![Stride, Inc. (LRN) Securities Class Action Update [November 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/lrn-alert-plus-banner.webp)

The Ghost Students That Haunt LRN Investors

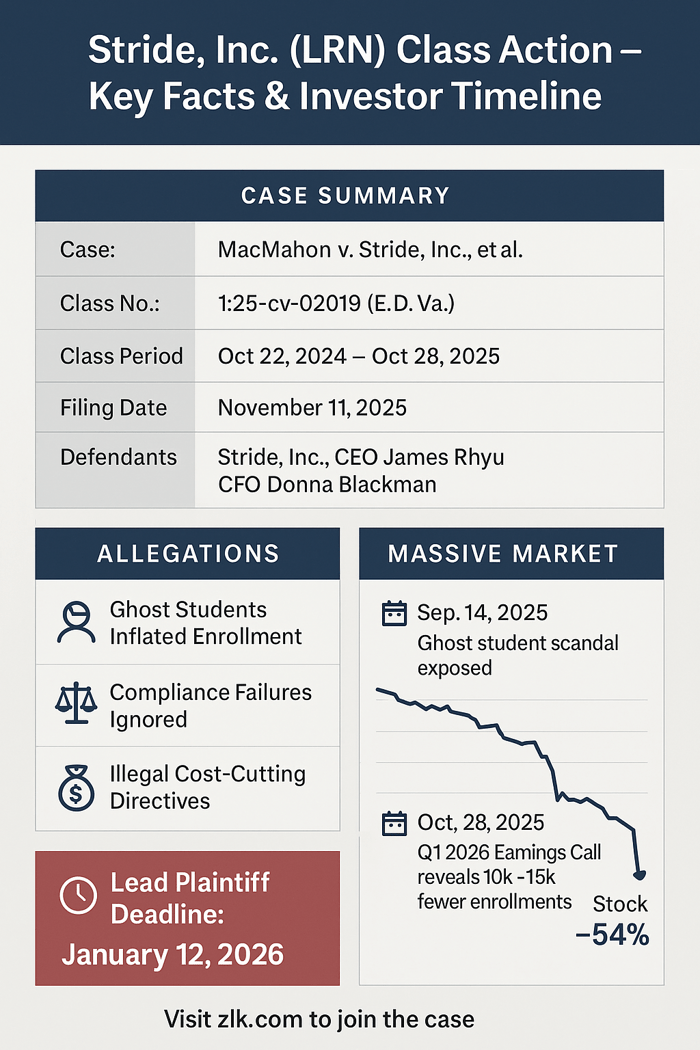

Case Name: Macmahon v. Stride, Inc., et al.

Case No.: 1:25-cv-02019

Jurisdiction: U.S. District Court, Eastern District of Virginia

Filed on: November 11, 2025

Class Period: October 22, 2024–October 28, 2025

Introduction

A reckoning has come for Stride, Inc. (NYSE: LRN), the nation’s prominent provider of online educational services. A recently filed securities class action lawsuit alleges that the digital learning company’s meteoric rise was constructed on a foundation of misrepresentation, specifically concerning its most vital metric: student enrollment. The complaint alleges Stride systematically misled investors during the Class Period by inflating its student rolls with "ghost students" and strategically undercutting essential compliance and staffing requirements to boost profit margins. This alleged deception, the lawsuit contends, culminated in two massive stock drops, wiping out billions in market capitalization and leaving LRN investors in financial devastation.

Backdrop and Business Context

Stride, formerly known as K12 Inc., operates in the intensely regulated K-12 and adult learning sectors, positioning itself as a leader in personalized, technology-based education. Its model hinges on partnering with state and local school districts to deliver virtual and blended learning curricula, a business that saw explosive interest and valuations in the wake of widespread pandemic-era school closures. The investment thesis for LRN was simple: sustainable enrollment growth coupled with operational leverage—the ability to grow revenue faster than costs. Stride’s deep educational, regulatory, and policy expertise, the company claimed, was its key competitive moat, allowing it to navigate the patchwork of state regulations where it operated. The entire investment narrative was predicated on the durable transfer of student demand into predictable, compliant, and profitable enrollment figures, setting the stage for what would become the central conflict of the lawsuit.

Promises Made vs. Reality

Throughout the Class Period, Stride presented an image of a well-governed company executing flawlessly on its growth strategy. The company routinely touted its operational stability and capacity for managing its regulated environment. It assured the market it was “one of the nation's most successful technology-based education companies” and lauded its “[d]eep educational, regulatory, and policy expertise”.

