Table of Contents

- What is Securities Fraud?

- Federal Securities Fraud Statute

- Elements of a Securities Fraud Claim

- Insider Trading and Rule 10b-5

- Exchange Act and Securities Fraud

- Securities Fraud Charges and Penalties

- Notable Securities Fraud Cases

- Securities Fraud Litigation and Attorneys

- Towards Safety Shores: Steering Clear of Securities Fraud Risks

- FAQs

Securities fraud is a pervasive threat in global financial markets, undermining investor confidence and the integrity of capital markets.

Investors, regulators, and companies alike must understand what constitutes securities fraud, the legal framework governing it, and the elements required to prove such claims.

This article provides a detailed overview of securities fraud, drawing on authoritative sources to help investors recognize and respond to fraudulent activities.

What is Securities Fraud?

Securities fraud refers to deceptive practices in connection with the offer, purchase, or sale of securities, such as stocks, bonds, or options, that result in financial harm to investors.

This can involve misrepresenting or omitting crucial information, manipulating market prices, or engaging in Ponzi schemes.

The consequences of securities fraud are severe: investors may lose substantial sums, while public trust in financial markets can erode.

The Securities and Exchange Commission (SEC) is the primary federal agency responsible for enforcing securities laws and protecting investors from fraud.

The SEC investigates suspicious activities, brings enforcement actions, and works to ensure that markets remain fair, transparent, and orderly.

Securities fraud can be perpetrated by a variety of actors, including corporate executives, brokers, financial advisors, and even entire companies.

The scope of misconduct ranges from false financial reporting and presenting misleading information to investors to insider trading and elaborate market manipulation schemes.

Federal Securities Fraud Statute

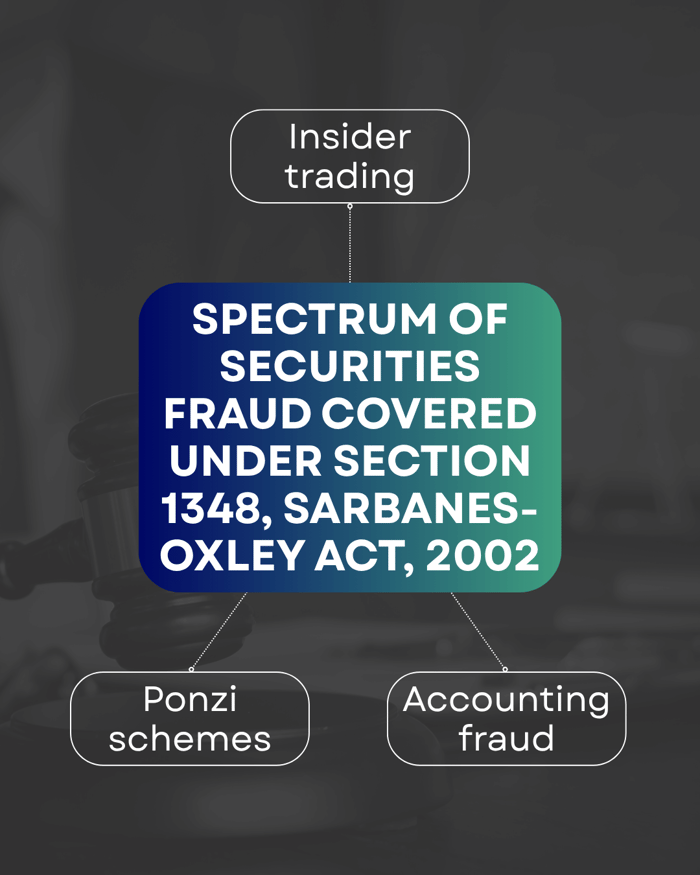

At the federal level, securities fraud is governed primarily by 18 U.S.C. Section 1348, a statute enacted as part of the Sarbanes-Oxley Act of 2002.

This law enables the prosecution of individuals and entities suspected of defrauding investors. Section 1348 covers a broad spectrum of fraudulent conduct, including:

- Insider trading: Trading securities based on nonpublic, material information.

- Ponzi schemes: Using funds from new investors to pay returns to earlier investors, rather than generating legitimate profits.

- Accounting fraud: Falsifying financial statements to mislead investors.

The statute is intentionally broad, allowing the Department of Justice (DOJ) to prosecute a wide array of fraud-related offenses.

Penalties under Section 1348 can include up to 25 years in prison and substantial fines, regardless of the specific nature of the allegations.

