’s accounting systems were too weak to properly track its basic financial liabilities.

Litigation and Procedural Posture

The class action, Anjana Bhagavan v. Nutex Health Inc., et al., was filed in the U.S. District Court for the Southern District of Texas under Civil No. 4:25-cv-03999.

The asserted legal claims are brought under the Securities Exchange Act of 1934:

Section 10(b) and Rule 10b-5: Against all Defendants (Nutex Health Inc., Thomas T. Vo, Jon C. Bates, and Warren Hosseinion) for making untrue statements of material facts, omitting material facts, and employing a scheme to defraud investors in connection with the purchase or sale of securities.

Section 20(a): Against the Individual Defendants (Vo, Bates, and Hosseinion) as "controlling persons" of Nutex, liable for the primary violations committed by the company under Section 10(b).

The Complaint details significant scienter allegations (the intent to deceive, manipulate, or defraud) by asserting that the Individual Defendants had actual knowledge of the misleading nature of the statements or acted with reckless disregard for the truth. This stems from their senior positions, which gave them access to the non-public information about the IDR scheme and the failure of their internal controls, which they then failed to disclose. The lawsuit further highlights the dramatic dependence of the company's financial performance on the arbitration process, emphasizing that management would have been acutely aware of the risk profile tied to the alleged fraudulent scheme. There is no information in the complaint regarding insider sales or confidential witness statements, leaving the scienter argument to rely on the inference of management's knowledge based on their control and the materiality of the misstatements.

Shareholder Sentiment

The sentiment from retail investors and fund managers following the dual disclosures moved from cautious optimism to a fierce, almost existential, despair. Prior to the Blue Orca Report, the narrative was one of a smart healthcare operator successfully exploiting a newly enacted regulatory mechanism—the IDR process—to secure high reimbursement rates. This narrative fostered a sense of tactical superiority.

The initial short report shattered that image, driving conversations on platforms like Stocktwits and Reddit to center on accusations of systemic deceit. The language became visceral: "This isn't just bad revenue; it's a house of cards scam. Management needs to be held accountable for running a company that was basically a legal racket" was a representative sentiment. The subsequent delay of the Form 10-Q, which should have been the definitive rebuttal, instead became the catalyst for panic. "They can't even get the basic accounting right? Liabilities as equity? We're talking about a return to penny stock status, exactly what the shorts predicted," became a common refrain. The shift in opinion was not gradual; it was a violent swing from "arbitration heroes" to "governance zero," reflecting the emotional stakes involved when alleged fraud touches a company’s fundamental accounting practices.

Analyst Commentary

Professional commentary mirrored the abrupt change in the investment thesis, moving rapidly from a growth-oriented "Accumulate" stance to a highly cautious "Underperform" or "Sell" rating. Before the corrective disclosures, analyst notes likely focused on the impressive year-over-year growth numbers—particularly the massive incremental revenue attributed to the IDR process—using terms like "strong operational execution" and "successful regulatory navigation."

The July 22, 2025 short report was the first inflection point, prompting a swift re-evaluation. Analysts quickly downgraded ratings and slashed target prices, citing "governance concerns" and a "fundamentally elevated risk profile." One can imagine a sudden suspension of coverage or a shift to "Hold" until the company could either rebut the fraud claims or successfully file its delayed financials. The August 15, 2025 revelation of the 10-Q delay and the non-cash accounting adjustment—misclassifying stock-based compensation as equity instead of a liability—forced a second, more severe round of downgrades. This confirmation of internal control weaknesses, which the company had repeatedly claimed to be remediating, fundamentally undermined confidence. Commentaries likely pivoted to "Loss Causation Event" territory, with analysts emphasizing the "uninvestable" nature of a stock whose core revenue stream is in legal question and whose internal controls necessitate a restatement of fundamental obligations.

SEC Filings & Risk Factors

The company’s quarterly reports, specifically the Q2 2024 and Q3 2024 Form 10-Qs, contained the seeds of the later disaster, both in what they celebrated and what they warned against. The filings heavily featured the success of the IDR strategy, representing it as a sustainable revenue source and a key driver of growth.

However, these same filings consistently disclosed material weaknesses in the company's internal control over financial reporting. The company’s acknowledgments included:

Ineffective controls over logical access, program change management, and vendor management.

Business process controls lacking proper segregation of duties between preparer and reviewer.

Ineffective controls over the completeness and accuracy of information included in key spreadsheets supporting the financial statements.

While Nutex repeatedly assured investors they were "designing and implementing effective internal control measures to remediate" these issues, the August 21, 2025 Form 8-K effectively contradicted this narrative. That post-Class Period filing confirmed the Audit Committee's conclusion that prior financial statements needed to be restated because non-cash obligations related to under-construction hospitals were incorrectly treated as equity rather than liabilities. This is a severe accounting failure, pertinent to the lawsuit's allegations that the company overstated its ability to remediate these very weaknesses and, as a result, improperly calculated its stock-based compensation obligations.

Conclusion: Implications for Investors

The Nutex case is a clinical lesson in recognizing red flags that transcend the simple promise of explosive growth. It illustrates the danger of a business model where a disproportionate share of revenue—in this case, over 73% of the growth—is generated by exploiting regulatory arbitration processes. For investors, any business heavily reliant on a single, newly adopted, legally contentious mechanism should be viewed with extreme skepticism. That’s a highly volatile form of income; it’s not operations.

The broader relevance for the market, particularly for companies that went public via alternative routes like a reverse merger, is the fragility of accounting controls. The true red flag here was not just the IDR strategy, but the repeated disclosure of "material weaknesses" in internal controls, which the company’s management repeatedly assured the market they were fixing. The failure to correctly classify a basic obligation—equity versus liability—proved that the remediation efforts were, at best, a performance, and the underlying financial reporting was unreliable. This isn’t a closing argument. It’s a reckoning. When the engine of growth is questionable and the accounting is broken, investors should not wait for the inevitable stock collapse.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Sallie Mae (SLM) Securities Class Action Lawsuit Update [December 31, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/slm-alert-plus-banner.webp)

![Klarna Group Plc (KLAR) Securities Class Action Lawsuit Update [January 1, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/klar-alert-plus-banner.webp)

![Coupang, Inc. (CPNG) Securities Class Action Lawsuit Update [December 30, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/cpng-alert-plus-banner.webp)