Table of Contents

When investors who have suffered similar financial losses due to alleged violations of securities laws, often involving deceptive statements, omissions, or fraudulent conduct by publicly traded companies, they may group together to seek legal remedy through a class action.

This guide attempts to help investors understand the essential requirements for a securities class action lawsuit and litigation.

Importance of Understanding the Requirements and Legal Framework

Class action lawsuits are governed by a labyrinth of federal statutes, judicial precedents, and procedural rules that set a high bar for plaintiffs. Understanding these requirements is essential for:

- Protection of investor rights at each step of the litigation process.

- Maximizing potential recoveries to compensate for the losses incurred due to unlawful activity.

- Ensure all the affected investors are equally represented and claims are not dismissed.

Key Legislative Acts Governing Securities Class Actions

The Securities Act of 1933

The Securities Act of 1933 (“Securities Act”) was enacted after the 1929 stock market crash with two main objectives: enabling investors to make informed investment decisions through increased financial transparency in financial statements and enacting laws against misrepresentations and fraudulent activities in securities markets. It is frequently invoked in class actions involving initial public offerings (IPOs) or secondary offerings where material information was misstated or withheld.

Key provisions include:

- Registration Requirements: Any company offering securities must file a registration statement with the SEC, disclosing material information about the company and the offering.

- Liability for Misstatements: The Securities Act imposes strict liability for material misstatements or omissions in registration statements or prospectuses.

- Private Right of Action: Investors harmed by violations of the Securities Act can bring private lawsuits, including class actions, to recover losses.

The Securities Exchange Act of 1934

The Securities Exchange Act of 1934 (“Exchange Act”) was created to restore investor confidence in the capital markets after the stock market crash of 1929. The Exchange Act governs securities transactions on the secondary market after they have been issued and was the key legal framework behind the inception of the Securities and Exchange Commission (SEC). The goal of the Exchange Act is to ensure increased financial transparency and accuracy and ensure less fraud or manipulation. It is central to claims involving ongoing misstatements, market manipulation, or insider trading. Key provisions relevant to class actions include:

- Section 10(b) and Rule 10b-5: Prohibit fraud, misrepresentation, and deceit concerning the purchase or sale of securities.

- Continuous Disclosure Obligations: Market-listed companies must file periodic reports and promptly disclose material events.

- Private Right of Action: Under Rule 10b-5, the courts have recognized an implied private right of action, forming the basis for most securities fraud class actions.

Private Securities Litigation Reform Act of 1995

The Private Securities Litigation Reform Act (PSLRA) was enacted in 1995 to address concerns about the prevalence of frivolous and unwarranted securities lawsuits in the private securities litigation system.

In addition to other items, the PSLRA raised the pleading requirements, such as increasing the amount of evidence that plaintiffs must submit before filing a securities class action lawsuit. Its key provisions include:

- Heightened Pleading Standards: Plaintiffs must specify each allegedly misleading statement, explain why it is deceptive, and allege facts supporting a strong inference of scienter (intent to deceive).

- Lead Plaintiff Provisions: The court appoints the investor with the largest financial interest as the lead plaintiff, giving institutional investors a greater role.

- Discovery Stay: This provision allows courts to prevent costly expeditions. Discovery shall be stayed until the court rules on motions to dismiss.

- Sanctions for Frivolous Claims: Courts may impose penalties for baseless litigation.

Requirements for Filing a Securities Class Action Lawsuit

Class Period and Eligibility Criteria

In a securities class action lawsuit, the class period is the specific timeframe during which the plaintiffs allege the company violated securities laws through means such as fraud or misstatements. Investors who purchased or sold the security and suffered a loss due to the defendants alleged misconduct, during the class period become eligible to participate in the class action.

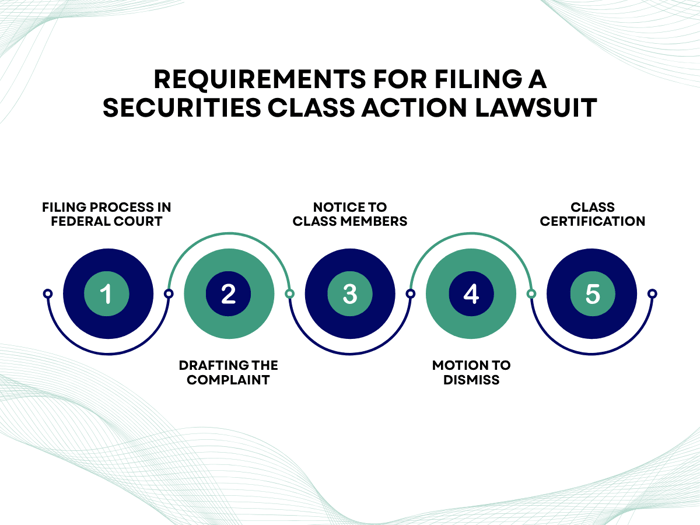

Filing Process in Federal Court

The process for filing a securities class action typically includes:

- Drafting the Complaint: The complaint must allege specific violations, identify misleading statements or omissions, and explain how these harmed investors.

- Notice to Class Members: Under the PSLRA, a notice must be published to alert potential class members and invite them to seek appointment as lead plaintiff.

- Motion to Dismiss: Defendants often challenge the complaint's sufficiency, and courts rigorously apply heightened pleading standards.

