Table of Contents

- Defining Insider Trading: Understanding the Basics

- Civil Penalties for Insider Trading: A Closer Look

- Criminal Penalties: When Insider Trading Becomes a Felony

- Beyond the Courtroom: Additional Consequences

- High-Profile Insider Trading Cases

- Securities Class Actions and Shareholder Rights

- Preventive Measures and Compliance Best Practices

- The Importance of Civil Enforcement

- FAQs

Introduction

Insider trading is a critical issue at the intersection of law, finance, and ethics. It involves the buying or selling of securities by individuals who possess material, nonpublic information about a company.

The practice threatens the integrity of financial markets, undermines investor confidence, and distorts the level playing field essential for fair trading.

Regulators such as the U.S. Securities and Exchange Commission (SEC) and the Department of Justice (DOJ) are tasked with detecting, investigating, and penalizing insider trading to maintain public trust and market stability.

Defining Insider Trading: Understanding the Basics

What Is Insider Trading?

The prohibition against insider trading comes from Rule 10(b)-5 of the Securities Exchange Act. In a number of cases, U.S. Courts interpreted Rule 10(b)-5 to prohibit trading based on material, nonpublic information if that trading would breach a fiduciary duty.

This information, often referred to as “material nonpublic information” (MNPI), is any confidential data that could influence an investor’s decision to buy or sell a security.

Examples include knowledge of upcoming mergers, financial results, or significant corporate events.

Legal vs. Illegal Insider Trading

Not all insider trading is illegal. Legal insider trading occurs when corporate insiders—such as officers, directors, and employees—buy or sell stock in their own companies and report these trades to the SEC as required by law (Section 16(a) and 16(b)).

Illegal insider trading, by contrast, occurs when individuals trade based on material nonpublic information (MNPI) in breach of a fiduciary duty or a relationship of trust and confidence. As per Rule 10(b)-5 of the Securities Exchange Act of 1934, both the person who leaks the information (the “tipper”) and the recipient who trades on it (the “tippee”) can be held liable.

The Legal Framework Governing Insider Trading

SEC Enforcement Authority

The SEC derives its enforcement authority from the Securities Exchange Act of 1934, which was enacted to restore investor confidence after the 1929 stock market crash.

The Act empowers the SEC to regulate securities markets and enforce rules against fraud, including insider trading.

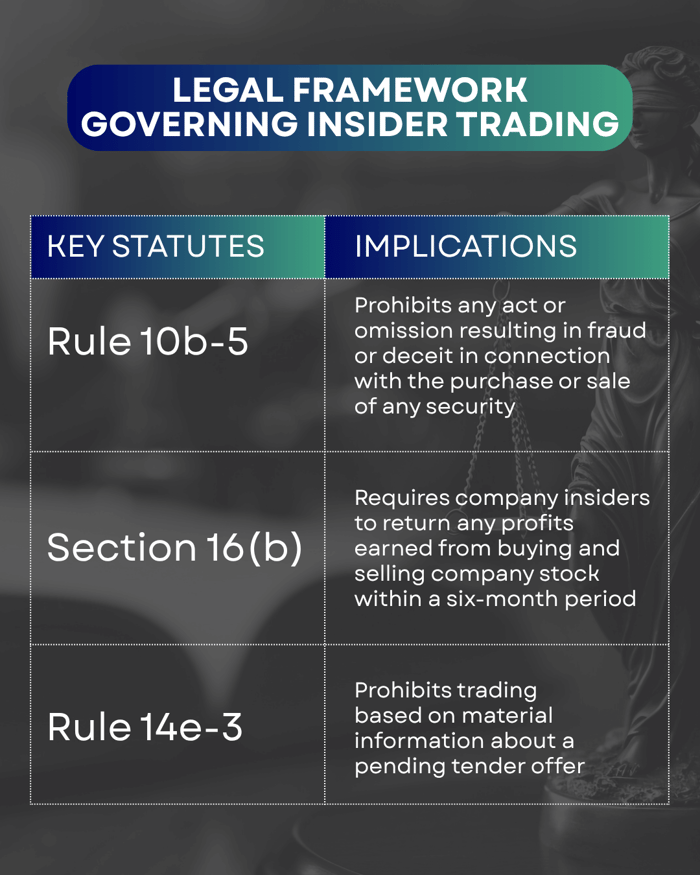

Key Statutes

- Rule 10b-5: The cornerstone of federal insider trading law, Rule 10b-5 prohibits any act or omission resulting in fraud or deceit in connection with the purchase or sale of any security. It covers classical insider trading, tipper/tippee liability, and misappropriation of information.

