![LifeMD, Inc. (LFMD) Securities Class Action Lawsuit Update [December 3, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/lfmd-alert-plus-banner.webp)

The Anatomy of a Crisis: LifeMD Securities Class Action Reveals the Fragility of the Telehealth 'Moat'

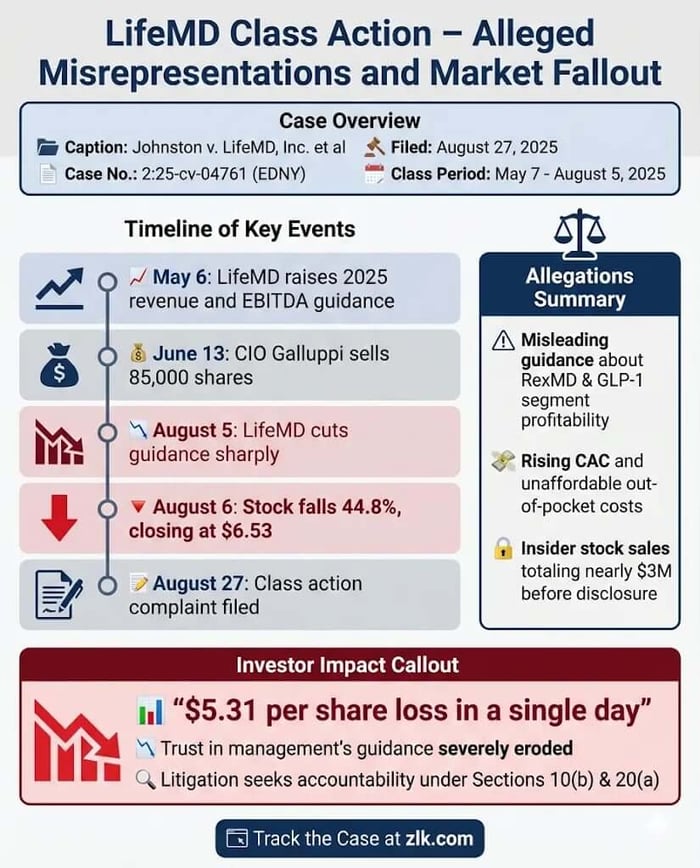

Caption: Johnston v. LifeMD, Inc. et al.

