![Fermi Inc. (FRMI) Securities Class Action Lawsuit Update [January 8, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/frmi-alert-plus-banner.webp)

Inside the Project Matador Collapse

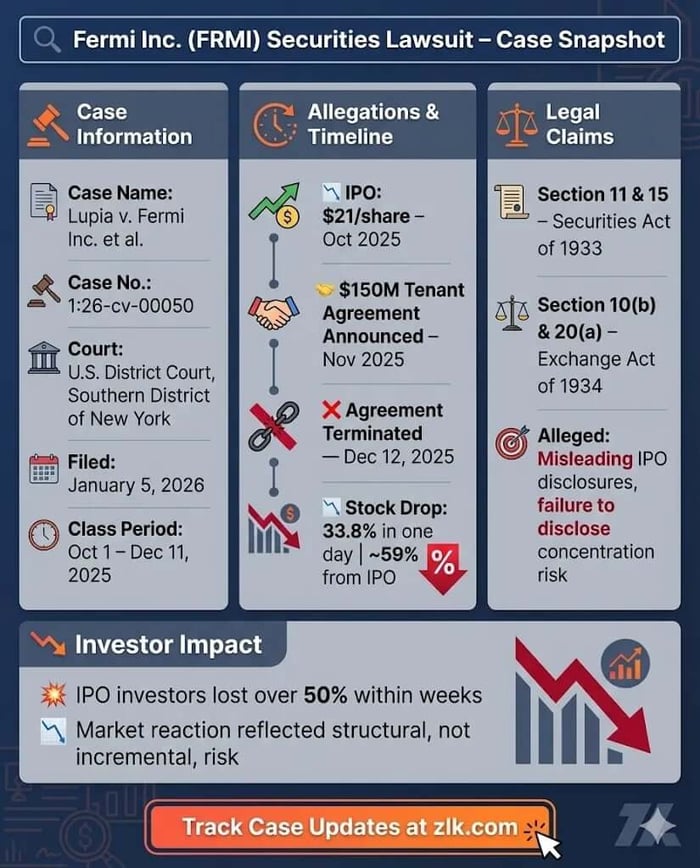

Case Name: Lupia v. Fermi Inc. et al.

Case No.: 1:26-cv-00050

Jurisdiction: U.S. District Court, Southern District of New York

Filed on: January 5, 2026

Class Period: October 1, 2025 - December 11, 2025 (IPO Date: October 2025)

Introduction

Fermi Inc. sold investors a vision of power without limits. Nuclear-backed energy campuses. Grid-independent AI infrastructure. Tenant demand so strong it could finance construction before a single data hall came online. By December 2025, that vision cracked.

A federal securities class action now pending in the U.S. District Court for the Southern District of New York accuses Fermi Inc. (NASDAQ: FRMI) and its executives of overstating tenant demand and understating the fragility of the company’s financing model tied to its flagship Project Matador development. The lawsuit alleges that when a single tenant terminated a $150 million Advance in Aid of Construction agreement, the market learned how concentrated—and how vulnerable—Fermi’s business really was.

The stock fell sharply. Investors followed. Now, the case tests whether Fermi’s IPO disclosures crossed the line from ambition into misrepresentation.

Backdrop and Business Context

Fermi Inc. describes itself as an energy and artificial intelligence infrastructure company structured as a real estate investment trust. At the time of its October 2025 initial public offering, the company had no operating history and no historical revenue. Its value proposition rested almost entirely on Project Matador—a proposed multi-phase energy campus in Texas designed to power hyperscale AI workloads using a mix of nuclear, natural gas, solar, and battery resources.

The IPO priced at $21.00 per share and raised approximately $745.7 million in net proceeds. Investors were told those funds, combined with tenant prepayments and project-level financing, would be sufficient to carry the company through early construction phases. The model depended on momentum—leases executed, prepayments collected, infrastructure financed in sequence.

That sequencing mattered. According to the complaint, it was also far less secure than investors were led to believe.

Promises Made vs. Reality

In its Registration Statement and Prospectus, Fermi repeatedly emphasized tenant demand and early commercial validation. The company disclosed that it had entered into a non-binding letter of intent with an “investment-grade” first tenant and was in “advanced discussions with a select group of foundational anchor tenants.”

Critically, Fermi also told investors that tenant prepayments were expected to fund “100% of the funding for our long lead-time items” upon execution of lease agreements. Liquidity disclosures reinforced that theme, stating that planned near-term funding sources—including tenant prepayments—would support operations for at least twelve months.

What investors were not told, plaintiffs allege, was how concentrated that funding really was. According to the complaint, Project Matador’s near-term viability depended overwhelmingly on a single tenant’s commitment—and on a $150 million Advance in Aid of Construction agreement that could be terminated before any funds were drawn.

When that agreement collapsed, the gap between the narrative and the structure became visible.

Timeline of Alleged Misconduct and Disclosures

The Exchange Act class period begins on October 1, 2025, when Fermi’s common stock began trading following the IPO. The complaint separately challenges alleged misstatements and omissions in the IPO registration statement under the Securities Act.

