![Sallie Mae (SLM) Securities Class Action Lawsuit Update [December 31, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/slm-alert-plus-banner.webp)

Investors Allege Delinquency Risks Were Misrepresented

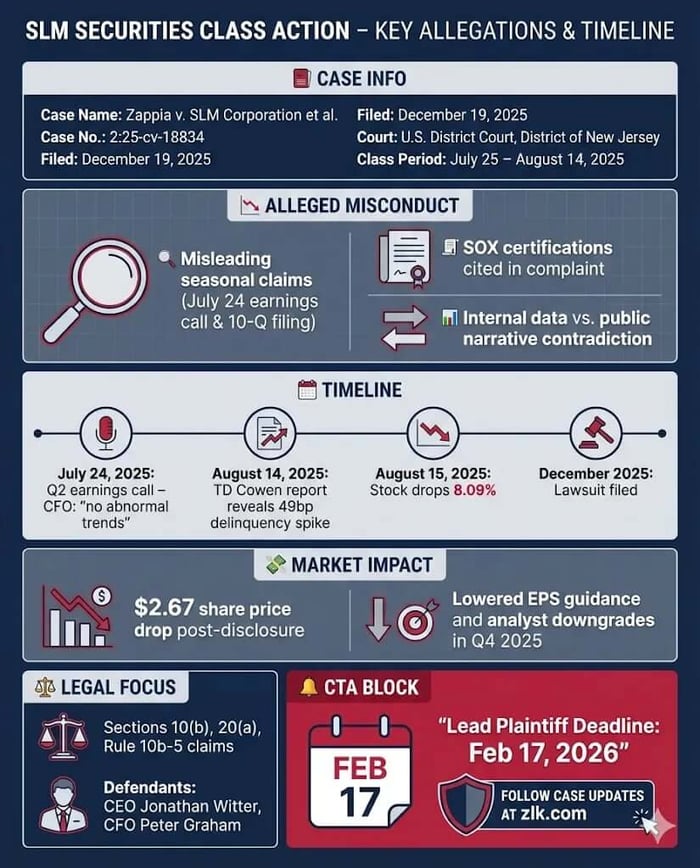

Case Name: Zappia v. SLM Corporation a/k/a Sallie Mae, et al.

Case No.: 2:25-cv-18834

Jurisdiction: U.S. District Court, District of New Jersey

Filed on: December 19, 2025

Class Period: July 25, 2025 - August 14, 2025

Introduction

Sallie Mae said its credit trends were seasonal. Investors allege they were structural.

In December 2025, a federal securities class action was filed against SLM Corporation, better known as Sallie Mae, accusing the company and two senior executives of misleading investors about rising delinquency risks in its private education loan portfolio. The case centers on a short but volatile class period in the summer of 2025, when executives repeatedly characterized worsening loan performance as routine—only for outside analysis to suggest something far more serious. When that contradiction surfaced, the stock fell sharply. Now, investors are fighting back.

Backdrop and Business Context

SLM Corporation operates almost entirely around one product: private education loans. The company originates and services loans to students and families, and its profitability depends on repayment behavior long after graduation. Delinquency trends are not a side metric. They are the metric.

SLM classifies loans as “in repayment” once borrowers begin making interest-only, fixed, or full principal-and-interest payments. Loans reaching 120 days delinquent are charged off. Servicing delinquent borrowers is materially more expensive than servicing current ones. As a result, even modest changes in early-stage delinquency can ripple through earnings, capital planning, and long-term guidance.

By mid-2025, investors were watching these numbers closely. According to the complaint, management knew that. And spoke accordingly.

Promises Made vs. Reality

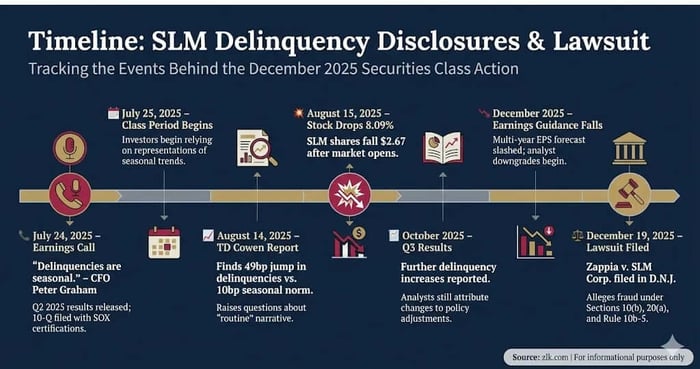

During a July 24, 2025 earnings call, Sallie Mae’s Chief Financial Officer Peter Graham assured analysts that rising delinquencies were “following the normal seasonal trends that we would expect in the business.” He emphasized confidence in the company’s loan modification programs and stated that management had not seen “any sort of abnormal trends.”

The same message appeared in writing. Sallie Mae’s Q2 2025 Form 10-Q attributed higher delinquency metrics primarily to “changes and refinements” in loss mitigation programs and touted “enhanced” modification efforts. The filing included Sarbanes-Oxley certifications from senior executives affirming that the report contained no material misstatements or omissions.

Investors allege those assurances omitted a critical fact: early-stage delinquencies were rising sharply and out of line with seasonal norms. According to the complaint, internal data already reflected this divergence when the statements were made.

Timeline of Alleged Misconduct and Disclosures

The class period begins on July 25, 2025, immediately after Sallie Mae released Q2 results and held its earnings call. Over the following weeks, the market relied on management’s framing: delinquencies were manageable, expected, and under control.

That narrative cracked on August 14, 2025. That evening, TD Cowen issued a report analyzing Sallie Mae’s July data. The firm found that overall delinquencies had risen 49 basis points month-over-month—far worse than the roughly 10-basis-point seasonal increase typically seen in July. The increase was driven largely by early-stage delinquencies.