Case No.: 2:25-cv-04761

Jurisdiction: U.S. District Court, Eastern District of New York

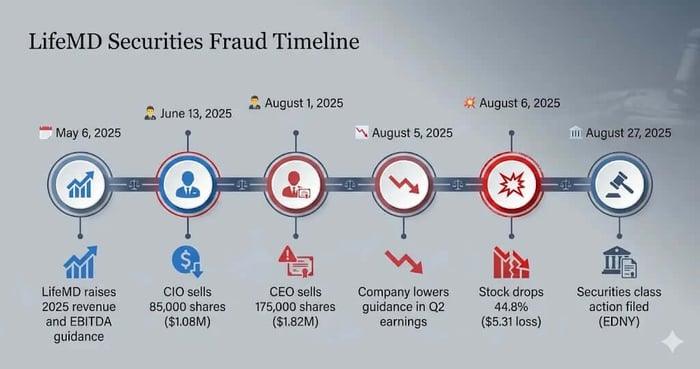

Filed on: August 27, 2025

Class Period: May 7, 2025–August 5, 2025

Introduction

A pivotal securities class action has been leveled against LifeMD, Inc. (LFMD), the virtual healthcare provider, alleging that the Company misrepresented the fundamental legitimacy of its operations and the sustainability of its growth model to investors. This securities class action lawsuit, Tyler Johnston v. LifeMD, Inc., Justin Schreiber, and Marc Benathen, filed in the United States District Court for the Eastern District of New York, casts a long shadow over the virtual primary care provider’s aggressive expansion. The core allegation is that CEO Justin Schreiber and CFO Marc Benathen knowingly or recklessly presented materially false and misleading full-year 2025 guidance to investors during the Class Period of May 7, 2025, through August 5, 2025. The Complaint alleges the Company failed to account for rising customer acquisition costs in its key RexMD men’s health segment, as well as the actual costs associated with the promising new weight management offerings like Wegovy and Zepbound. The reckoning for investors arrived on August 5, 2025, when a dramatic lowering of the full-year guidance triggered a massive sell-off. The ensuing 44.8% stock drop wiped out significant shareholder value, suggesting the firm’s claimed competitive moat was far thinner than management had assured the market. This analysis explores the anatomy of the alleged LifeMD securities fraud and its lasting implications for the high-growth telehealth investment sector.

Backdrop and Business Context

LifeMD operates as a leading provider of virtual primary care. The Company delivers telemedicine, pharmacy services, and specialized treatments across a wide spectrum of over 200 conditions, including primary care, men's and women's health, hormone therapy, and weight management. The business model hinges on two key pillars: the growth of its established men’s health brand, RexMD, and a strategic pivot into the highly competitive market for GLP-1 weight loss medications, such as Wegovy and Zepbound.

LifeMD sought to differentiate itself by establishing strategic collaborations with LillyDirect and NovoCare, claiming to be the only virtual care provider offering synchronous consults integrated with both platforms for cash-pay access to these branded therapies. This positioned the firm as a technology-enabled gateway to some of the most sought-after therapies in healthcare, leading management to claim they had created a "category-defining competitive moat in virtual obesity care." The operational setup leading to the alleged misconduct was characterized by this aggressive, two-pronged push for revenue growth—one that allegedly prioritized aspirational top-line figures over the underlying reality of rapidly increasing marketing expenses necessary to sustain that patient volume.

Promises Made vs. Reality

The narrative constructed for investors during the Class Period was one of exceptional strength and operational superiority. On May 6, 2025, after reporting its first quarter results, CEO Justin Schreiber declared an outstanding first quarter that achieved a first-ever quarter of GAAP profitability well ahead of expectations. CFO Marc Benathen underscored this performance, noting the "exceptionally strong first quarter" and confirming the Company was "raising our full-year 2025 guidance to reflect our strong performance." The total revenue guidance was raised to a new range of $268 million to $275 million, with Telehealth adjusted EBITDA forecast to exceed $21 million.

Schreiber was unequivocal about the competitive advantage, stating on a May 6 Earnings Call that LifeMD’s partnerships and infrastructure created a "category-defining competitive moat in virtual obesity care." When questioned by an analyst about the seemingly conservative new guidance, Benathen dismissed any concerns, claiming, "I mean, we tend to take a relatively conservative view to revenue."

The Complaint alleges the reality was starkly different. This heightened 2025 guidance was allegedly not "conservative" but recklessly issued and "impossible to achieve." The competitive moat was, in fact, porous. The Company was allegedly struggling with two critical, undisclosed operational risks:

RexMD's Cost Overruns: The men's health segment was experiencing "temporarily elevated customer acquisition costs in the highly competitive ED market."

Weight Management Affordability: The GLP-1 business was impacted by a "higher-than-anticipated refund rate" driven by patients unable to afford the out-of-pocket costs for branded therapies or lacking insurance coverage.

The lawsuit frames the contrast as a failure of candor, arguing management recklessly disregarded negative facts at the time they were issuing overconfident financial projections.

Timeline of Alleged Misconduct and Disclosures

The alleged wrongful conduct took place primarily within the Class Period, which spanned from May 7, 2025, to August 5, 2025, inclusive.

May 7, 2025: The Class Period began. This followed the release of the Company's First Quarter 2025 Results (the "Q1 Release") and the associated Earnings Call on May 6, 2025. During these announcements, the Company raised its full-year 2025 guidance for both revenue and adjusted EBITDA. Specifically, they raised expected total revenues to a range of $268 million to $275 million, and adjusted EBITDA to a range of $31 million to $33 million, citing "outperformance of our Telehealth business to-date." The complaint alleges these statements were materially false and misleading, as the heightened guidance was recklessly issued and was unlikely to be achieved.

