![Klarna Group Plc (KLAR) Securities Class Action Lawsuit Update [January 1, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/klar-alert-plus-banner.webp)

Inside the BNPL Reckoning After the IPO

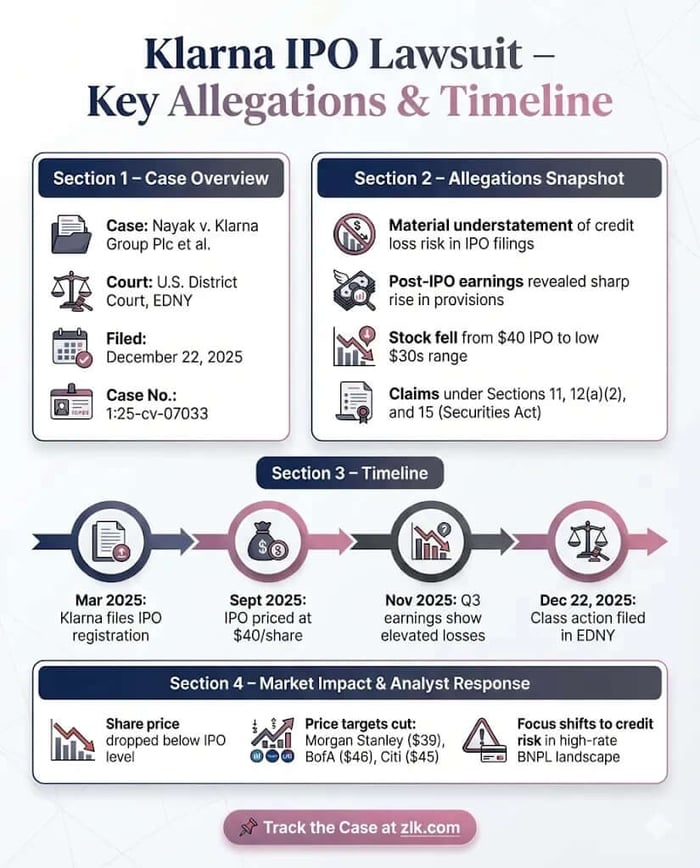

Case Name: Nayak v. Klarna Group Plc et al.

Case No.: 1:25-cv-07033

Jurisdiction: U.S. District Court, Eastern District of New York

Filed on: December 22, 2025

Introduction

In December 2025, a federal securities class action was filed against Klarna Group plc following its highly anticipated U.S. IPO, accusing the company, its executives, and its underwriters of selling confidence while quietly carrying mounting consumer credit risk. The lawsuit targets Klarna’s September 2025 offering and alleges that the Registration Statement materially understated the likelihood that credit loss provisions would surge shortly after the IPO. When Klarna’s first post-IPO earnings revealed exactly that, the stock dropped. Now, investors are asking whether the damage was embedded from day one.

Backdrop and Business Context

Klarna is a global payments company built around “buy now, pay later” financing. Its products—Pay in Full, Pay Later, and longer-dated “Fair Financing” installment loans—sit at the intersection of e-commerce, consumer credit, and behavioral finance. The company expanded aggressively into the United States beginning in 2019, recalibrating its risk appetite to fuel growth. That strategy worked. Gross merchandise volume climbed. Revenue followed.

But the model carried a tradeoff. Klarna increasingly extended credit to younger, less-established consumers, often for discretionary purchases. By the time Klarna went public in September 2025 at $40 per share, its U.S. lending book had become central to the growth narrative—and, according to investors, central to the risk that was not fully disclosed.

Promises Made vs. Reality

In its IPO prospectus, Klarna framed underwriting as a core strength. Management emphasized proprietary data, real-time decisioning, and declining credit losses in the U.S. market. The filings acknowledged risk in theory but stressed control in practice. Investors were told that earlier spikes in losses had been addressed through tighter underwriting, higher down payments, and improved models.

The complaint alleges that these assurances omitted a critical reality: Klarna’s loan portfolio depended heavily on consumers experiencing financial stress and willing to borrow at high interest rates for everyday purchases. According to the lawsuit, the Registration Statement understated how quickly provisions for credit losses were likely to rise and failed to disclose that a material increase was already reasonably foreseeable at the time of the offering.

Timeline of Alleged Misconduct and Disclosures

The story unfolds quickly. Klarna filed its initial registration materials in March 2025 and completed its IPO in September. Two months later, in November 2025, the company reported its first earnings as a public issuer. Revenue beat expectations. Losses did not. Klarna disclosed a sharp increase in provisions for credit losses, driven in part by longer-duration installment loans. Bloomberg and Barron’s coverage focused on the same theme: growth was intact, but the credit bill was coming due.

