![Skye Bioscience, Inc. (SKYE) Securities Class Action Lawsuit Update [December 10, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/skye-alert-plus-banner.webp)

Nimacimab's Overstated Promise and the Clinical Fallout Exposed

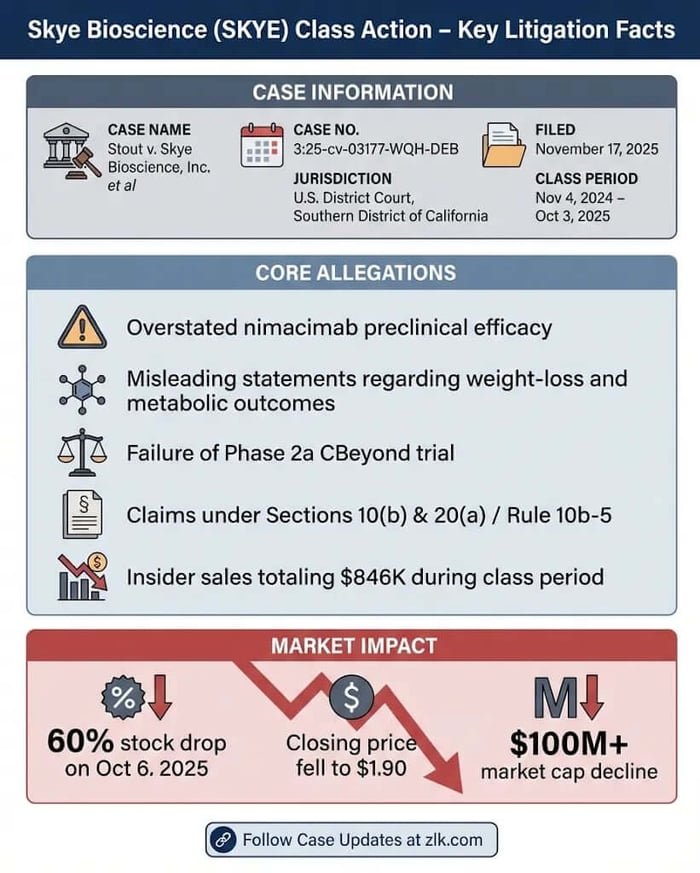

Case Name: Stout v. Skye Bioscience, Inc. et al

Case No.: 3:25-cv-03177-WQH-DEB

Jurisdiction: U.S. District Court, Southern District of California

Filed on: November 17, 2025

Class Period: November 4, 2024—October 3, 2025

Introduction

Skye Bioscience, Inc. promised a breakthrough in obesity treatment. Investors allege it delivered deception instead. The federal securities class action filed against the company and its top executives reveals a story of preclinical hype crashing against clinical reality, leaving shareholders to reckon with a 60% stock plunge. This case, centered on the CB1 inhibitor nimacimab, underscores the high-stakes gamble in biotech—where optimism can veil uncertainty, and failure arrives without warning.

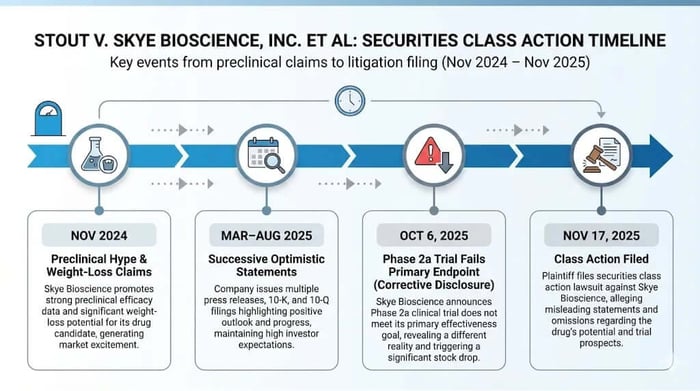

A federal securities class action lawsuit has landed in the U.S. District Court for the Southern District of California, Case No. 3:25-cv-03177-WQH-DEB, targeting Skye Bioscience, Inc. (NASDAQ: SKYE) and key executives Punit Dhillon (CEO), Kaitlyn Arsenault (CFO), and Christopher G. Twitty (CSO). Lead plaintiff Jeremy Stout, on behalf of purchasers of SKYE securities from November 4, 2024, to October 3, 2025, claims violations of Sections 10(b) and 20(a) of the Securities Exchange Act and Rule 10b-5. The core allegations? Defendants overstated nimacimab's efficacy in preclinical studies, misleading investors about its potential to deliver meaningful weight loss and metabolic benefits. This inflated SKYE's stock, only for the Phase 2a CBeyond trial to fail its primary endpoint on October 6, 2025, erasing $2.85 per share—or 60%—in a single day, closing at $1.90. For investors, the fallout raises familiar questions of scienter and loss causation in a sector where trial risks can devastate portfolios. Fund managers and class counsel should watch closely: insider sales during the period totaled over $846,000, adding fuel to claims of knowing misrepresentation.

