![Primo Brands Corporation (PRMB) Securities Class Action Update [November 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/prmb-alert-plus-banner-image.webp)

Primo Brands Faces Federal Securities Class Action Over Allegedly “Flawless” Merger Integration

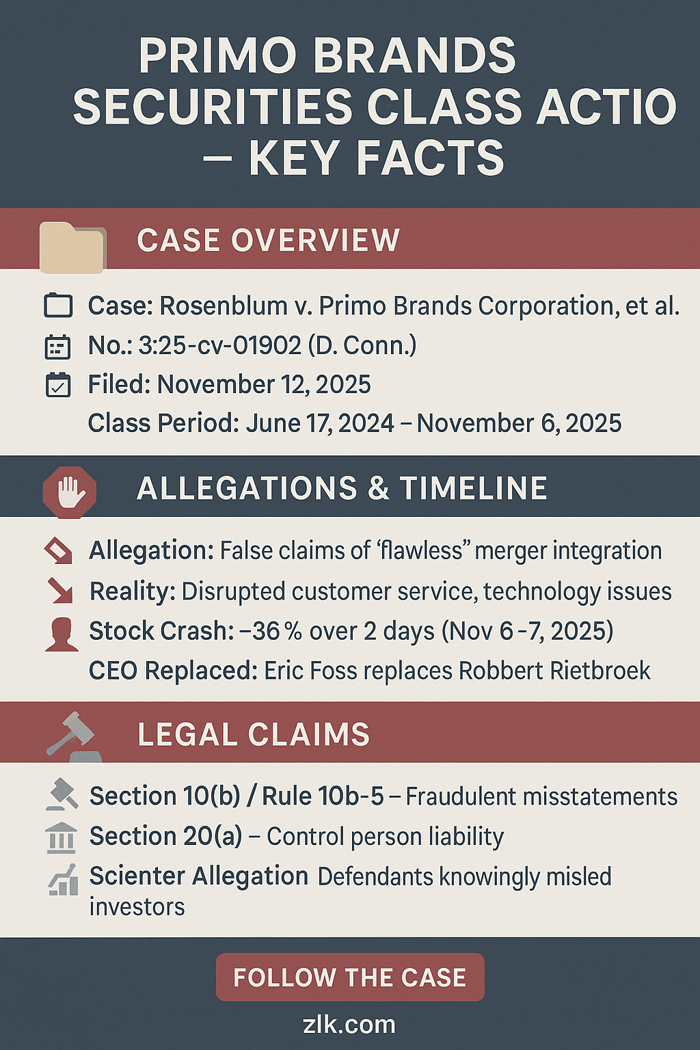

Case Name: Rosenblum v. Primo Brands Corporation, et al.

Case No.: 3:25-cv-01902

Jurisdiction: U.S. District Court, District of Connecticut

File on: November 12, 2025

Class Period: June 17, 2024–November 6, 2025

Introduction

Primo Brands Corporation, a newly formed beverage giant, is now the target of a federal securities class action lawsuit. The action, filed in the U.S. District Court for the District of Connecticut, alleges that the Company and executives David Hass, C. Dean Metropoulos, and Robbert Rietbroek (“Individual Defendants”) made materially false and/or misleading statements regarding the merger of Primo Water Corporation and an affiliate of BlueTriton Brands.

The lawsuit centers on the purchase of (1) common stock of Primo Water Corporation from June 17, 2024, through November 6, 2025, inclusive, and/or (2) common stock of Primo Brands between November 11, 2024 through November 8, 2024, inclusive (collectively, the “Class Period”). According to the complaint, management repeatedly assured investors of "transformative operational efficiencies," achieving "meaningful synergies," and a "flawless integration execution”, while the reality was a “disastrous merger integration process” and customer service issues that actively crippled the Company’s ability to supply customers. This alleged deception was unmasked across two corrective disclosures. As alleged, the full truth culminated on the November 6, 2025, with the announcement that the CEO was replaced and full-year 2025 guidance slashed in a separate press release announcing Q3 2025 financial results the same day. The market’s reaction was immediate and punishing: the stock plummeted more than 36% over two trading days, wiping out over $2.0 billion in shareholder value.