- Section 16(b): Known as the “short-swing profit rule”, Section 16(b) requires company insiders to return any profits earned from buying and selling company stock within six months. This provision serves as a deterrent against speculative trading by insiders.

- Rule 14e-3: Specifically targets insider trading in the context of tender offers, prohibiting trading based on material information about a pending tender offer, regardless of whether a fiduciary duty has been breached.

SEC Detection and Investigation

The SEC utilizes sophisticated market surveillance tools, data analytics, and artificial intelligence to monitor trading patterns and identify anomalies that may indicate insider trading.

Investigations often begin with market surveillance, tips from whistleblowers (as outlined in Section 21F of the Securities Exchange Act of 1934), or complaints from investors.

The SEC collaborates with other regulatory bodies and utilizes subpoenas, interviews, and analysis of trading records to build cases.

Civil Penalties for Insider Trading: A Closer Look

Civil penalties for insider trading are the most frequently imposed consequence for insider trading violations, reflecting the SEC’s primary role as a civil enforcement agency.

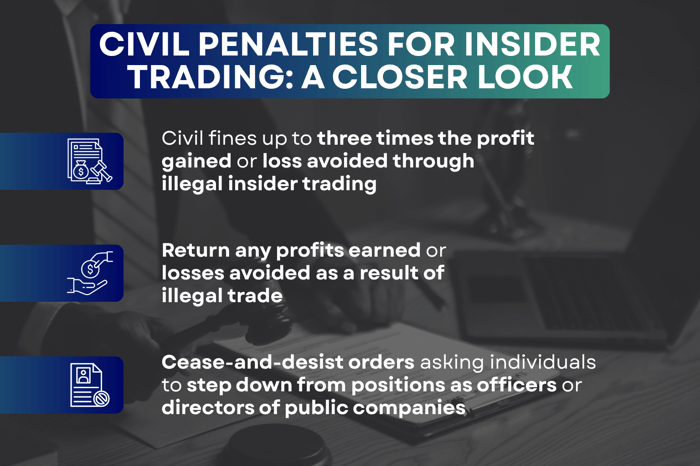

1. Fines Imposed by the SEC

As per the Insider Trading Sanctions Act of 1984 (ITSA) and Section 21A of the Exchange Act, the SEC can impose civil fines up to three times the profit gained or loss avoided through illegal insider trading—commonly referred to as “treble damages”.

These penalties are designed to strip wrongdoers of their ill-gotten gains and deter future misconduct.

2. Disgorgement of Ill-Gotten Gains

Disgorgement requires violators to return any profits earned or losses avoided as a result of illegal trades (Section 21(d)(5) and Section 21(d)(7) of the Exchange Act).

This restitutionary payment is made to ensure that offenders do not benefit from their misconduct.

3. Injunctions and Bars

As per sections 21(d), 21(c), and 21(d)(2) of the Securities Exchange Act of 1934, the SEC may seek court orders—such as injunctions or cease-and-desist orders—to prevent individuals from serving as officers or directors of public companies or from engaging in future violations.

Industry bars can be permanent or temporary, depending on the severity of the offense.

Real-World Impact

A civil penalty for insider trading can lead to financial ruin, irreparable reputational harm, and permanent professional consequences.

Even being investigated for insider trading can result in loss of employment, professional licenses, and future career opportunities.

Levi & Korsinsky’s Experience

Levi & Korsinsky is recognized for its experience in pursuing civil remedies on behalf of investors harmed by insider trading. The firm leverages securities litigation to recover losses and hold wrongdoers accountable, providing a vital avenue for investor protection.

Criminal Penalties: When Insider Trading Becomes a Felony

While the SEC handles civil enforcement, the DOJ (Securities Exchange Act of 1934) is responsible for criminal prosecution of insider trading cases.

Criminal charges are typically brought when the conduct is particularly egregious or involves large sums of money.

a) Federal Prosecution

The DOJ can prosecute insider trading as a felony, with penalties including imprisonment for up to 20 years per violation (section 32(a) of the Securities Exchange Act of 1934).

Criminal fines can reach up to $5 million for individuals and $25 million for corporations.

b) Asset Forfeiture and Dual Liability

In addition to prison and fines, convicted individuals may face asset forfeiture—losing property or funds connected to the illegal activity.

It is also common for both civil and criminal proceedings to be pursued simultaneously, increasing the stakes for defendants.

Beyond the Courtroom: Additional Consequences

Insider trading convictions carry consequences beyond legal penalties:

- Loss of Professional Licenses: Convicted individuals may lose securities licenses, legal credentials, or other professional certifications, effectively ending their careers.

