![Alexandria Real Estate Equities, Inc. (ARE) Securities Class Action Lawsuit Update [December 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/are-alert-plus-banner.webp)

ARE Securities Class Action Centers on Long Island City Write-Down and Leasing Claims

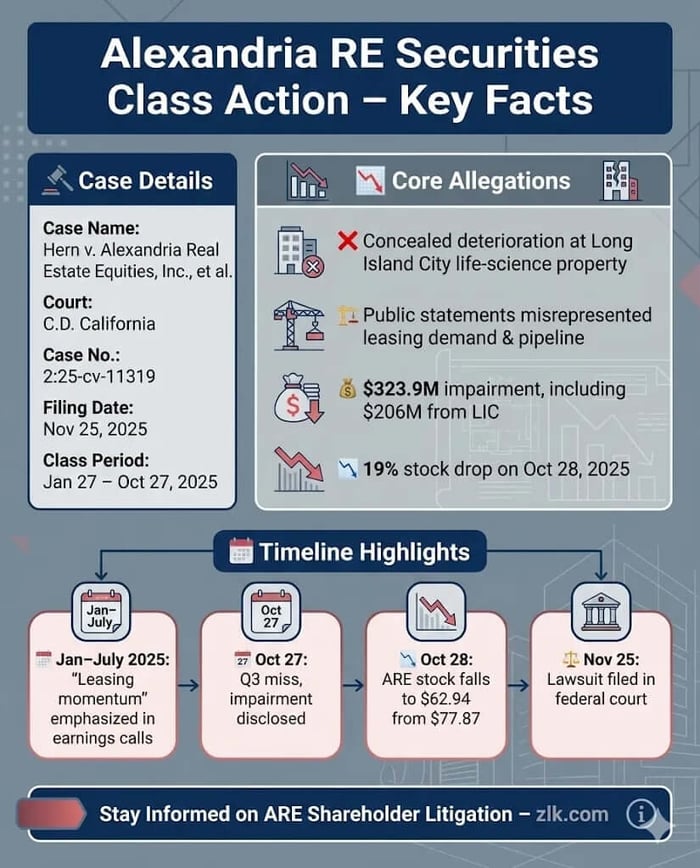

Case Name: Hern v. Alexandria Real Estate Equities, Inc., et al.

Case No.: 2:25-cv-11319

Jurisdiction: U.S. District Court, Central District of California

Filed on: November 25, 2025

Class Period: January 27, 2025 - October 27, 2025

Introduction

Alexandria Real Estate Equities, Inc. said its leasing engine was humming. Investors say it wasn’t.

On November 25, 2025, a federal securities class action was filed in the U.S. District Court for the Central District of California against Alexandria Real Estate Equities, Inc. (NYSE: ARE) and senior executives Peter M. Moglia, Marc E. Binda, and Joel S. Marcus. The complaint alleges that during the Class Period from January 27, 2025 through October 27, 2025, defendants repeatedly assured investors that leasing demand, occupancy stability, and growth prospects for Alexandria’s life-science portfolio remained solid—while concealing a long-running deterioration at its Long Island City, New York property.

The reckoning arrived on October 27, 2025. Alexandria disclosed a $323.9 million real estate impairment, including approximately $206 million tied to Long Island City, cut full-year FFO guidance, and acknowledged that the site was no longer viable as a scalable life-science destination. The stock fell roughly 19% in a single day. Investors sued soon after.

Backdrop and Business Context

Alexandria Real Estate Equities is a REIT focused on life-science campuses—labs, research facilities, and office space clustered in innovation hubs such as Greater Boston, San Diego, the Bay Area, Seattle, and New York City. Its business model centers on what it brands as “Megacampus™” ecosystems: dense portfolios of specialized properties designed to lock in large pharmaceutical and biotech tenants over long lease terms.

During the Class Period, Alexandria emphasized scale, tenant loyalty, and development visibility. Executives repeatedly highlighted leasing volumes exceeding one million rentable square feet per quarter, high occupancy rates in North America, and a pipeline positioned to capture future demand as capital markets normalized. Long Island City was presented as aligned with that strategy—another node in a national life-science network.

According to the complaint, that narrative masked a more uncomfortable truth: LIC had struggled for years to attract and retain life-science tenants, suffered from structural demand issues after Amazon abandoned plans for a nearby HQ in 2019, and never achieved the critical mass management publicly implied.

Promises Made vs. Reality

From the opening weeks of 2025, Alexandria’s messaging was consistent and confident.

In January 2025, the company reported “continued solid leasing volume,” stable occupancy, and momentum heading into the year. Executives told analysts that Alexandria’s pipeline was “well positioned to capture future demand,” supported by tenant loyalty and scale advantages. CFO Marc Binda emphasized that leasing volume had exceeded one million square feet for four consecutive quarters and that occupancy remained “solid.”

Those assurances continued through April and July 2025. Management reaffirmed FFO guidance, reiterated confidence in leasing spreads, and described development and redevelopment projects as gaining traction despite a muted biotech funding environment. When asked directly about demand inflection points, executives urged patience—suggesting good news was coming.

Investors allege those statements were materially misleading. According to the complaint, Alexandria internally knew that LIC was failing as a life-science hub, that leasing velocity there had been declining for years, and that the property’s highest and best use was no longer aligned with management’s public portrayal. None of that, plaintiffs say, was disclosed until the impairment forced the issue.