- Appointing a Lead Plaintiff: The court appoints a lead plaintiff to play a specific role in the litigation process. The lead plaintiff is usually characterized as the investor with the most significant financial interest in the class action lawsuit

- Class Certification: Plaintiffs must move for class certification under Rule 23 of the Federal Rules of Civil Procedure (FRCP), demonstrating numerosity, commonality, typicality, and adequacy of representation, among other requirements.

Appointment of Lead Plaintiff and Their Role

The court appoints a lead plaintiff, and their role can shape the trajectory of the securities class action. Their responsibilities include:

- Active participation in the litigation and works directly with class counsel

- Represents the interests of all class members in negotiations and court proceedings

- Approves major decisions, including settlements

Investor Rights and Responsibilities

Class members in securities class action lawsuits have specific rights. These include:

- Right to Participate: Class members have the right to receive notice of the lawsuit, including information about settlements and any significant developments in the case.

- Right to Object: Class members can object to any proposed settlement terms or attorney's fees if they believe the terms are unfair or unreasonable.

- Right to Recover Losses: If the court rules in favor of the class, class members may submit claims to recover their share of any settlement or judgment.

Importance of Document Preservation

Additionally, the class members must follow certain things to maximize their recovery. Investors should:

- Maintain accurate records of securities purchases and sales during the class period.

- Submit claim forms and supporting documentation promptly.

Failure to keep records or submit claims can result in forfeiture of recovery rights.

Once a lawsuit has been filed, both plaintiffs and defendants must preserve all relevant documents and communications. Failure to do so can result in sanctions or adverse inferences.

Next Steps for Investors

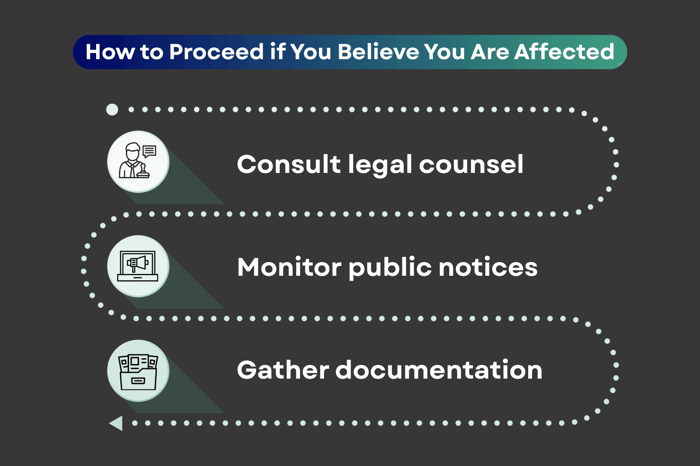

How to Proceed if You Believe You Are Affected

If you believe you have suffered losses due to securities fraud:

- Monitor Public Notices: Watch for class action notices related to companies you invested in.

- Consult Legal Counsel: Seek advice from experienced securities attorneys to evaluate your eligibility and potential recovery.

- Gather Documentation: Collect transaction records, account statements, and relevant communications.

Importance of Legal Consultation and Staying Informed

Attorneys can help assess your claim, ensure compliance with procedural requirements, and maximize your potential recovery.

The legal framework, anchored by the Securities Act, the Exchange Act, and the PSLRA, establishes rigorous requirements for initiating and maintaining these actions. To participate successfully, investors must understand the class period, eligibility criteria, filing process, and their rights and responsibilities. By staying informed and seeking qualified legal guidance, investors can navigate the complexities of securities litigation and protect their financial interests.

You Can Also Read... |

FAQs

What are the requirements for a securities class action lawsuit?

For securities class actions, plaintiffs must meet both the general requirements for class actions as provided by FRCP, Rule 23 and must show the elements of securities fraud have been met.

What is the role of the SEC in securities fraud cases?

The SEC has five key roles in securities fraud cases including: rulemaking and guidance, such as under Rule 10b-5, investigation, investor protection, collaboration, and enforcement.

How do I join a securities class action lawsuit?

To be eligible to join a securities class action, investors must have purchased the securities of a company during the stipulated class period and have suffered financial losses due to the alleged violations of securities laws. If you believe you qualify, you can start by contacting the law firm representing the case which may include completing a submission form to determine eligibility.

What damages can be recovered in a securities class action?

If the court rules in favor of the class, class members may submit claims to recover their share of any settlement or judgment, including lost investment income, lost market value of a stock, and costs borne for seeking legal counsel.

What is the statute of limitations for securities fraud claims?

There are two timeframes applicable to Rule 10b-5 claims that plaintiffs must meet. Generally, plaintiffs must file the claim within two years of discovering the facts of the alleged violation(s) of securities laws and must file the claim no more than five years after the violation occurred.

How are class action lawsuits certified in court?

Plaintiffs must meet the numerous requirements of FRCP, Rule 23 including numerosity, commonality, typicality, and adequacy of representation for class action lawsuits to be certified in court. Plaintiffs of the proposed class must meet the four prerequisites in Rule 23(a) and at least one of the requirements outlined in Rule 23(b).

![Actinium Pharmaceuticals, Inc. (ATNM) Securities Class Action Lawsuit Update [April 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/atnm.jpeg)

![Solaris Energy Infrastructure, Inc. (SEI) Securities Class Action Lawsuit Update [April 30, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/sei.jpeg)