- Ineligibility for Employment: Many industries bar individuals with insider trading convictions from holding certain positions or regulatory approvals.

- Shareholder Derivative Suits: Shareholders can initiate derivative lawsuits against insiders who breach their fiduciary duties, seeking to recover losses on behalf of the company.

High-Profile Insider Trading Cases

Several high-profile cases highlight the far-reaching consequences of insider trading:

- Raj Rajaratnam (Galleon Group): Rajaratnam was convicted on 14 counts of conspiracy and securities fraud for orchestrating an extensive insider trading network, resulting in over $70 million in illicit gains and a lengthy prison sentence.

- Jeffrey Skilling (Enron): The former Enron CEO sold millions in stock before the company’s collapse, exploiting nonpublic information. The scandal led to significant regulatory reforms, including the enactment of the Sarbanes-Oxley Act.

- Recent SEC Actions: In 2024, the SEC secured an $18 million civil penalty against J.P. Morgan for insider trading violations, demonstrating the continued rigor of enforcement.

These cases highlight how civil penalties can result in substantial recoveries for shareholders and prompt regulatory changes.

Securities Class Actions and Shareholder Rights

Illegal insider trading frequently gives rise to securities class action lawsuits, enabling shareholders to seek compensation for losses resulting from fraudulent conduct.

Levi & Korsinsky has extensive experience representing shareholders in insider-related fraud cases, advocating for investor rights, and maximizing recoveries for clients.

With over 80 collective years of experience, our experienced attorneys are on hand to provide you with the support and legal expertise you need to maximize your recovery.

- Current Class Actions: For a list of ongoing cases, visit zlk.com/cases.

- Check Eligibility: Investors can verify their eligibility to join a class action at compensationrecovery.com.

Preventive Measures and Compliance Best Practices

Best Practices for Insiders and Investors

- Blackout Periods: Companies often impose blackout periods during which insiders are prohibited from trading, especially around earnings releases or major corporate events.

- Form 4 Filings: Corporate officers and directors must promptly disclose trades in their company’s securities via Form 4 filings, ensuring transparency and regulatory compliance.

- Material Nonpublic Information (MNPI): Insiders must avoid trading when in possession of MNPI and should implement robust compliance programs to monitor and restrict access to sensitive information.

Tips to Avoid Regulatory Scrutiny

- Establish and follow written trading plans (such as Rule 10b5-1 plans) to provide a defense against accusations of insider trading.

- Maintain clear records of all trades and ensure timely disclosure as required by the Securities and Exchange Commission (SEC).

- Educate employees and executives on insider trading laws and company policies to ensure compliance.

The Importance of Civil Enforcement

Civil penalties are essential to protecting market integrity and deterring misconduct. They empower regulators and private litigants to recover losses and restore investor confidence.

If you have been affected by insider trading and aim to seek legal counsel to check on measures for maximizing your recovery through a securities class action lawsuit, Levi & Korsinsky has got you covered.

Over the past 20 years, Levi & Korsinsky has established itself as a nationally-recognized securities litigation firm that has secured hundreds of millions of dollars for aggrieved shareholders and built a track record of winning high-stakes cases.

With over 80 collective years of experience, our experienced attorneys are on hand to provide you with the support and legal expertise you need to maximise your recovery.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal advice. Readers should not act or refrain from acting on any of the information contained in this blog without consulting a qualified legal professional. Levi & Korsinsky LLP is not responsible for any actions taken or not taken based on the information provided in this blog.

You Can Also Read... |

FAQs

What are civil penalties for insider trading?

Civil penalties include fines up to three times the profit gained or loss avoided, disgorgement of ill-gotten gains, and injunctions or industry bars.

Can shareholders sue for insider trading?

Yes. Shareholders can bring derivative suits to recover losses on behalf of the company, and class actions are commonplace in cases of widespread harm.

What’s the difference between criminal and civil enforcement?

Civil enforcement (by the SEC) results in monetary penalties and injunctions, while criminal enforcement (by the DOJ) can result in imprisonment and higher fines.

How long does it take to recover compensation?

The timeline varies by case complexity, but class actions and SEC enforcement actions can take several months to years to resolve.

How can I file or join a class action if I suspect insider misconduct?

Visit zlk.com/cases for current class actions or check eligibility at compensationrecovery.com.

![Organon & Co. (OGN) Securities Class Action Lawsuit Update [June 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/organon-lawsuit-key-facts.webp)

![DoubleVerify Holdings, Inc. (DV) Securities Class Action Lawsuit Update [June 20, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/doubleverify-lawsuit-banner.webp)