Timeline of Alleged Misconduct and Disclosures

The alleged misconduct unfolded gradually, then all at once.

From January through July 2025, Alexandria issued quarterly earnings releases and held earnings calls touting leasing momentum, occupancy stability, and long-term growth visibility. Management repeatedly reassured analysts that development deliveries in 2025 and 2026 were in “pretty good shape” and that no material changes to capital allocation were expected.

On October 27, 2025, the tone shifted abruptly. After market close, Alexandria reported third-quarter results below expectations, cut full-year FFO guidance, and disclosed a $323.9 million impairment charge—two-thirds of it tied to Long Island City. The next day, executives acknowledged on the earnings call that LIC had failed to scale as a life-science destination and would be better recycled into other Megacampuses.

The market reaction was swift. ARE shares fell from $77.87 on October 27 to $62.94 on October 28, erasing nearly one-fifth of the company’s market value in a single session.

Investor Harm and Market Reaction

Plaintiffs allege classic loss causation. Alexandria’s stock price, they say, was artificially inflated by repeated statements about leasing strength, occupancy, and pipeline visibility—particularly as those claims related to LIC. When the truth emerged through the impairment disclosure and guidance cut, the inflation dissipated.

The one-day decline of approximately 19% translated into billions in market capitalization losses. Analysts responded by slashing price targets and reframing their outlook. Analysts responded by slashing price targets and reframing their outlook, including Citizens JMP which downgraded to Market Perform from Outperform, Cantor Fitzgerald which lowered target (e.g., to $79, later further cuts), and BMO Capital which lowered to $60 from $67.

Litigation and Procedural Posture

The complaint asserts claims under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and Rule 10b-5. Defendants include Alexandria and its CEO, CFO, and principal executive officer.

Plaintiffs allege scienter based on defendants’ access to internal leasing data, direct involvement in property strategy, repeated detailed commentary on LIC and the pipeline, and the magnitude and timing of the impairment. The case is in its early stages; no motion to dismiss has yet been adjudicated.

The litigation will likely turn on whether optimistic statements about leasing demand and occupancy constituted actionable misrepresentations or non-actionable corporate optimism—and whether LIC’s deterioration was a known trend that should have been disclosed earlier.

Shareholder Sentiment

Investor reaction following the October disclosure reflected shock more than surprise. On X, users questioned how a property written down by over $200 million could have been discussed as strategically sound only months earlier, with recurring themes of “management blind spots,” “overconfidence in Megacampus branding,” and frustration with guidance reversals. For instance, one post highlighted the market pricing $ARE like “Office 2.0” after the LIC impairment and dividend cut, asking: "Is this capitulation or a value trap?"

Post-disclosure sentiment skewed sharply negative on platforms like X, Reddit, and Stocktwits, but some optimism emerged from insider activity, such as Director Sheila K. McGrath's purchase of 3,100 shares at $45.60 on Dec 10, 2025, signaling confidence amid the drop. Pre-disclosure optimism gave way to skepticism—particularly among income-focused REIT investors drawn to Alexandria for perceived stability.

Analyst Commentary

Sell-side analysts echoed those concerns. Following the Q3 disclosure, multiple firms reduced price targets and revised long-term assumptions about life-science demand recovery. Analysts cited longer-than-expected leasing downtimes, capital recycling uncertainty, and structural challenges in certain submarkets. For instance, one analysis highlighted that the stock "plunged 25% after Q3 2025 results, driven by oversupply fears and weak 2026 FFO guidance."

Notably, commentary emphasized that prior models had relied heavily on management’s repeated assertions about leasing momentum and pipeline visibility. Once those assumptions were withdrawn, valuation frameworks shifted accordingly, with another noting that "ARE's 9-cent miss for Q3-2025 was a pretty bad omen in itself."

SEC Filings & Risk Factors

Throughout the Class Period, Alexandria’s SEC filings acknowledged general macro risks—biotech funding cycles, interest rates, and development costs—but, according to plaintiffs, failed to disclose the specific, long-running deterioration at Long Island City.

Only after the impairment did Alexandria’s Form 8-K and earnings disclosures acknowledge that LIC was unlikely to function as a scalable life-science hub and that additional impairments could follow. Investors allege those risks should have been disclosed earlier, particularly given management’s repeated emphasis on LIC’s strategic alignment with the Megacampus model.

Conclusion: Implications for Investors

The Alexandria case is not about a missed quarter. It is about narrative control.

Investors allege that management framed localized structural weakness as temporary noise, leaning on branding, scale, and optimism until accounting reality intervened. For REIT investors, the case underscores a familiar lesson: when valuation rests on long-dated development assumptions and specialized demand, transparency around underperforming assets matters.

Whether the lawsuit survives a motion to dismiss remains to be seen. But the episode has already reshaped how the market views Alexandria’s growth story. The Megacampus may endure. The illusion of uniform strength did not.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![F5, Inc. (FFIV) Securities Class Action Lawsuit Update [December 22, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/ffiv-alert-plus-banner.webp)

![PubMatic, Inc. (PUBM) Securities Class Action Lawsuit Update [November 27, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/pubm-alert-plus-banner.webp)

![Sprouts Farmers Market, Inc. (SFM) Securities Class Action Lawsuit Update [December 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/sfm-alert-plus-banner.webp)