Backdrop and Business Context

Primo Brands Corporation (PRMB) operates as a leading North American beverage company, focusing on healthy hydration products distributed across multiple channels and price points. The Company's common stock trades on the New York Stock Exchange (NYSE).

The alleged misconduct is inseparable from the Company’s origin: its formation via an all-stock merger between Primo Water Corporation and an affiliate of BlueTriton Brands, Inc. Announced in June of 2024, and completed on November 8, 2024, this "transformative transaction" was touted as a merger positioned for "sustained long-term growth," boasting an iconic brand portfolio that includes Poland Spring and Pure Life®. The operational setup was vertically integrated, spanning a "coast-to-coast manufacturing and distribution network." The central promise—enhanced distribution capabilities and meaningful cost synergies—became the nexus of the future class action.

Promises Made vs. Reality

Throughout the Class Period, Primo Brands leadership, including CEO Robbert Rietbroek and CFO David Hass, repeatedly framed the merger integration as a seamless success, a narrative that stood in stark opposition to the internal challenges later revealed.

The Promises: In the June 17, 2024 merger announcement, CFO Hass pointed to an opportunity to "better align our activities to deliver superior service at a lower cost." Following the merger's close, then-CEO Rietbroek highlighted the goal to "capture transformative operational efficiencies, achieve our synergy goals and deliver strong financial results." Most critically, during the fourth quarter 2024 earnings call on February 20, 2025, Rietbroek stated that "all aspects of our business are aligning for flawless integration execution." He repeated this sentiment in May 2025.

The Alleged Reality: The complaint alleges these statements were materially false and misleading because, in truth, the merger integration was tracking poorly, being "far more complicated and more complex" than investors were led to believe. This complexity led to significant and immediate problems, including technology and customer service issues, major supply disruptions, and an internal state of crisis. The rush to achieve synergies—closing facilities and reducing headcount—is alleged to have led directly to "disruptions in product supply, delivery, and service." The eventual admission came from the newly appointed CEO, Eric Foss, on November 6, 2025, who conceded that the Company "probably moved too far too fast on some of the various integration work streams" and that the speed impacted their ability to manage warehouse closures and route realignment without serious disruption.

Timeline of Alleged Misconduct and Disclosures

The narrative of the alleged fraud unfolds through a series of increasingly optimistic statements followed by two painful corrective disclosures.

