![Jayud Global Logistics Limited (JYD) Securities Class Action Lawsuit Update [December 2, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/jyd-new-case-banner.png)

Alleged Pump-and-Dump Scheme Leaves Jayud Investors Facing Massive Losses

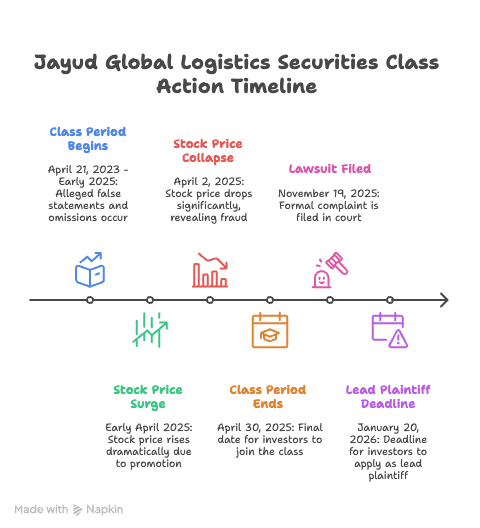

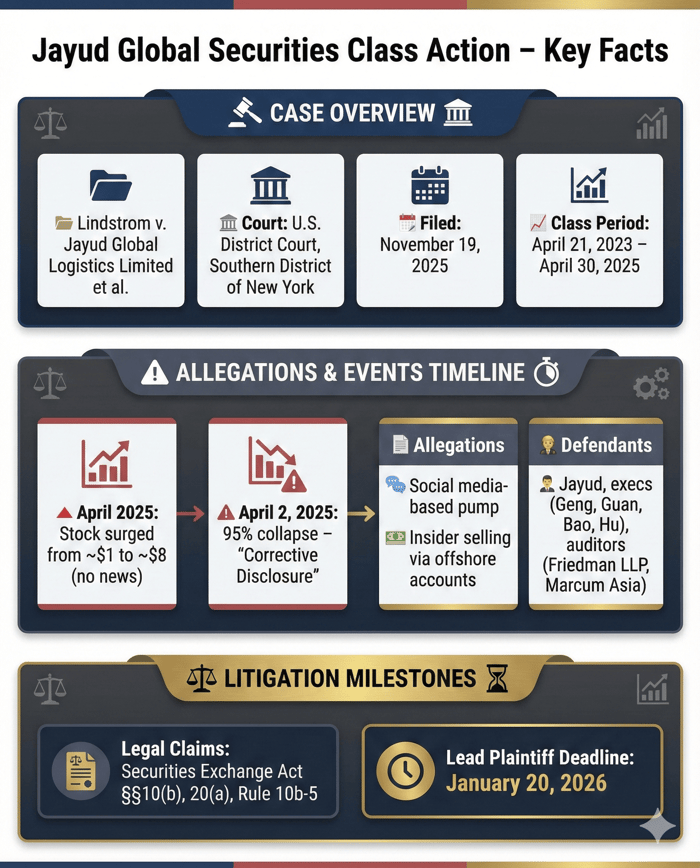

Caption: Lindstrom v. Jayud Global Logistics Limited et al.

Case No.: 1:25-cv-09662

Jurisdiction: United States District Court, Southern District of New York

Filed on: November 19, 2025

Class Period: April 21, 2023 - April 30, 2025, inclusive.

Introduction

A securities fraud class action has been filed against Jayud Global Logistics Limited (JYD), alleging that the Cayman Islands-based company became the centerpiece of a brazen pump-and-dump scheme that left investors with catastrophic losses. The lawsuit, filed on behalf of all investors who purchased Jayud securities between April 21, 2023, and April 30, 2025 (the Class Period), centers on the claim that the Company’s stock price was artificially inflated through social media misinformation and coordinated selling by insiders and affiliates. This narrative isn’t about a fundamental business failure; it's about a failure of corporate integrity, a market manipulation that climaxed with a near-total destruction of shareholder value. The legal battle ahead will determine whether investors can recover losses tied to what the complaint frames as a calculated act of deception.

Backdrop and Business Context

Jayud Global Logistics is a holding company incorporated in the Cayman Islands with primary operations based in Shenzhen, China. It positions itself as a provider of cross-border supply chain solutions, including freight forwarding, supply chain management, and other value-added services. The Company first entered the U.S. public markets around the beginning of the Class Period through a traditional Initial Public Offering (IPO), gaining access to U.S. capital and a broader investor base.

