![Sprouts Farmers Market, Inc. (SFM) Securities Class Action Lawsuit Update [December 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/sfm-alert-plus-banner.webp)

Investors Allege Resilience Was an Illusion

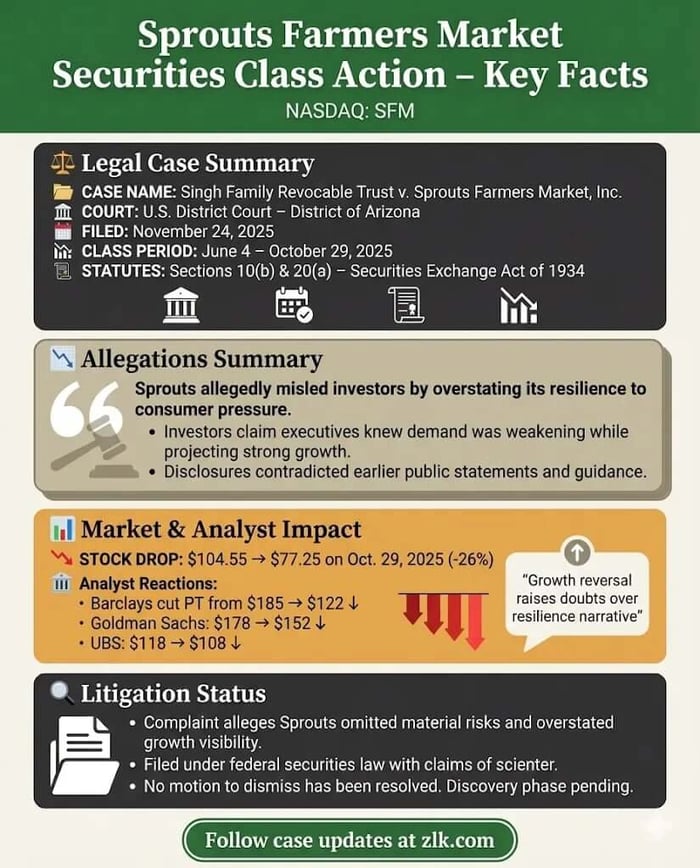

Case Name: Singh Family Revocable Trust U/A DTD 02/18/2019 v. Sprouts Farmers Market, Inc., et al.

Case No.: 2:25-cv-04416-JJT

Jurisdiction: U.S. District Court, District of Arizona

Filed on: November 24, 2025

Class Period: June 4, 2025-October 29, 2025

Introduction

Sprouts Farmers Market, Inc. did not warn investors about a weakening consumer. It dismissed the possibility outright—until it couldn’t.

In November 2025, a federal securities class action was filed against Sprouts Farmers Market, Inc. (NASDAQ: SFM), alleging that the company and its top executives misled investors about the durability of demand, the resilience of its customer base, and its ability to sustain elevated growth through a shifting macroeconomic environment. The lawsuit centers on a sharp reversal: repeated assurances that Sprouts was insulated from consumer pressure, followed by an abrupt disclosure that growth had faltered and guidance would be cut.

The market response was swift. One day. A 26 percent drop. Investors allege the damage was avoidable—and that the warning signs were already known inside the company.

Backdrop and Business Context

Sprouts Farmers Market operates a specialty grocery chain focused on natural, organic, and health-oriented products. With more than 450 stores across 24 states during the relevant period, the company positioned itself as a differentiated retailer—less exposed to price sensitivity, more anchored to lifestyle commitment.

That positioning mattered. Management consistently framed Sprouts’ customer as resilient, health-focused, and willing to maintain spending even as macroeconomic pressure mounted elsewhere. In earnings calls and investor conferences, executives emphasized that Sprouts would not merely weather a cautious consumer—it would benefit from it.

By mid-2025, the company was reporting double-digit comparable store sales growth and raising full-year guidance. Internally, according to investors, the story was already more fragile.