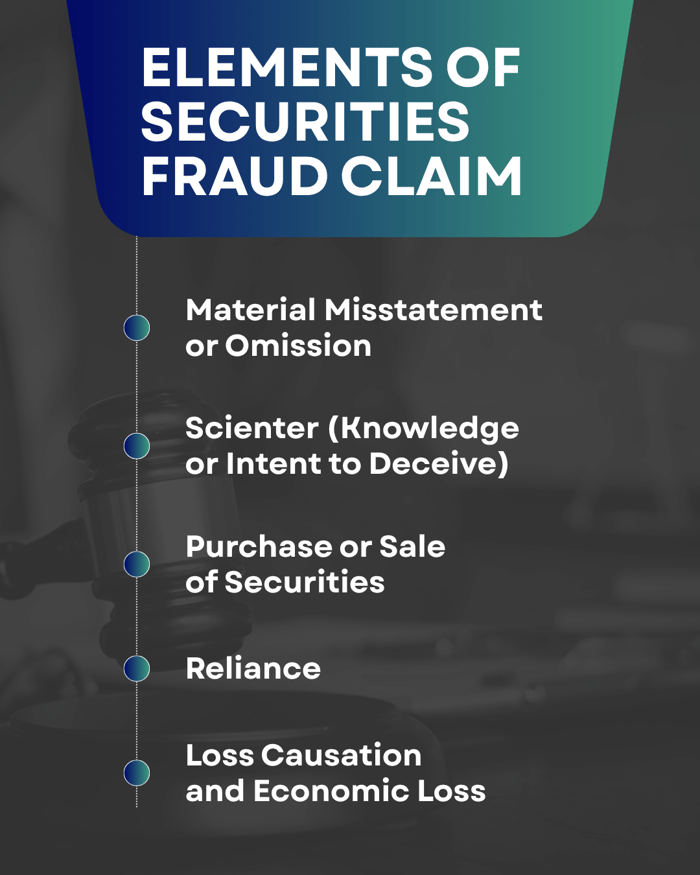

Elements of a Securities Fraud Claim

To prevail in a securities fraud lawsuit, certain legal elements must be established.

These elements ensure that only genuine cases of fraud are prosecuted and that innocent mistakes or business losses are not unfairly penalized.

1. Material Misstatement or Omission

A central element of securities fraud is the presence of a material misstatement or omission.

As per the Securities and Exchange Commission's Rule 10b-5, a statement or omission is considered "material" if there is a substantial likelihood that a reasonable investor would consider it important in making an investment decision (Supreme Court, Basic Inc. v. Levinson, 485 U.S. 224 (1988)).

Material misstatements can take several forms:

- False or misleading statements: For example, a company may overstate its revenues or profits.

- Omissions: Failing to disclose significant risks, ongoing investigations, or adverse developments that would alter an investor’s view.

- Misstatements of intent or belief: Providing overly optimistic guidance about future performance without a reasonable basis.

Example: In the Enron scandal, executives concealed massive debt and losses through off-balance-sheet entities, misleading investors about the company’s proper financial health.

2. Scienter (Knowledge or Intent to Deceive)

Scienter refers to the defendant’s state of mind—specifically, the intent to deceive, manipulate, or defraud. It can be established through:

- Direct evidence, Such as internal communications acknowledging the falsity of statements.

- Circumstantial evidence: Such as unusual insider trading activity or sudden departures of key executives.

- Recklessness: Acting with such disregard for the truth that it amounts to intentional misconduct.

Courts require proof that the defendant acted knowingly or recklessly at the time the misstatement or omission was made.

Example: In the WorldCom case, executives intentionally manipulated accounting entries to inflate earnings, knowing the information was false.

3. Purchase or Sale of Securities

To have standing under federal securities laws, the plaintiff must have purchased or sold the security in question.

This requirement ensures that only those directly affected by the fraud can bring suit.

Additionally, there must be transactional causation—meaning the fraudulent statement or omission influenced the plaintiff’s decision to buy or sell the security.

Example: If an investor bought shares of a company based on false earnings reports, and later suffered losses when the truth emerged, this element is satisfied. (Blue Chip Stamps vs Manor Drug Stores)

4. Reliance

The plaintiff must demonstrate reliance on the false or misleading statement. There are two primary types:

- Direct reliance: The investor personally read or heard the misstatement and relied on it.

- Fraud-on-the-market theory: In cases involving publicly traded securities, courts presume that all public information is reflected in the market price.

Therefore, investors are presumed to have relied on material misstatements that affected the security’s price (Basic Inc. v. Levinson, 485 U.S. 224 (1988)).

Defendants can rebut this presumption by showing that the misstatement did not actually affect the price or that the plaintiff would have transacted regardless.

5. Loss Causation and Economic Loss

Plaintiffs must show they suffered a quantifiable economic loss as a direct result of the fraud and that the revelation of the truth caused the loss.

- Economic loss: Measured by the decline in the security’s value after the fraud is revealed.