In November 2025, the company issued a shareholder letter and investor presentation highlighting the execution of the $150 million Advance in Aid of Construction agreement with its first tenant, describing it as a “pivotal milestone” that strengthened alignment and advanced the parties toward a long-term lease.

On December 12, 2025, before the market opened, Fermi disclosed that the first tenant had terminated the Advance in Aid of Construction agreement after the exclusivity period expired. No funds had been drawn. The company stated it was pursuing discussions with other potential tenants, but the damage was immediate.

That day, Fermi’s stock fell $5.16 per share—approximately 33.8 percent—on heavy trading volume. By the time the lawsuit was filed in January 2026, shares had traded as low as $8.59, representing a decline of roughly 59 percent from the IPO price.

Investor Harm and Market Reaction

The complaint ties investor losses directly to the December 12 disclosure. Plaintiffs allege that Fermi’s securities traded at artificially inflated prices throughout the class period because the market was unaware of the degree to which Project Matador relied on a single tenant’s funding commitment.

Once that concentration risk materialized, the repricing was swift. The loss was not incremental. It was structural. The market did not merely reassess a delayed milestone—it reassessed the foundation of the company’s financing strategy.

For investors who purchased shares in or traceable to the IPO, the harm was compounded. Shares purchased at or near the $21.00 offering price lost more than half their value within weeks.

Litigation and Procedural Posture

The action is pending in the Southern District of New York. The named plaintiff, Salvatore Lupia, seeks to represent investors who purchased Fermi securities pursuant to or traceable to the IPO registration statement and those who purchased during the October 1 to December 11, 2025 class period.

The complaint asserts claims under Sections 11 and 15 of the Securities Act of 1933 and Sections 10(b) and 20(a) of the Securities Exchange Act of 1934. Defendants include the company, senior executives—including CEO Toby Neugebauer and CFO Miles Everson—directors, and multiple IPO underwriters.

Plaintiffs allege both strict liability for false IPO disclosures and scienter-based fraud for post-IPO statements that allegedly reinforced a misleading narrative about tenant demand and liquidity.

Shareholder Sentiment

In the wake of the December 2025 collapse, shareholder sentiment turned sharply from speculative excitement to open hostility. On social platforms like Reddit, retail investors and local community members coalesced around a narrative of overpromising and under-delivering. Threads such as “Texans Are Fighting a 6,000 Acre Nuclear-Powered Datacenter” became hubs for venting frustration, not just over the stock’s “tailspin” but over the project’s environmental impact. Users criticized the company’s leadership for “parachuting in” and risking local water resources, with some commentators noting that the rumored “unnamed client” (often speculated to be Amazon) dropping out was a foreseeable disaster that insiders should have flagged sooner. The formation of opposition groups like the “806 Data Center Resistance” further fueled a sense that the company was fighting battles on multiple fronts—financial, legal, and reputational—while investors were left holding the bag.

Analyst Commentary

The reversal in professional sentiment was equally stark. Just a month prior to the collapse, analysts had been defending the company’s delays. In November 2025, Nicholas Amicucci of Evercore ISI—a lead underwriter for the IPO—told Morningstar that the $150 million advance was “seemingly underappreciated by the market” and signaled a deepening commitment from the tenant. That framing crumbled on December 12.

Following the termination of that very agreement, financial outlets like CarbonCredits.com and MT Newswires shifted their focus from the company’s “ambitious” $90 billion potential to the immediate reality of a 40%+ pre-market crash. The narrative rapidly pivoted from a story about a “Manhattan Project for AI” to a cautionary tale about a pre-revenue REIT reliant on a single, non-binding counterparty.

SEC Filings & Risk Factors

Fermi’s SEC filings contained extensive risk disclosures warning that the company had not yet constructed its facilities, had entered into only a single non-binding letter of intent, and might not achieve tenant adoption at the pace required for financial viability.

The lawsuit does not claim those warnings were absent. Instead, it argues they were incomplete. Plaintiffs contend that risk factors framed tenant funding as a possibility, while omitting the extent to which Project Matador’s near-term financing depended on a single tenant whose commitment could evaporate before construction began.

Under securities law, cautionary language cannot shield disclosures that fail to reveal known trends or uncertainties. Whether Fermi crossed that line is now a question for the court.

Conclusion: Implications for Investors

The Fermi case is not just about a failed agreement. It is about concentration risk dressed as momentum.

For investors, the lesson is familiar but unforgiving: early-stage infrastructure stories often hinge on counterparties, not concepts. When financing depends on one tenant, one agreement, one assumption, the margin for error narrows to almost nothing.

For companies riding the AI infrastructure wave, the case underscores the importance of precision in IPO disclosures—especially when ambition outruns execution. The market can forgive delays. It rarely forgives surprise dependence.

Now, investors are fighting back.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![LifeMD, Inc. (LFMD) Securities Class Action Lawsuit Update [December 3, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/lfmd-alert-plus-banner.webp)

![Agilon Health, Inc. (AGL) Securities Class Action Lawsuit Update [January 7, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/agl-alert-plus-banner.webp)

![Klarna Group Plc (KLAR) Securities Class Action Lawsuit Update [January 1, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/klar-alert-plus-banner.webp)