The reality, painted by the complaint, was a stark counter-narrative of management directives prioritizing profit over principle. While Stride boasted of enrollment figures, the lawsuit alleges the company was achieving them through fraudulent methods: retaining students who had withdrawn—the very definition of a "ghost student"—to artificially inflate official counts. Furthermore, the pursuit of "operational scale" allegedly involved assigning teachers caseloads far exceeding statutory limits, resulting in a breakdown of the promised "customer experience" and fundamental compliance failures, including a lack of necessary background checks and proper special education services. The discrepancy was a chasm between public pronouncements of compliance and the alleged internal reality of systemic regulatory negligence.

Timeline of Alleged Misconduct and Disclosures

The alleged scheme maintained its façade until two sharp disclosures punctured the optimistic narrative.

The Alleged Optimistic Narrative (The Class Period)

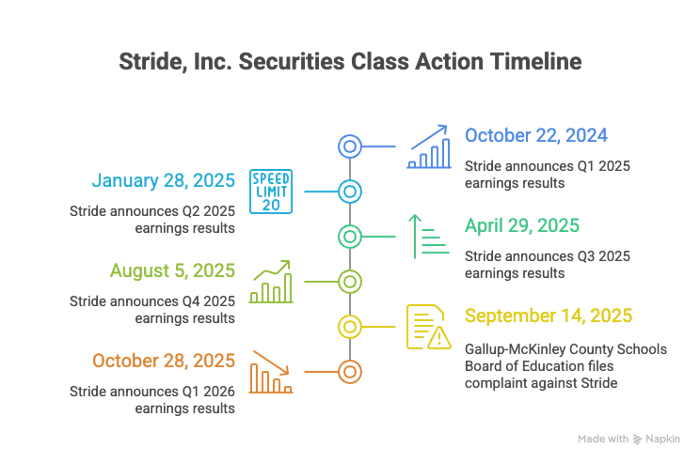

- October 22, 2024: Stride announced its Q1 2025 earnings results. CEO James J. Rhyu spoke of delivering "meaningful products and services to millions of students," and CFO Donna M. Blackman forecasted full-year 2025 revenue in the range of $2.225 billion to $2.3 billion.

- January 28, 2025: Stride announced its Q2 2025 earnings results, with CEO Rhyu stating that for three consecutive years, the business had seen "increasing growth" and that "The macro environment for our business is as strong as ever."

- April 29, 2025: Stride announced its Q3 2025 earnings results. CFO Blackman raised the full-year revenue guidance to a new range of $2.370 billion to $2.385 billion.

- August 5, 2025: Stride announced its Q4 2025 earnings results. CEO Rhyu stated that customers "continue to choose us in record numbers" and anticipated "double-digit enrollment growth this fall." CFO Blackman added that they expected year-over-year enrollment growth in the first quarter to be in the range of 10% to 15%.

The Disclosures and Market Reaction

- September 14, 2025: The first tremor hit when a report stated that the Gallup-McKinley County Schools Board of Education had filed a complaint against Stride. This complaint alleged fraud, deceptive trade practices, systemic legal violations, and intentional misconduct, including inflating enrollment numbers by retaining "ghost students" to secure state funding and ignoring compliance requirements.

- Market Reaction: Stride's stock fell $18.60 per share, or 11.7%, to close at $139.76 per share on September 15, 2025.

- October 28, 2025: The second, and far more devastating, blow landed on an earnings call for Q1 2026. CEO Rhyu announced that Stride experienced "approximately 10,000 to 15,000 fewer enrollments" than expected. Management attributed this to "poor customer experience" from upgraded platforms, which resulted in "higher withdrawal rates and lower conversion rates." Stride stated that its outlook for the year was "muted."

- Market Reaction: The price of Stride's stock dropped $83.48 per share, or more than 54%, to close at $70.05 per share on October 29, 2025.

Investor Harm and Market Reaction

The disclosures initiated a catastrophic deletion of shareholder equity. The $83.48 price drop following the October 28 guidance revision confirmed to investors that the underlying business model had been fundamentally compromised, a direct loss tied to the alleged misstatements about stable, compliant enrollment.

Prior to the September disclosure, analyst sentiment was deeply bifurcated. Some community models saw fair values as high as $218.15, while others held lower, yet still optimistic, targets. The market was already pricing in elevated expectations for the growth story. The lawsuit and its underlying allegations that management knowingly allowed compliance failures and inflated metrics shredded the high-growth thesis. The massive, immediate drop demonstrated that the market viewed the "poor customer experience" explanation not as an isolated issue, but as the inevitable consequence of the alleged aggressive and non-compliant cost-cutting and enrollment inflation strategy.

Litigation and Procedural Posture

The securities class action, filed in the Eastern District of Virginia, names Stride, Inc., CEO James J. Rhyu and CFO Donna M. Blackman, as defendants. The lawsuit asserts claims under the Securities Exchange Act of 1934, specifically Sections 10(b) and 20(a), as well as Rule 10b-5, which target fraudulent misrepresentations and omissions made in connection with the purchase or sale of securities.