- Loss causation: Requires a direct link between the corrective disclosure (e.g., a restatement of earnings or regulatory investigation) and the investor’s loss.

Example: If a company’s stock price drops sharply after it discloses accounting irregularities, investors must show that the drop was due to the fraud, not other market factors.

Insider Trading and Rule 10b-5

Insider trading is a form of securities fraud involving the use of nonpublic, material information to buy or sell securities for personal gain.

The SEC’s Rule 10b-5 (17 C.F.R. § 240.10b-5) prohibits any act or omission resulting in fraud or deceit in connection with the purchase or sale of any security.

Rule 10b-5 is broad, covering not only insider trading but also any scheme to defraud investors. It is a cornerstone of federal securities enforcement.

Exchange Act and Securities Fraud

The Securities Exchange Act of 1934 established the SEC and created a framework for regulating the secondary trading of securities. Key provisions include:

- Mandatory disclosures: Companies are required to file periodic reports (10-Ks, 10-Qs) to ensure transparency.

- Anti-manipulation rules: Prohibit deceptive practices, including market manipulation, wash trading, and disseminating false rumors.

The Act empowers the SEC to investigate, sanction, and refer cases for criminal prosecution, serving as the backbone of U.S. securities law.

Securities Fraud Charges and Penalties

Securities fraud is a felony that can result in severe penalties:

- Criminal penalties: Up to 25 years imprisonment and substantial fines under 18 U.S.C. § 1348.

- Civil penalties: The SEC can seek disgorgement of ill-gotten gains, monetary fines, and injunctions against future violations.

- Private lawsuits: Investors can bring class-action lawsuits to recover their losses.

The SEC and DOJ often coordinate on significant cases, and whistleblowers can report suspected fraud to the SEC for investigation and subsequent action.

Notable Securities Fraud Cases

Several high-profile cases illustrate the devastating impact of securities fraud:

- Enron: Executives concealed debt and losses, resulting in a $74 billion loss for investors and the company’s collapse.

- WorldCom: Massive accounting fraud resulted in over $11 billion in investor losses.

- Bernie Madoff: Ran the largest Ponzi scheme in history, defrauding investors of $64.8 billion.

These cases underscore the importance of robust enforcement and investor vigilance.

Securities Fraud Litigation and Attorneys

Securities fraud litigation is a complex process, involving intricate legal and financial issues. Experienced attorneys are essential for both plaintiffs and defendants.

Plaintiffs must gather evidence, prove the elements of fraud, and quantify losses. Defendants require skilled counsel to navigate investigations, regulatory actions, and potential criminal charges.

Legal strategies may include challenging the materiality of statements, disproving scienter, or demonstrating that losses were due to market forces rather than fraud.

Towards Safety Shores: Steering Clear of Securities Fraud Risks

Securities fraud is a grave offense with far-reaching consequences for investors and markets. Understanding the elements of securities fraud—material misstatements or omissions, scienter, transaction, reliance, and loss causation—is crucial for identifying and addressing it.

The federal legal framework, led by the SEC and DOJ, provides powerful tools for enforcement and investor protection. By staying informed and vigilant, investors can better protect themselves and contribute to the integrity of financial markets.

At Levi & Korsinsky, LLP, we specialize in investor class action lawsuits, representing shareholders who have suffered financial losses due to securities fraud, corporate misconduct, and deceptive investment practices.

With over 80 collective years of experience, our experienced attorneys are on hand to provide you with the support and legal expertise you need to maximize your recovery.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal advice. Readers should not act or refrain from acting on any of the information contained in this blog without consulting a qualified legal professional. Levi & Korsinsky LLP is not responsible for any actions taken or not taken based on the information provided in this blog.

You Can Also Read... |

FAQs

What does securities fraud include?

Securities fraud encompasses false or misleading statements, omissions of material facts, insider trading, market manipulation, and Ponzi schemes.

What are the elements to prove securities fraud?

The elements are: (1) material misstatement or omission, (2) scienter (intent or recklessness), (3) purchase or sale of securities, (4) reliance, and (5) loss causation and economic loss.

What are the elements of conspiracy to commit securities fraud?

Conspiracy to commit securities fraud requires an agreement to commit securities fraud, intent to achieve the fraud’s objective, and proof of an overt act in furtherance of the conspiracy.

What are the elements of a 10b-5 claim?

A 10b-5 claim requires: (1) a material misrepresentation or omission, (2) scienter, (3) a connection with the purchase or sale of a security, (4) reliance, (5) economic loss, and (6) loss causation.

![Digimarc Corp. (DMRC) Securities Class Action Lawsuit Update [June 6, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/digimarc-corp-lawsuit-banner.webp)