June 13, 2025: LifeMD's Chief Innovation Officer, Stefan Galluppi, sold 85,000 shares of stock, raising $1,079,500. The Plaintiff's purchases of stock also occurred during this time, including a transaction on July 14, 2025.

August 1, 2025: CEO and Chairman Justin Schreiber sold 175,000 shares of LifeMD stock, raising $1,821,750 in the process.

August 5, 2025: The Class Period concluded. After the market closed that day, LifeMD issued its Second Quarter 2025 Results and held the Q2 2025 Earnings Call. During this announcement, the truth of the undisclosed issues began to emerge. The Company lowered its full-year 2025 guidance due to "temporary challenges facing our Rex MD business," and a "higher-than-anticipated refund rate" in the weight management business.

The revised guidance was drastically lower, with total revenue expectations being reduced to a range of $250 million to $255 million and Adjusted EBITDA reduced to a range of $27 million to $29 million. The next day, August 6, 2025, the price of LifeMD common stock fell $5.31 per share, or 44.8%, closing at $6.53. The Class Action Complaint was officially filed on August 27, 2025.

The securities class action outlines a clear causal chain from alleged misstatement to market correction, focusing on the brief, consequential Class Period.

Investor Harm and Market Reaction

The disclosure on August 5, 2025, served as the loss causation for LifeMD investors, directly linking the revelation of concealed operational issues to the precipitous decline in the Company’s valuation. The initial alleged inflation was driven by the May 6th statements that materially overstated the Company’s competitive position and profitability, convincing investors to purchase shares at inflated prices.

The market’s reaction on August 6th was a brutal quantification of this alleged misrepresentation: a 44.8% price drop. This single-day event tied the price collapse to the systemic issues of unmanageable Customer Acquisition Costs (CAC) in the RexMD segment and severe refund issues tied to patient affordability for GLP-1 weight loss drugs. The market, in its cold calculation, repudiated the management’s narrative of a "conservative" and structurally sound business. An analyst, reflecting the shock on the Q2 call, questioned whether the full-year guide down was "totally related to the dynamics faced with the RexMD business," highlighting deep skepticism about the Company’s sudden admission of problems it insisted were already resolved.

Litigation and Procedural Posture

The Johnston v. LifeMD action asserts claims under the Securities Exchange Act of 1934. The primary legal claims are:

Section 10(b) and Rule 10b-5: Asserted against LifeMD, Inc., and the Individual Defendants (Justin Schreiber and Marc Benathen) for employing devices, schemes, and artifices to defraud, and for making untrue statements or omitting material facts.

Section 20(a): Asserted against the Individual Defendants as "controlling persons" who were able to, and did, control the content of LifeMD’s public statements and are thus liable for the Company's primary violations.

The Complaint's core legal challenge lies in the scienter allegations—proving the Defendants acted knowingly or with reckless disregard for the truth. This is supported by two key pillars: the reckless issuance of "heightened 2025 guidance" that Defendants should have known was impossible to achieve , and the strategically timed insider sales by CEO Justin Schreiber and Chief Innovation Officer Stefan Galluppi just prior to the corrective disclosure. The sales, totaling nearly $3 million at allegedly "artificially inflated prices," suggest the executives were personally capitalizing on the concealed operational weaknesses.

Shareholder Sentiment

The 44.8% stock drop on August 6, 2025, acted as an emotional sledgehammer for shareholders, quickly transforming digital sentiment from cautious optimism to outright betrayal. Before the Q2 disclosure, discussions on platforms like X/Twitter and Reddit often centered on the GLP-1 optionality and the successful pivot into weight management.

The shift was immediate, intense, and focused on the alleged manipulation of expectations. The consensus quickly became one of feeling manipulated by the aggressive, now-retracted, guidance. The focus on X/Twitter was sharp, short, and accusatory. Conversations on Reddit focused on the systemic nature of the problems. The Stocktwits platform saw a surge of "Bearish" tags and comments demanding accountability.