Promises Made vs. Reality

On June 4, 2025, Sprouts’ CEO told analysts that the company was seeing “no change whatsoever” in customer behavior despite rising concerns about consumer confidence. The message was unambiguous: Sprouts was different. Its customers were insulated. Its model was resilient.

Weeks later, that confidence hardened into numbers. On July 30, 2025, Sprouts raised its full-year outlook, projecting comparable store sales growth of up to 9 percent and reaffirming confidence in its ability to lap prior year comparisons. Executives attributed performance to strong produce seasons, limited competitive exposure, and what they described as consistent two-year stack performance.

Investors allege these statements omitted material facts. According to the complaint, consumer spending had already begun to soften, particularly in middle-income and younger trade areas. The tailwinds management described were temporary. The comparisons ahead were steeper than disclosed. And the forecasting processes were not as reliable as portrayed.

When the truth surfaced, it did so all at once.

Timeline of Alleged Misconduct and Disclosures

The alleged misconduct unfolded in a tight arc. In early June 2025, Sprouts publicly rejected the idea that macroeconomic pressure was affecting its customer base. By late July, the company raised guidance and reinforced that narrative with detailed projections.

On October 29, 2025, the tone changed. Sprouts reported third-quarter results that missed expectations, with comparable store sales growth falling below both analyst forecasts and the company’s own guidance. Fourth-quarter projections were slashed. Full-year expectations were revised downward—despite having been raised only one quarter earlier.

Management attributed the reversal to “challenging year-on-year comparisons” and “a softening consumer.” Investors allege that was precisely the risk they had been told did not exist.

Investor Harm and Market Reaction

The market reacted immediately. Sprouts’ stock fell from $104.55 to $77.25 in a single trading day, wiping out more than a quarter of the company’s market value.

Analysts followed quickly. Barclays cut its price target by roughly one-third, warning that growth was slowing faster than expected amid consumer uncertainty and competitive pressure. Other firms echoed the concern, highlighting the speed of the deceleration and questioning whether Sprouts’ differentiation was as durable as previously believed.

Investors allege that these losses were directly tied to the corrective disclosures—that the stock price had been artificially inflated by prior misstatements, and that the decline represented the market finally absorbing the truth.

Litigation and Procedural Posture

The lawsuit was filed in the United States District Court for the District of Arizona under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934. The named defendants include Sprouts Farmers Market, Inc., CEO Jack L. Sinclair, and CFO Curtis Valentine.

Plaintiffs allege that defendants acted with scienter—either knowingly or recklessly—by presenting growth projections and resilience claims without disclosing known risks and internal weaknesses. The complaint emphasizes the contrast between earlier categorical assurances and later admissions that consumer pressure had been building.

The case is at an early stage. No motion to dismiss has yet been resolved. Discovery, if it proceeds, will test what management knew, when they knew it, and how forecasting decisions were made.

Shareholder Sentiment

Prior to the October 29, 2025, earnings release, investor commentary on platforms like X (formerly Twitter) largely reflected optimism about Sprouts Farmers Market's ($SFM) differentiation, consistent growth trajectory, and attractive valuation. For example, one investor highlighted the company's strong fundamentals, including 15% top-line growth projections for 2025 and a forward price-to-free-cash-flow ratio of 15x, describing it as "THE CLEANEST SETUP in the market" with a robust buyback program. Another expressed enthusiasm for its fast-growing specialty grocery model focused on health-oriented products, positioning it as a standout amid competitors. Some even added to positions ahead of earnings, citing potential for continued expansion despite recent pullbacks. On Reddit, discussions in September 2025 questioned if the stock was undervalued at a P/E of 24.3x, noting its outperformance relative to peers and persistent earnings beats despite a gradual price decline.