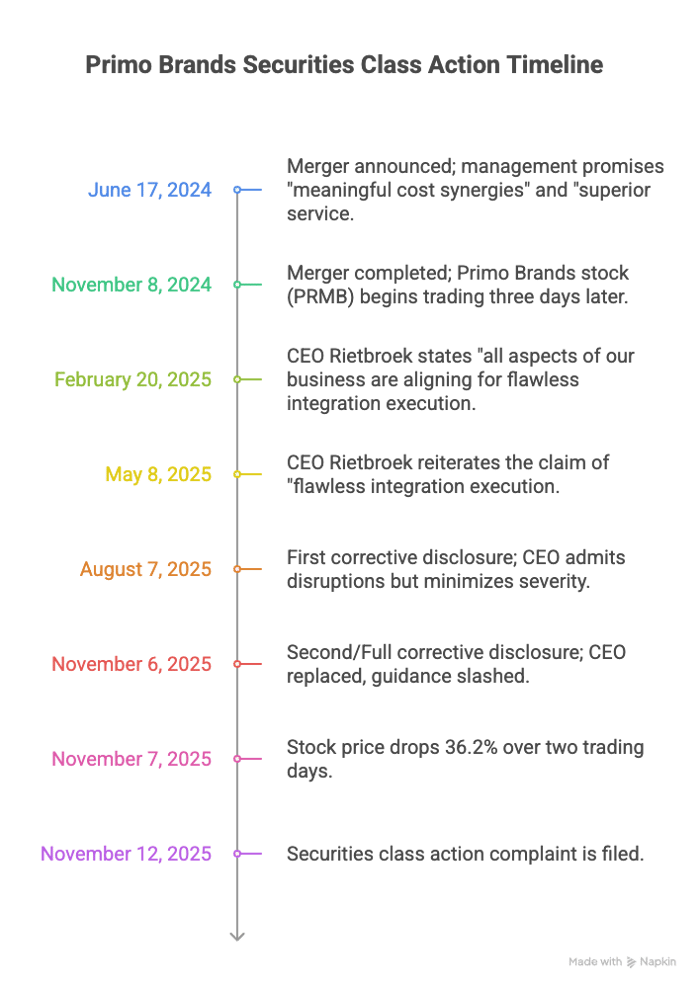

June 17, 2024: Merger announced; management promises "meaningful cost synergies" and "superior service." This begins the Class Period (for Primo Water stock).

November 8, 2024: Merger completed; Primo Brands stock (PRMB) begins trading three days later. This is the start of the Class Period (for PRMB stock).

February 20, 2025: CEO Rietbroek states "all aspects of our business are aligning for flawless integration execution," allegedly establishing the high-water mark for misstatements.

May 8, 2025: CEO Rietbroek reiterates the claim of "flawless integration execution."

August 7, 2025 (First Corrective Disclosure): Company announces Q2 2025 results. CEO Rietbroek admits headcount and facility reductions led to "disruptions in product supply, delivery, and service" but minimizes the severity. The stock drops $2.41, or 9.1%, to close at $24.00, signaling investor concern.

November 6, 2025 (Second/Full Corrective Disclosure): CEO Rietbroek is replaced; new CEO Eric Foss admits the Company "moved too far too fast," revealing extensive "customer services issues" and severe "integration issues related to the technology move over." Full-year 2025 net sales and adjusted EBITDA guidance are severely slashed as reported in the earnings release.

November 7, 2025: Following the news, the stock closes down, resulting in a total drop of $8.20 per share, or 36.2%, over two trading days.

November 12, 2025: Securities class action complaint is filed.

Investor Harm and Market Reaction

The lawsuit directly connects the precipitous decline in Primo Brands’ common stock price to the market's absorption of the corrective disclosures, asserting that the price had been artificially inflated throughout the Class Period by the Defendants' misrepresentations.

The most severe impact occurred on November 6 and 7, 2025, following the full disclosure of the disastrous merger integration, technology issues, and customer service failures. The stock price fell from a closing price of $22.66 on November 5, 2025, to close at $14.46 per share on November 7, 2025, representing a decline of $8.20 per share, or more than 36%. This single event is alleged to have wiped out $2.0 billion in market capitalization. Investors were left with a company facing operational headwinds far more severe than management had publicly admitted.

Litigation and Procedural Posture

The complaint, filed in the District of Connecticut, names Primo Brands Corporation and Individual Defendants: David Hass, C. Dean Metropoulos, and Robbert Rietbroek.

The asserted legal claims are:

Violation of Section 10(b) and Rule 10b-5 of the Securities Exchange Act of 1934, the central fraud claim alleging all Defendants knowingly or recklessly made false or misleading statements or omissions of material fact.

Violation of Section 20(a), the "controlling person" claim asserted against the Individual Defendants who allegedly had the power and authority to influence and control the dissemination of the allegedly false statements.

The complaint makes strong allegations of scienter, asserting that the Individual Defendants knew, or recklessly disregarded, the materially false or misleading nature of their public statements. Given their high-level positions, they were allegedly aware that the positive representations were materially false because the integration was actively failing. This failure to disclose known adverse facts forms the basis for the scienter claim.