The operational setup of a newly listed, low-float China-based logistics firm carries inherent risks. They often command less institutional oversight and attention than their larger, domestically-listed peers. In this specific case, the Company's relatively small float—the number of shares available for public trading—appears to have made it acutely vulnerable to the kind of coordinated market manipulation that is now the core of the class action. The alleged misconduct took root in this context: a new market entrant with a thin capitalization structure, offering a ripe target for a fraudulent promotion.

Promises Made vs. Reality

Throughout the Class Period, Jayud management was making standard public statements about its business growth, operational success, and market position. While these statements may have appeared benign on their face, the lawsuit contends they were fundamentally misleading due to one central, devastating omission: the Company's failure to disclose the true, artificial nature of the trading in its shares.

The disconnect between the Company's claimed operational stability and the volatility of its stock was vast. While the Company spoke of logistics and cross-border solutions, the reality, as alleged in the complaint, was that its stock was being driven by a phantom momentum—a fraudulent promotion campaign involving social media-based misinformation and impersonated financial professionals. The public filings were silent on this orchestrated scheme. The Company, the complaint argues, was operating on two tracks: the purported business of moving goods and the alleged clandestine business of pumping its own stock, a deep betrayal of the fiduciary duty owed to every investor.

Timeline of Alleged Misconduct and Disclosures

The alleged scheme took place across the two-year Class Period, yet the decisive events occurred rapidly in early 2025.

- April 21, 2023 – Early 2025: The Company’s Class Period begins. Throughout this time, Defendants are alleged to have been making materially false or misleading statements by failing to disclose the existence of a stock promotion campaign and the use of offshore or nominee accounts by insiders/affiliates.

- Early April 2025: The stock price began a meteoric, unjustified rise, surging from approximately $1.00 per share to a peak near $8.00 per share. This surge, absent any corresponding fundamental news, is identified by the lawsuit as the climax of the fraudulent promotion.

- April 2, 2025: The price surge abruptly ended. The stock suffered a sudden, catastrophic collapse of approximately 95% from its recent high. This event serves as the "corrective disclosure"—the moment the market’s realization of the scheme became manifest, wiping out billions in market capitalization.

- April 30, 2025: The end of the Class Period, marking the final date for investors to have purchased the stock and still be considered members of the Class.

- November 19, 2025: The formal securities class action complaint is filed in the Southern District of New York.

Investor Harm and Market Reaction

The gravity of the market reaction is quantified by the 95% stock drop that occurred on or around April 2, 2025. This was not a modest correction following a missed earnings report; it was a total capitulation, a market rejection of the stock's recent valuation after the alleged fraud became too large to sustain.

Investors who purchased the stock near its peak of $8.00 saw their investments reduced to mere pennies in a single trading session. This abrupt, total destruction of value directly ties loss causation to the emergence of the "truth"—the fact that the previous price was driven by manipulation, not legitimate business performance.

Because of the stock’s micro-cap nature and the suddenness of the event, there was likely a vacuum of legitimate analyst coverage. The only "market reaction" that truly mattered was the liquidity vanishing. Those few professional analysts or financial commentators tracking the stock likely issued immediate, severe downgrades or "Strong Sell" advisories, shifting from caution to alarm as the stock entered freefall.

Litigation and Procedural Posture

The class action, Lindstrom v. Jayud Global Logistics Limited, et al., is proceeding in the United States District Court for the Southern District of New York under Civil Action No. 1:25-cv-09662.

- Asserted Legal Claims: The complaint asserts claims under Section 10(b) of the Securities Exchange Act of 1934 and Rule 10b-5, which address manipulative and deceptive practices in connection with the purchase or sale of securities. Claims under Section 20(a) are also likely asserted against the individual officers and directors for their control over the Company.

- Named Defendants: The litigation names Jayud Global Logistics Limited as the corporate defendant, along with key executives Xiaogang Geng, Alan Tan Khim Guan, Lin Bao, and Mengmeng Hu. Crucially, the complaint also names the accounting firms Friedman, LLP and Marcum Asia CPAs, LLP, suggesting the scope of the alleged misconduct may extend to the integrity of the Company’s financial reporting and the offering documents.

- Scienter Allegations: The scienter—the requisite state of mind for fraud—is heavily implied by the allegation that executives and affiliates were "uniquely situated" to orchestrate and benefit from the pump-and-dump scheme. The use of offshore and nominee accounts for coordinated selling suggests a deliberate, knowing intent to defraud investors by profiting from the artificial price inflation.