Backdrop and Business Context

Skye Bioscience emerged as a clinical-stage biopharmaceutical player zeroed in on modulating G protein-coupled receptors (GPCRs) to tackle obesity, overweight, and metabolic disorders. Headquartered in San Diego, the Nevada corporation traded on NASDAQ under SKYE, building its narrative around nimacimab—a peripherally restricted negative allosteric modulator of the cannabinoid receptor type-1 (CB1). This mechanism aimed to inhibit CB1 signaling without crossing the blood-brain barrier, sidestepping neuropsychiatric side effects that doomed earlier small-molecule CB1 inhibitors.

The company went public through a traditional NASDAQ listing, not a SPAC, cultivating interest with promises of differentiated obesity treatments in a market dominated by GLP-1 agonists like semaglutide. Milestones piled up: In August 2024, Skye launched the CBeyond Phase 2a trial, a 26-week study testing nimacimab's weight-loss potential alone and combined with semaglutide. Preclinical data from diet-induced obesity (DIO) mouse models fueled the buzz, showing dose-dependent weight loss up to 16% and metabolic improvements. Yet this setup masked vulnerabilities. As a single-product focus in a high-failure-rate field, Skye's fortunes hinged on nimacimab translating animal results to humans—a leap that, investors allege, executives knew was riskier than portrayed.

Promises Made vs. Reality

Skye's public narrative painted nimacimab as a game-changer. In a November 4, 2024, press release, the company highlighted preliminary DIO model data: "[P]eripherally-restricted nimacimab achieve[d] significant dose-dependent weight loss" and "[p]reliminary data shows that nimacimab achieves desired metabolic outcomes." Three days later, CEO Dhillon reinforced this on an earnings call: "We believe nimacimab’s first-in-class profile as a perfectly targeting CB1 inhibitor offers the right combination of efficacy and safety." The Q3 2024 10-Q echoed the theme, touting nimacimab's potential to "positively impact metabolic disorders including obesity."

This optimism escalated. By March 20, 2025, Dhillon declared in a press release: "Skye’s prime accomplishment in 2024 was the initiation and rapid advancement of its comprehensive Phase 2a clinical study of nimacimab... We believe nimacimab’s product profile is well-positioned to potentially fulfill critical unmet needs." The 2024 10-K claimed nimacimab "stands apart from GLP-1’s... because its primary mechanism goes beyond suppression of food intake," citing preclinical models for lean mass preservation and insulin sensitivity. April 15, 2025, data boasted over 30% weight loss in combination with tirzepatide. May 8, 2025, filings and calls emphasized "superior potency" over competitors like monlunabant.

Reality, per the complaint, diverged sharply. No confidential witnesses or whistleblowers are cited—allegations stem from public discrepancies—but the Phase 2a failure exposed the gap. Nimacimab monotherapy achieved only -1.52% weight loss versus placebo's -0.26%, with lower-than-expected exposure suggesting suboptimal dosing. Investors argue these risks were downplayed, as preclinical hype ignored translational uncertainties that internal analyses likely flagged.

Timeline of Alleged Misconduct and Disclosures

The class period opens November 4, 2024, with preclinical DIO data touting nimacimab's weight-loss prowess. November 7 follows with Q3 results and Dhillon's call, framing nimacimab as "truly peripherally-restricted" with "significant opportunity." Misstatements build: March 20, 2025, Q4/FY 2024 release and 10-K hype the drug's "differentiated mechanism." April 15 data claims 30%+ combination weight loss. May 8 Q1 results highlight "superior potency." June 23 video series calls nimacimab a "new frontier." August 7 Q2 results assert "superior weight rebound profile."

Media coverage amplified the narrative—analyst notes praised potential synergies with GLP-1s—until October 6, 2025. Skye's press release admits monotherapy failure due to low exposure, triggering the 60% drop. The lawsuit, filed November 17, cites this as the corrective disclosure, with no prior "early tremors" like whistleblower reports.