Following the October 29, 2025, disclosure—which revealed a comparable store sales miss (5.9% vs. guided 6-8%) and sharply lowered guidance (Q4 comps 0-2%, full-year sales ~14%) attributed to a softening consumer and tough comparisons—sentiment shifted abruptly to skepticism, frustration, and disappointment. On X, reactions included dismay at the ~25% single-day drop, with comments describing the stock as "getting whacked," "skewered," or in a "complete reset," and questioning whether it was "priced for perfection" beforehand. Many pointed to the sudden deceleration as evidence of broader consumer weakness impacting grocery stocks, with some viewing it as a short opportunity or expressing shock ("this cannot be fucking real") despite an EPS beat. Analysts and summaries echoed concerns over the guidance cut eroding prior resilience claims, with the market reaction seen as punishing the reversal from July's raised outlook.

By November-December 2025, commentary remained mixed but cautious, with ongoing references to the post-earnings selloff, lawsuit alerts, and a ~50% decline from June highs. Some investors saw value in the beaten-down price, noting strong long-term fundamentals like high margins (~7.7%, nearly double peers), store expansion, and buybacks, while others highlighted risks from consumer softening. Overall, the prevailing post-disclosure theme was frustration over the abrupt slowdown and lack of earlier signaling, damaging trust in management's prior assurances of insulation from macroeconomic pressures.

Analyst Commentary

Following the October 29, 2025, Q3 earnings release—which revealed comparable store sales growth of 5.9% (below the guided 6-8%) and a slashed Q4/full-year outlook amid tougher comparisons and consumer softening—analysts quickly recalibrated their views on Sprouts Farmers Market ($SFM). Firms that had endorsed the company's growth and resilience narrative lowered price targets significantly, emphasizing near-term uncertainty, faster-than-expected deceleration, and questions about the durability of Sprouts' differentiation in a cautious consumer environment.

Barclays cut its price target from $185 to $122 (a ~34% reduction) while maintaining an Overweight rating, noting disappointing Q3 results due to slower comp sales but highlighting well-managed margins and a constructive long-term outlook.

Goldman Sachs lowered its target from $178 to $152 (maintaining Buy), expecting shares to trade lower due to softer Q4 guidance but pointing to resilient profitability and EPS growth as positives.

UBS reduced its target to $108 from a prior $118 (and earlier $180), maintaining Neutral, reflecting ongoing concerns over comp deceleration and macro pressures.

Broader commentary highlighted the magnitude of the slowdown as more than temporary, shifting focus to structural issues like pricing power, customer elasticity, competitive dynamics in natural/organic groceries, and whether Sprouts' niche provides the insulation previously claimed. Consensus post-earnings leaned toward caution, with average price targets dropping (e.g., to around $142-160 across firms) and discussions of consumer weakness impacting the sector.

SEC Filings & Risk Factors

Sprouts’ SEC filings during the class period included risk disclosures related to competition, consumer behavior, and macroeconomic conditions. Plaintiffs allege those disclosures were generic and failed to reflect the specific, known pressures already affecting the business.

According to the complaint, forward-looking statements were not accompanied by meaningful cautionary language and did not adequately disclose weaknesses in forecasting processes. Investors argue that risks were framed as hypothetical when, in reality, they were already materializing.

Conclusion: Implications for Investors

This case is not about a company missing a quarter. It is about narrative control—and what happens when that narrative collapses.

For investors, the Sprouts lawsuit underscores a familiar lesson in securities litigation: repeated assurances of resilience can become liabilities when conditions change faster than disclosures. Growth stories built on differentiation and confidence demand transparency when cracks appear.

Sprouts told investors it was insulated. The market now waits to see whether that insulation was overstated—and whether the law will require accountability for the difference.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![F5, Inc. (FFIV) Securities Class Action Lawsuit Update [December 22, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/ffiv-alert-plus-banner.webp)

![Alexandria Real Estate Equities, Inc. (ARE) Securities Class Action Lawsuit Update [December 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/are-alert-plus-banner.webp)

![Integer Holdings Corporation (ITGR) Securities Class Action Lawsuit Update [December 17, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/itgr-alert-plus-banner.webp)