The next trading day, Sallie Mae’s stock fell $2.67 per share, an 8.09% drop. Investors allege this decline reflected the market’s first real look at the truth.

Investor Harm and Market Reaction

According to the complaint, shareholders purchased Sallie Mae securities at artificially inflated prices during the class period, relying on management’s characterization of credit trends. When the TD Cowen report contradicted those assurances, the market adjusted abruptly.

The August 2025 decline was not the end of the story. In October, Sallie Mae reported Q3 results showing delinquency rates continuing to rise. Analysts expressed concern that credit quality was deteriorating. By December, the company issued multi-year earnings guidance that fell well below consensus, triggering another sharp stock drop.

Investors allege these later disclosures confirmed what had already begun to surface in August: the risks were real, known, and earlier than disclosed.

Litigation and Procedural Posture

The lawsuit, Zappia v. SLM Corporation, et al., is pending in the U.S. District Court for the District of New Jersey. The complaint asserts claims under Sections 10(b) and 20(a) of the Securities Exchange Act and Rule 10b-5.

Defendants include Sallie Mae itself, CEO Jonathan Witter, and CFO Peter Graham. Plaintiffs allege that the individual defendants had access to real-time delinquency data and exercised control over public statements, SEC filings, and earnings calls.

Scienter allegations focus on the importance of delinquency metrics to Sallie Mae’s core business, the timing of executive statements, and the contradiction between management’s assurances and contemporaneous data trends later identified by analysts.

Shareholder Sentiment

Searches across social media platforms, including X (formerly Twitter) and Reddit, reveal limited direct discussion from retail investors specifically addressing the August 2025 TD Cowen report on Sallie Mae's delinquency trends or the subsequent securities class action lawsuit filed in December 2025.

Most online commentary on Sallie Mae (SLM) continues to focus on borrower experiences with private student loans, such as high interest rates, repayment challenges, and occasional fraud concerns. Posts about the company as an investment or its credit quality issues are sparse, with no widespread evidence of a rapid shift in sentiment following the August disclosure.

The emergence of the class action lawsuit has prompted some promotional posts on X highlighting investor alerts and deadlines (e.g., February 17, 2026, for lead plaintiff motions), but these appear driven by law firm announcements rather than organic retail investor frustration.

Overall, while the allegations suggest potential management mischaracterization of risks, public social media sentiment among shareholders has not shown a pronounced or permanent change in tone as of late December 2025. Broader skepticism toward the student loan industry persists, but it predates and is not uniquely tied to these events.

Analyst Commentary

Analyst coverage of Sallie Mae (SLM) in 2025 initially focused on stable credit trends and growth potential, but shifted markedly following the company's December 2025 investor forum, where multi-year earnings guidance fell well below consensus expectations due to higher planned expenses for new initiatives and balance sheet transitions.

The August 14, 2025 TD Cowen report highlighting a sharp month-over-month rise in delinquencies (up 49 basis points, versus a typical seasonal 10 basis points) drew attention to potential credit quality concerns, though direct analyst downgrades tied to this specific disclosure were limited in public reports (Seeking Alpha, Investing.com).

Following Q3 2025 results in October, commentary remained generally constructive, noting modest delinquency increases largely attributed to policy changes in loan modifications rather than fundamental deterioration, with stabilized roll rates and strong origination growth (StockStory, Investing.com earnings transcripts).

The pivotal shift occurred in early December 2025 after SLM outlined a medium-term outlook implying significantly lower EPS for 2026-2027 amid investments in partnerships (e.g., with KKR) and preparations for federal loan reforms. This prompted a wave of downgrades and price target cuts:

Morgan Stanley downgraded from Overweight to Equalweight, citing higher expense outlook and reduced EPS estimates.

Compass Point double-downgraded from Buy to Sell, slashing its target from $35 to $23 on a "major reset" in earnings.

Wells Fargo cut its target from $35 to $30; Deutsche Bank from $42 to $37.

Overall, credit quality has become a sustained point of scrutiny, evolving from a manageable issue tied to seasonal and policy factors into a broader concern amid the company's strategic pivot toward capital-light growth. The consensus has cooled, with the through-line now emphasizing near-term earnings pressure and execution risks on new ventures (Seeking Alpha analyst articles, StockStory reports).

SEC Filings & Risk Factors

The complaint places particular emphasis on Sallie Mae’s Q2 2025 Form 10-Q. Plaintiffs allege the filing failed to disclose known adverse trends as required under Item 303 of Regulation S-K. Instead, the company attributed higher delinquencies to benign program refinements and emphasized enhanced mitigation efforts.

Plaintiffs argue that these disclosures, combined with affirmative statements about seasonality, created a misleading picture of risk. The inclusion of SOX certifications is cited as further evidence that executives stood behind the accuracy of the narrative presented to investors.

Conclusion: Implications for Investors

This case is not about a missed forecast. It is about timing, disclosure, and trust.

For investors, the alleged lesson is familiar but sharp: when a company’s business hinges on a single operational metric, characterizations matter as much as numbers. Seasonal explanations can soothe markets—until they don’t.

For Sallie Mae shareholders, the lawsuit asks whether rising delinquencies were framed as routine when they were anything but. The court will decide the legal outcome. The market has already rendered its verdict on credibility.

Now, investors are fighting back.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Nutex Health, Inc. (NUTX) Securities Class Action Lawsuit Update [November 28, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/nutx-alert-plus-banner.webp)

![Klarna Group Plc (KLAR) Securities Class Action Lawsuit Update [January 1, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/klar-alert-plus-banner.webp)

![Coupang, Inc. (CPNG) Securities Class Action Lawsuit Update [December 30, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/cpng-alert-plus-banner.webp)