- Litigation Milestones: The first and most pressing milestone is the Lead Plaintiff Submission Deadline of January 20, 2026. This date will determine which investor, or group of investors, will be appointed by the Court to represent the Class and direct the litigation against the Defendants.

Shareholder Sentiment

The emotional arc of the Jayud shareholders was one of euphoric, almost desperate hope followed by sudden, absolute betrayal. Prior to the April 2025 crash, sentiment on platforms like Stocktwits and Reddit would have reflected the classic hallmarks of a pump: frantic speculation, celebration of daily gains, and a fierce, sometimes cult-like defense of the high valuation.

The 95% collapse fundamentally changed that dynamic. The chatter shifted instantly to anger, disbelief, and a profound sense of having been swindled. The focus immediately turned to the insiders and affiliates who were alleged to have been quietly selling shares into the manufactured euphoria. This shift—from the high of speculative success to the cold, hard reality of loss—is a potent driver for class action participation. The shareholder base is currently united by a sense of common victimhood.

Analyst Commentary

Legitimate analyst commentary on a micro-cap Chinese logistics firm would likely have been sparse, cautious, and focused primarily on fundamental metrics like logistics volume, margins, and geopolitical risk. However, the nature of the alleged pump-and-dump scheme suggests a different kind of "analyst commentary" was at play.

The lawsuit specifically cites "impersonated financial professionals" as a tool of the fraudulent promotion. This means the positive commentary that fueled the stock’s ascent may have been entirely fabricated—fake reports, fictitious price targets, or paid-for promotional content masquerading as objective research. True institutional analysts, observing the stock's massive surge without underlying fundamental news, would have likely issued private warnings or quietly avoided coverage altogether, knowing the price action was disconnected from reality. Any genuine analyst would have had to downgrade the stock to a "Sell" or "Avoid" status immediately following the April 2nd collapse, citing a total loss of confidence in the integrity of the market price.

SEC Filings & Risk Factors

A review of Jayud’s public filings (such as its 20-F annual report) reveals the critical risks the Company failed to disclose. Like all foreign issuers, Jayud would have included extensive boilerplate risk factors concerning its operations in China, foreign exchange fluctuations, and regulatory compliance.

However, the core omission, and the material falsehood at the heart of the lawsuit, lies in the failure to disclose the internal scheme. While a company may warn of general "market volatility" or "fraudulent third-party actors," the complaint argues that Jayud executives, affiliates, and advisors were actively facilitating the fraud. They failed to disclose that:

- The rapid appreciation of the stock was not due to business success, but to a controlled, fraudulent promotion.

- Insiders or affiliates were using private vehicles (offshore or nominee accounts) to sell shares into the inflated market, thereby breaching their fiduciary duty and profiting from the alleged misstatements.

The SEC filings, therefore, become documents of silence. By failing to disclose the "true nature of the trading activity in its securities," every official statement about the Company’s financial condition and market confidence was rendered misleading.

Conclusion: Implications for Investors

The Jayud Global Logistics Limited securities class action offers a stark lesson for investors in the contemporary market, particularly those involved with low-float, non-U.S. issuers. This case is a profound illustration of loss causation—the direct link between the allegedly fraudulent statements (or omissions) and the investor's eventual harm. When the true risk—in this case, an orchestrated pump-and-dump scheme—emerged, the stock lost virtually all its value.

The key takeaway is a simple yet profound one: if a stock price exhibits explosive growth without a corresponding, verifiable, fundamental business development, investors must approach the ascent with deep skepticism. In an age of pervasive social media, the line between legitimate market analysis and promotional fraud is constantly being blurred. The naming of the accounting firms in this suit further suggests that the legal net is expanding to capture gatekeepers who may have facilitated the listing process. For investors, this case serves as a powerful reminder that corporate trust must be earned with transparent, fully disclosed actions, not with artificial price surges driven by misinformation. This isn’t a closing argument. It’s a reckoning.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Skye Bioscience, Inc. (SKYE) Securities Class Action Lawsuit Update [December 10, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/skye-alert-plus-banner.webp)

![Stride, Inc. (LRN) Securities Class Action Update [November 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/lrn-alert-plus-banner.webp)

![Primo Brands Corporation (PRMB) Securities Class Action Update [November 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/prmb-alert-plus-banner-image.webp)