The complaint details substantial allegations of scienter—the required state of mind suggesting intent to deceive or severe recklessness. The claim links the massive internal cost-cutting directives and suppression of whistleblower reports directly to the highest levels of management. For the litigation to proceed past the motion to dismiss phase, investors will need to demonstrate that the defendants either knew about the "ghost student" practice and compliance failures or acted with severe recklessness in overlooking them. The window for investors with substantial losses to seek appointment as Lead Plaintiff closes on January 12, 2026.

Shareholder Sentiment

Shareholder sentiment following the October collapse shifted from divided optimism to stark alarm. Before the disclosures, the narrative focused on LRN’s potential to disrupt traditional education, with community members on platforms like StockTwits and Reddit anticipating continued revenue growth.

Now, the tenor is overwhelmingly judicial. The online discussion is less about long-term potential and more about recovering capital. Numerous legal alerts flooded investor forums, creating an echo chamber of urgency. The collective digital voice is dominated by the deadlines to seek appointment as lead plaintiff for those who suffered substantial losses. Despite the legal turbulence, a contingent of value investors remains, evidenced by internal community valuation models that still see Stride's worth significantly above its post-drop price.

The sentiment is one of a profound betrayal; the fundamental belief in the company’s transparent execution has been replaced by a pervasive fear of governance risk. It is not merely a stock decline—it’s a violation of trust, a feeling of having been sold a phantom story.

Analyst Commentary

The immediate aftermath of the October 28 disclosure brought a wave of reassessment from professional analysts, even though the formal analyst consensus before the news was highly bullish, with a "Strong Buy" rating on a related sector. The sheer magnitude of the 54% price drop demonstrated an instant market downgrade.

The key observation from post-suit commentary is the re-prioritization of risk. While Stride had been lauded for its solid sales growth, analysts now must weigh these financial achievements against the legal allegations, recognizing that the short-term optimism was entirely focused on the now-discredited enrollment growth. The legal proceedings have introduced critical uncertainty regarding governance and regulatory compliance, risks that had previously been discounted. Though some longer-term analysts still forecast revenue growth toward $3.1 billion by 2028, the integrity of the data underpinning such forecasts is now deeply questionable. The focus has moved from "What are the fundamentals?" to "Is the management trustworthy?"

SEC Filings & Risk Factors

An examination of Stride’s relevant SEC filings—such as its annual report on Form 10-K—reveals that the company was acutely aware of the risks that now form the basis of the class action, but the lawsuit alleges management failed to appropriately mitigate or transparently disclose the existence of internal fraud.

Stride's filings historically included standard risk factors warning that its results could be materially affected by the "inability to achieve a sufficient level of new enrollments to sustain our business model" and the potential "failure of the schools we serve or us to comply with federal, state and local regulations, resulting in a loss of funding". Crucially, the filings also contained caveats about the "limitations of the enrollment data we present, which may not fully capture trends in the performance of our business".

While these are standard boilerplates, the complaint transforms them from general warnings into evidence of withheld truth. The lawsuit alleges that management did not just face the risk of enrollment data limitations or compliance failure; they allegedly caused the failure through the "ghost student" scheme and illegal cost-cutting directives. The omission of internal whistleblower reports about these specific, systemic issues becomes the most relevant "omitted risk" for investors.

Conclusion: Implications for Investors

The Stride class action serves as a reminder that in hyper-growth sectors like digital education, regulatory compliance and operational integrity are not simply costs of doing business—they are the core financial thesis. When a company's profit expansion relies on leveraging a public funding model, the numbers must be beyond reproach.

For investors, the key takeaway is the absolute necessity of scrutinizing metrics that rely on complex regulatory environments. The alleged use of "ghost students" to inflate revenue, combined with illegal cost-cutting through excessive teacher caseloads, is a red flag that transcends sector lines. Investors must view any sudden, massive decline in a company’s outlook—especially one attributed vaguely to "poor customer experience" after a period of reported strong growth—not as a market overreaction, but as the final, public collapse of a suppressed internal truth. When the market narrative centers on operational leverage, look for evidence that compliance and quality controls are being cut to achieve it. This isn't a closing argument. It's a reckoning for the promise of virtual learning.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal nor financial advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Jayud Global Logistics Limited (JYD) Securities Class Action Lawsuit Update [December 2, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/jyd-new-case-banner.png)

![Primo Brands Corporation (PRMB) Securities Class Action Update [November 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/prmb-alert-plus-banner-image.webp)

![Skye Bioscience, Inc. (SKYE) Securities Class Action Lawsuit Update [December 10, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/skye-alert-plus-banner.webp)