Investor Harm and Market Reaction

The October 6 revelation erased $2.85 per share, a 60% freefall to $1.90 on heavy volume, vaporizing over $100 million in market cap. Jeremy Stout's certification details purchases at $3.975 and $3.91, crystallizing losses for those buying near peaks. Broader harm ties to fraud-on-the-market: inflated prices from preclinical hype lured investors, only for trial failure to reveal overstated efficacy.

Analyst downgrades followed swiftly. Pre-drop targets hovered around $10-15; post-disclosure, firms slashed to $2-4, citing "execution risks" and "suboptimal dosing." Trading volume spiked 500%, signaling panic sales. No subsequent recoveries—SKYE lingered below $2, underscoring permanent erosion for long-term holders.

Litigation and Procedural Posture

Claims invoke Section 10(b)/Rule 10b-5 for primary liability and Section 20(a) for control-person accountability. Scienter allegations hinge on executives' access to trial data, yet persistent touting of preclinical "potency" despite red flags. Insider sales—Dhillon's 82,910 shares for $413,925; Arsenault's 86,612 for $432,406—bolster motive claims. No confidential witnesses, but fraud-on-the-market presumes reliance.

Filed November 17, 2025, the case demands class certification, damages, and jury trial. Milestones loom: lead plaintiff deadline, motion to dismiss likely by Q1 2026. Pomerantz LLP leads, emphasizing executives' SOX certifications as evidence of recklessness.

Shareholder Sentiment

Online forums captured raw frustration as SKYE's promise unraveled. On Stocktwits, users vented disbelief. Users on X (formerly Twitter) echoed the pain, with one post lamenting, “What is the level of greed when market makers allegedly try to destroy a small public company working on a cure for cancer?” Trends showed a pre-disclosure buzz around differentiated CB1 giving way to post-failure hashtags like #SKYEfail and calls for accountability.

Analyst Commentary

Before the drop, coverage leaned positive but measured. Cantor Fitzgerald's September 2025 note rated Overweight at $14. Piper Sandler was even more aggressive, holding an Overweight/$20 target into the readout and highlighting the upcoming 52-week extension data expected in H1 2026.

Post-October 6, the tone soured. Oppenheimer slashed its price target to $10 from $17 the same week, acknowledging the pharmacokinetic surprise while clinging to combination upside, noting exposure-response trends that suggest higher doses could unlock efficacy without mechanistic flaws. Industry publications framed the event in stark terms, with one headline reading, “Skye Bioscience stock plummets after failed weight loss drug trial.”

SEC Filings & Risk Factors

Skye's 2024 10-K (March 20, 2025) disclosed standard biotech perils: "Clinical trials may fail to demonstrate safety and efficacy," with specifics on nimacimab's Phase 2 uncertainties, including "potential for suboptimal dosing" and "failure to meet endpoints." Yet plaintiffs argue these were boilerplate, omitting known gaps in preclinical-to-clinical translation. The Q1 2025 10-Q (May 9) referenced no material risk changes, despite hyping DIO data. Q2 2025 10-Q (August 7) warned of "dependence on nimacimab success," but framed rebound benefits positively.

The October 6 8-K laid bare the failure: "Nimacimab monotherapy did not meet primary endpoint... lower than expected drug exposure." Omitted risks, per the suit, included over-reliance on mouse models without flagging human variability. Management's SOX certifications affirmed no material weaknesses, now scrutinized as evidence of oversight lapses.

Conclusion: Implications for Investors

This case distills biotech's peril: when preclinical narratives outpace clinical proof, the reckoning hits hard. For fund managers, red flags include over-dependence on a single asset and insider sales amid hype. Class counsel see a blueprint for scienter claims in mismatched data. Broader lesson for the sector—especially obesity plays—lies in transparency around translational risks. Investors chasing next-gen therapies must demand rigor over rhetoric. Now, they push back through the courts.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Jayud Global Logistics Limited (JYD) Securities Class Action Lawsuit Update [December 2, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/jyd-new-case-banner.png)

![Stride, Inc. (LRN) Securities Class Action Update [November 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/lrn-alert-plus-banner.webp)

![Primo Brands Corporation (PRMB) Securities Class Action Update [November 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/prmb-alert-plus-banner-image.webp)