Shareholder Sentiment

Shareholder sentiment in the wake of the Primo Brands merger mirrored the arc of the Company's public statements: initial enthusiasm for a "transformative" deal quickly soured into confusion, then outrage, upon the full disclosure.

Before the August and November 2025 disclosures, the prevailing sentiment on platforms like X/Twitter and Reddit was anchored in the promised synergies. The belief was that the combined entity was creating a defensive and profitable powerhouse. Statements align reflected a hopeful, almost complacent, tone about an unstoppable growth story.

The November 6, 2025 news triggered a massive emotional and financial reckoning. When the CEO was replaced and guidance was severely cut, the sentiment transformed into one of betrayal. The prevailing narrative became: management had lied about the core of the merger's success—the integration—for months. The dramatic stock collapse felt like a punishment for what the market perceived as deliberate concealment of operational failure.

Analyst Commentary

Professional analyst commentary quickly turned from cautious optimism to outright alarm following the corrective disclosures, explicitly citing a profound crisis of credibility for the Company’s leadership.

Following the November 6, 2025, disclosure, the reaction was exceptionally sharp. JPMorgan analysts reported that the 3Q 2025 earnings print and subsequent guidance cut were "another in a series of disappointments since the merger." They explicitly tied the severe stock price reaction not just to the poor financials but to the "overall lack of investor confidence in the company."

Barclays analysts echoed this sentiment, stating that the outsized stock reaction "tells us this seemingly has more to do with credibility than anything else." They delivered a grim prognosis: "trends will get worse before they get better." The sudden and drastic reversal—moving from an expected growth of +3-5% to a "low single digit decline"—forced sweeping downgrades and significant target price cuts as reflected by the revised average target prices. The core takeaway from the analyst community was a loss of faith in the Company's ability to forecast and execute its core integration strategy.

SEC Filings & Risk Factors

The lawsuit suggests that while management failed to disclose the true extent of the integration issues in their public pronouncements, an examination of general risk factors may reveal a tension between the disclosed boilerplate warnings and the specific, undisclosed operational crisis.

Primo Brands, as a public U.S. company, files periodic reports with the SEC. These filings detail Risk Factors—potential events that could materially and adversely affect the Company’s business. The core allegation here is not that the Company failed to warn of general merger risks, which is standard. Instead, the lawsuit contends there was a distinct lack of candor: the specific, crippling risks cited in the complaint (e.g., technology transition failures, customer service breakdowns, and supply chain disruptions) were not mere possibilities but were allegedly known adverse facts that had already materialized and were being actively concealed during the Class Period.

The Plaintiff contends that the statements complained of were not forward-looking speculation but purported statements of current facts and conditions—such as the "flawless" nature of the ongoing integration.

Conclusion: Implications for Investors

The Primo Brands class action serves as a crucial, expensive lesson in the risks of synergy. It highlights the possibility of management teams to over-promise the smoothness and speed of complex merger integrations—especially when the resulting entity is positioned for major growth.

For investors, any time a management team repeatedly uses superlative, definitive terms like "flawless" to describe a dynamic process, caution is warranted. Furthermore, the Company's eventual admission—that they "moved too far too fast"—is a classic symptom of prioritizing short-term synergy capture over long-term operational integrity. The ultimate outcome of this litigation will rest on the Plaintiff's ability to prove the requisite scienter—that the executives knew the integration was failing while publicly painting a rosy picture. For all market participants, the Primo Brands case is a potent reminder: operational reality always catches up to promotional rhetoric.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal nor financial advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Stride, Inc. (LRN) Securities Class Action Update [November 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/lrn-alert-plus-banner.webp)

![Jayud Global Logistics Limited (JYD) Securities Class Action Lawsuit Update [December 2, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/jyd-new-case-banner.png)

![Skye Bioscience, Inc. (SKYE) Securities Class Action Lawsuit Update [December 10, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/skye-alert-plus-banner.webp)