The dominant trend was a profound and rapid erosion of trust, transitioning from faith in a high-growth telehealth story to an immediate push for legal recourse against the alleged LifeMD securities fraud.

Analyst Commentary

The nature of the August 5th disclosure—a sudden, deep cut to previously raised guidance—prompted a wave of decisive analyst action. The prior narrative of success, driven by the Company’s strategic partnerships and the "blue sky" opportunity of the GLP-1 market, was instantly discredited. Multiple firms issued rapid "Hold" or "Sell" ratings, revising their outlook from "Outperform" or "Buy." The reports centerED on the failure of the margin story.

Target prices saw dramatic cuts, commensurate with the 44.8% stock drop. A prior target of $18 was ultimately lowered to $10 by BTIG's David Larsen, reflecting the realization of structural cost issues.

SEC Filings & Risk Factors

The LifeMD lawsuit alleges that the Company's public statements were materially misleading because they omitted or downplayed crucial negative operational trends, particularly in their Q1 2025 filings. In standard SEC filings, the Risk Factors section is intended to warn investors about potential threats to the business. The allegations suggest LifeMD failed to adequately articulate the imminence and severity of the now-realized risks:

Customer Acquisition Cost Escalation Risk: The complaint alleges RexMD's internal CAC was already unsustainably high by May 2025. A sufficiently candid risk factor would have warned that "intense competition in the men’s health telehealth market is driving up customer acquisition costs (CAC) to a degree that may materially impair our profitability and ability to meet Adjusted EBITDA targets, requiring a sudden revision of financial guidance."

Patient Affordability and Refund Rate Risk: The corrective disclosure revealed a "higher-than-anticipated refund rate driven by patients either lacking insurance coverage [...] or being unable to afford the out-of-pocket cost" for GLP-1 therapies. The relevant 8-K filing for the Q2 results served as the admission of this omitted risk. Prior filings should have provided a candid assessment of the financial vulnerability tied to the patient’s ability to sustain the cash-pay price for these medications, especially if internal refund data already indicated a looming problem. The failure to include these specific, material operational risks in the forward-looking statements or risk sections of the 10-Q is what fundamentally underpins the securities class action allegations.

Conclusion: Implications for Investors

The LifeMD securities class action serves as a stark object lesson for investors navigating the rapid, disruptive landscape of digital health and telehealth stocks. The central theme of this case is the danger of growth narratives detached from sustainable unit economics. Management's repeated assurances of a "competitive moat" and "conservative" guidance were, according to the lawsuit, a thin veneer over structural business challenges.

The key red flags for investors in similar high-growth, high-marketing-spend companies—especially those scaling through direct-to-consumer digital channels—are clear:

The CAC-to-LTV Disconnect: A sudden, devastating rise in Customer Acquisition Costs is a severe warning signal. When a company with an established segment (RexMD) suddenly cites "elevated CAC" as the primary reason for a guidance cut, it suggests fundamental problems with the Lifetime Value (LTV) of that customer base that were not being disclosed or controlled.

Affordability Risk in GLP-1s: For all companies participating in the weight management or GLP-1 sector, the LifeMD case highlights that patient affordability—specifically the ability to pay high cash prices or secure insurance coverage—is an immediate, material risk, not just a long-term headwind. Relying on cash-pay access without adequately mitigating churn or refund risk is inherently fragile.

This case is a reckoning for the entire telehealth investment sector, reinforcing that operational excellence and disciplined cost control must always take precedence over market performance and aspirational top-line figures. Now, investors are fighting back to hold the control persons accountable for the alleged inflation of their share price.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Fermi Inc. (FRMI) Securities Class Action Lawsuit Update [January 8, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/frmi-alert-plus-banner.webp)

![Agilon Health, Inc. (AGL) Securities Class Action Lawsuit Update [January 7, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/agl-alert-plus-banner.webp)

![Klarna Group Plc (KLAR) Securities Class Action Lawsuit Update [January 1, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/klar-alert-plus-banner.webp)