The market reacted immediately. Klarna shares fell well below the IPO price in the days following the earnings release, erasing billions in market value and reframing the company’s risk profile overnight.

Investor Harm and Market Reaction

Plaintiffs allege that investors who purchased shares in the IPO paid $40 for securities that soon traded in the low $30s. The decline coincided directly with Klarna’s disclosure of higher-than-expected credit provisions and net losses. Analysts recalibrated expectations, shifting focus from revenue momentum to loan performance, delinquency risk, and the sustainability of BNPL economics in a higher-rate environment.

Loss causation, investors argue, is straightforward. The omitted risk materialized. The stock repriced.

Litigation and Procedural Posture

The action, filed in the U.S. District Court for the Eastern District of New York, asserts claims under Sections 11, 12(a)(2), and 15 of the Securities Act. Defendants include Klarna, senior executives and directors who signed the Registration Statement, and a broad syndicate of underwriters. Because the case arises under the Securities Act, plaintiffs are not required to plead scienter. The theory is negligence: that the offering documents failed to disclose known trends and reasonably likely adverse outcomes related to credit losses.

The case is at an early stage. No motion to dismiss has yet been resolved. But the allegations place Klarna squarely within a growing line of IPO cases focused on risk disclosure rather than outright fraud.

Shareholder Sentiment

Retail investor sentiment toward Klarna flipped from bullish hype to outright frustration in the wake of the November 2025 earnings miss, with social media threads exploding over perceived disclosure lapses and the fragility of the BNPL model. On Stocktwits, users vented that Klarna's IPO was a trap, capturing the raw sting of the post-earnings plunge. Reddit's r/investing subreddit saw similar backlash, where a top post lamented classic pump and dump vibes, and sparking debates on whether the prospectus buried red flags in legalese.

Overall, the online chorus evolved from pre-IPO excitement about Klarna's sleek branding to a defensive, accusatory roar, zeroing in on the grievance that the "growth story" masked an imminent credit reckoning. Investors didn't just feel burned—they felt baited.

Analyst Commentary

Sell-side analysts adopted a cautiously optimistic tone following Klarna's November 2025 post-IPO earnings, acknowledging robust revenue growth and U.S. momentum while highlighting elevated credit provisions as a near-term headwind to profitability and margin stability. Bloomberg noted that the surge in longer-duration loans drove record revenue but triggered higher provisions, with CEO Sebastian Siemiatkowski describing the increase as an "expected profit lag" from rapid Fair Financing expansion. Reuters reported that Q3 revenue beat estimates at $903 million, fueled by U.S. growth, though provisions rose sharply amid the shift to interest-bearing products.

Several firms trimmed price targets in response, citing sensitivity to borrower stress, loan duration, and the need for disciplined growth-credit balance. Morgan Stanley lowered its target to $39 from $43, maintaining an Equal-Weight rating and flagging ongoing credit concerns despite solid top-line results. BofA Securities reduced its target to $46 from $51 while keeping a Buy rating, pointing to credit growth worries and in-line Q4 guidance as reasons for caution. UBS cut to $46 from $48 (Buy maintained), Citigroup to $45 from $58 (Buy), and JPMorgan to $45 from $50 (Overweight), reflecting uncertainty around future provisioning in a higher-rate environment.

Consensus remains constructive, with most analysts viewing Klarna's revenue strength and market leadership as intact, but confidence in near-term margin recovery has moderated amid macro sensitivities and portfolio maturation risks.

SEC Filings & Risk Factors

Klarna’s prospectus contained extensive risk disclosures about underwriting, credit losses, and economic conditions. The lawsuit does not argue that risks were entirely absent. Instead, it alleges that they were framed as hypothetical when, in reality, adverse trends were already unfolding. Under SEC rules, known trends and uncertainties that are reasonably likely to impact financial results must be disclosed. Investors claim Klarna crossed that line—describing “if” and “could” where “was” and “would” were required.

Conclusion: Implications for Investors

This case is not about whether BNPL works. It is about timing, framing, and disclosure. IPO investors rely on offering documents to understand not just what might go wrong, but what management already sees coming. Klarna’s lawsuit underscores a familiar lesson: growth stories built on consumer credit are only as strong as the assumptions beneath them. When those assumptions crack, markets respond quickly. Now, investors are fighting back.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Agilon Health, Inc. (AGL) Securities Class Action Lawsuit Update [January 7, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/agl-alert-plus-banner.webp)

![Nutex Health, Inc. (NUTX) Securities Class Action Lawsuit Update [November 28, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/nutx-alert-plus-banner.webp)

![Sallie Mae (SLM) Securities Class Action Lawsuit Update [December 31, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/slm-alert-plus-banner.webp)